Normally, a stock trading near 52-week lows isn’t the ideal time to explore a deal. GitLab Inc. (NASDAQ:GTLB) has seen a tepid rally following reports the company is seeking a potential sale after attracting acquisition interest. My investment thesis is more Neutral on the stock trading up at $54 following the bump for the merger rumors.

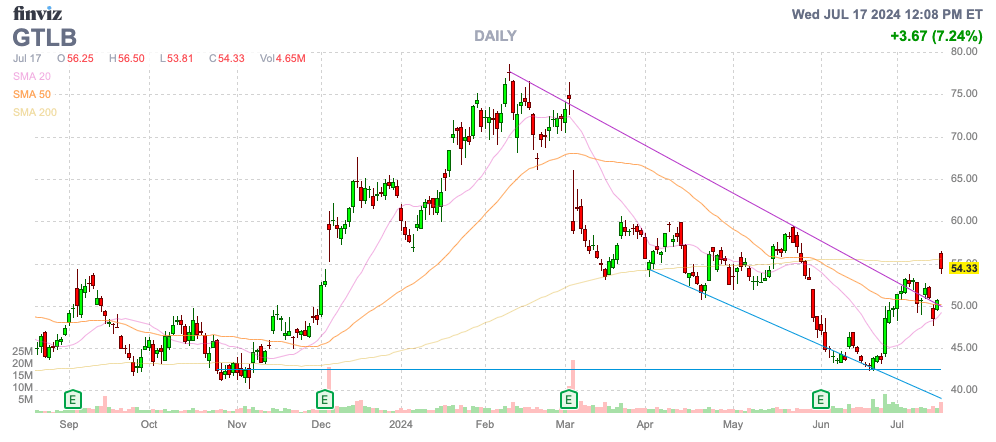

Source: Finviz

Ripe Acquisition Target

GitLab is definitely ripe for an acquisition due to the stock languishing since a hot IPO at the end of 2021. Investors holding GitLab since the stock traded over $100 following the initial trading are likely frustrated with the DevOpsSec company trading down over 50% some 30 months later.

According to the news, GitLab is working with investment bankers on a sales process, though the news seems more a rumor than any hardcore details. Plenty of companies will see if any acceptable bids will come forward without any intent to unload the stock to the highest bidder.

Google parent Alphabet (GOOG, GOOGL) owns 22.2% of the voting stock and could be a potential acquirer, but the company is apparently engaged in a major deal to buy cybersecurity cloud provider Wiz for $23 billion. Google would be a very unlikely buyer right now, possibly limiting the bids to the suggested Datadog (DDOG).

GitLab runs a DevSecOps platform, benefitting already from AI growth. The platform likely has the best opportunity for success with the cloud monitoring platform of Datadog along with less regulatory than a buyout from a big tech firm, not to mention Google might work to block a deal to Amazon (AMZN) or another tech giant.

The company has some other reasons for pursuing a deal now, but these issues might not be legitimate. The controlling shareholder undergoing cancer treatments again and competitive pricing threats from Microsoft (MSFT) are the primary reasons the company might look to dump the business now.

Back on the FQ1 ’25 earnings call, CEO Sid Sijbrandij sadly confirmed another flare up of the cancer issue he faced last year:

On a personal note, during a recent routine scan, I learned that I need to again undergo treatment for osteosarcoma, the same form of cancer I was treated for in 2023. My doctor believes that this finding is part of the original lesion and that as such the disease has not metastasized. I’m working on making a full recovery.

The other issue is competitive pricing threats from Microsoft. The tech giant bought GitHub back in 2018, so a Microsoft threat doesn’t seem a logical reason to dump the shares now, though the tech giant is strong in AI due to the relationship with OpenAI.

As mentioned back on the FQ1 earnings call, Microsoft Developer Copilot already has 1.8 million pay subs with potentially more than $100 million in ARR. GitLab is only getting started with GitLab Duo.

Buy GitLab Stock On Dips

The best way to handle these merger rumors is to buy dips. Our prior research highlighted how GitLab was a buy on dips, such as the move to the low-$40s in mid-June.

GitLab estimates a 10x improvement in software development using their tools. The business should thrive during the great software boost from new AI tools, and the cloud neutrality from the major tech giants is an advantage in this race.

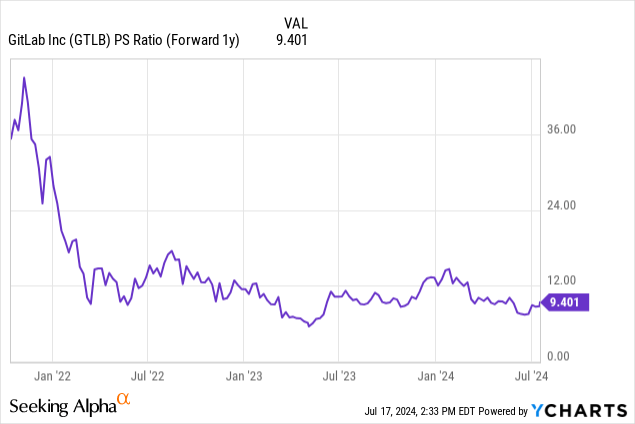

The company has forecasted sales growth of up to 27% this year, and the stock entered today trading at just below 9x FY26 (Jan.) revenue estimates of $921 million. The consensus analyst estimates have revenues growing at least 25% annually through FY27 and likely beyond, but the stock trading much above 10x sales forward a year is a rather rich premium.

The time to load up is when market doldrums allows the stock to dip back into the mid-$40s where GitLab was trading at 7x FY26 revenue targets. The company is already profitable with a cash balance topping $1 billion, so the BoD shouldn’t be desperate to unload the business for financial reasons.

Outside the CEO cancer scare, GitLab really has no reason to unload the stock now outside a massive premium. These sales processes where investment bankers are brought in typically don’t lead to big premiums due to buyers lacking motivation.

The only way to play a potential merger is to buy at the right place for long-term growth. If a big premium buyout occurs, an investor can quickly cash in a big gain. If not, an investor chasing the stock here at $54 will find their trade underwater quickly.

Takeaway

The key investor takeaway is that GitLab Inc. appears poised to ride a strong wave in AI demand for DevOpsSec platforms. A buyout is less than ideal, starting with the stock trading near all-time lows and a lot of the potential buyers clashing with the Google investment.

Investors are best to wait for a dip to buy GitLab for a long-term investment, to where a buyout with a large premium is just a bonus.

Read the full article here