Vir Biotechnology, Inc. (NASDAQ:VIR) develops innovative medicines for treating infectious and viral-associated diseases. The company leverages its proprietary platforms for monoclonal antibodies and the T cell-based Viral Vector to discover therapies to enhance the immune response to combat serious viral disorders. VIR’s pipeline targets the Human Immunodeficiency Virus [HIV], chronic hepatitis delta [HDV], chronic hepatitis B [HBV], and other viral conditions in partnership with entities like the Bill & Melinda Gates Foundation, Alnylam Pharmaceuticals (ALNY), and Gilead Sciences (GILD). Positive results from Phase 2 clinical trials for HDV highlight the company’s potential to address unmet medical needs. On balance, I believe the company’s valuation provides more upside than downside potential at this stage. Thus, I rate VIR a “strong buy” for investors who understand the inherent risks.

Vaccine Platform: Business Overview

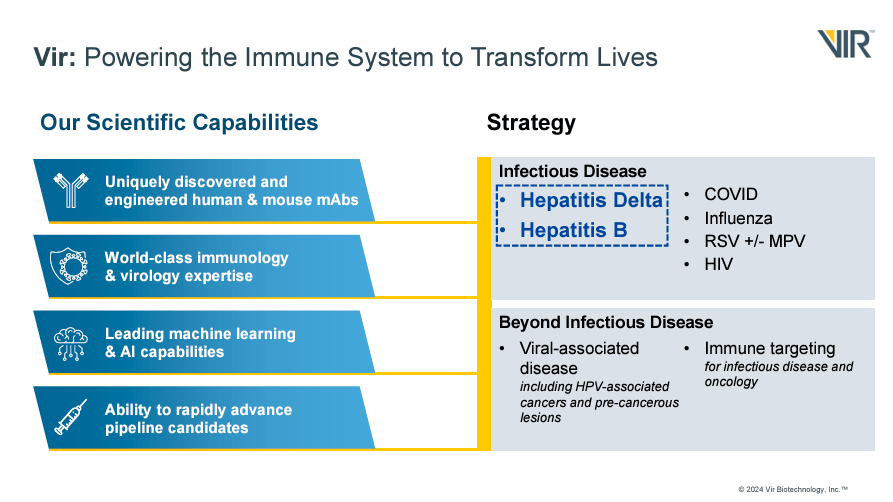

Vir Biotechnology, founded in 2016, is a biotech company headquartered in San Francisco, California. VIR focuses on infectious diseases, viral-associated diseases, and immune targeting, leveraging new technologies to generate immune system therapies against these conditions. VIR uses its proprietary monoclonal antibody discovery platform and T cell-based Viral Vector technology, which elicits T-cell responses, generating novel vaccines and antibodies.

Source: Corporate Presentation. June 2024.

Therefore, the company’s platform uses AI to engineer proteins and create antibodies targeting pathogens with high specificity, reducing side effects and enhancing treatment efficacy. This approach generated sotrovimab for COVID-19 in collaboration with GlaxoSmithKline (GSK). Sotrovimab is authorized for the disease’s early stages. On the other hand, VIR’s T cell-based Viral Vector platform employs engineered viruses that carry genetic elements that produce T-cell responses, strengthening the body’s defenses. This way, VIR develops vaccines, infectious disease therapies, and oncology treatments, generating a durable immune response.

Source: Corporate Presentation. June 2024.

It’s worth mentioning that VIR’s vaccines are based on the Human cytomegalovirus [HCMV]. This common herpes virus causes persistent immune activation, producing a pool of effector memory T cells critical for long-term immunity following infections. This vaccine is in Phase 1. VIR also has an additional preclinical program for an HIV functional cure using a combination of mAB. The vaccine and the functional cure are being developed in collaboration with the Bill & Melinda Gates Foundation.

Product Pipeline: HIV, Hepatitis, and COVID-19

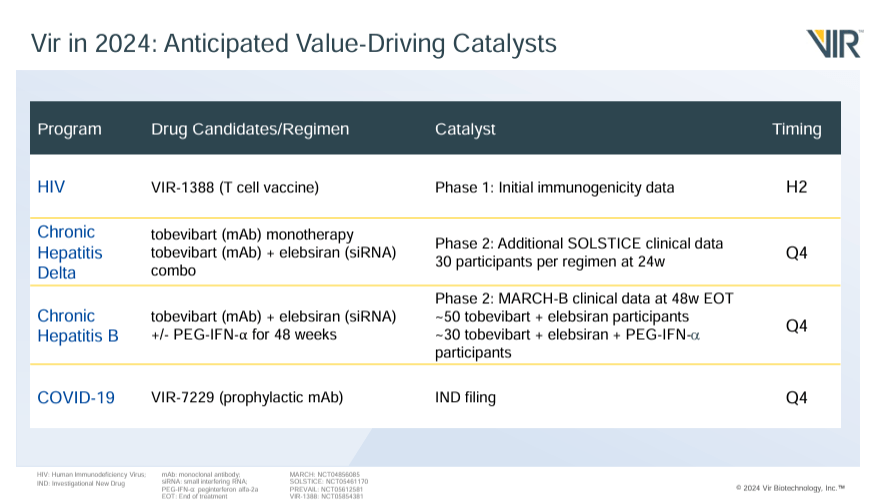

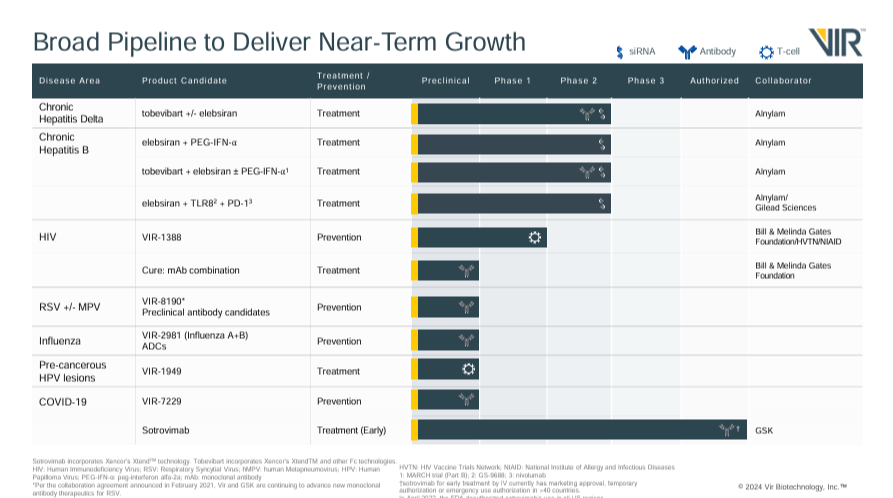

Vir’s pipeline addresses HIV, chronic hepatitis delta, chronic hepatitis B, and COVID-19. The underlying approach uses advanced monoclonal antibodies to target and kill viruses and small interfering RNA (siRNA) to degrade viral RNA to combat infections. The HIV program focuses on developing a T-cell vaccine called VIR-1388, currently in Phase 1. Initial immunogenicity data from the trial is expected in H2 2024.

Source: Company’s website.

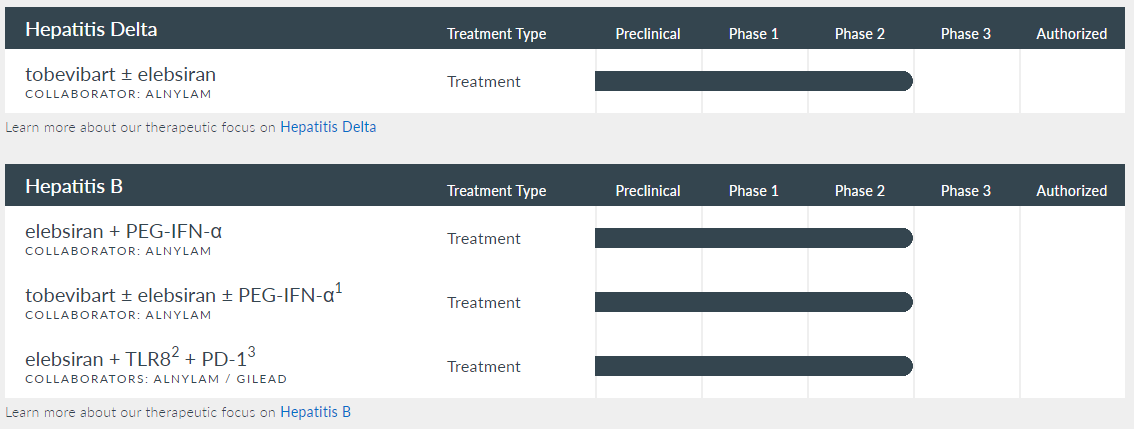

The chronic hepatitis delta [HDV] program studies two drug candidates: Tobevibart, a monoclonal antibody [mAb], applied as monotherapy and combined with Elebsiran (siRNA). This research is in Phase 2, with data from the SOLSTICE trial expected in Q4 2024. The chronic hepatitis B [HBV] program is studying a regimen consisting of the combination of mAbs plus Elebsiran applied to 50 study participants and 30 participants receiving the same combination of drugs plus pegylated interferon-alpha (PEG-IFN-α) for 48 weeks. Data from the MARCH-B Phase 2 study is expected by the end of this year.

The HBV program is also investigating in Phase 1 the combination of Elebsiran, which reduces the viral load by silencing viral RNA, with a Toll-like receptor 8 [TLR8] agonist to stimulate the immune response and with programmed cell death protein 1 [PD-1] inhibitors to prevent immune evasion of the virus. This multifaceted approach aims to obtain a functional cure for chronic hepatitis B. The program’s first three product candidates are developed in collaboration with ALNY, and the combination of Elebsiran with TLR8 and PD-1 inhibitors is investigated with GILD.

Source: Corporate Presentation. June 2024.

The COVID-19 program has a prophylactic mAb called VIR-7229 in the Investigational New Drug [IND] filing phase, expected in Q4 2024. This drug will complement Sotrovimab, an FDA-approved treatment for early treatment of the disease. VIR’s broad pipeline also includes programs in the preclinical stages. First, 1) VIR-1949 for pre-cancerous HPV lesions as a T-cell-based vaccine. Second, 2) VIR-8190 for Respiratory Syncytial Virus [RSV] and Human Metapneumovirus [MPV] as a monoclonal antibody. Third, 3) VIR-2981 for influenza A+B as a monoclonal antibody. Lastly, 4) antibody-drug conjugates [ADCs] for influence A+B.

Positive Trial Data and Fast Track Prospects

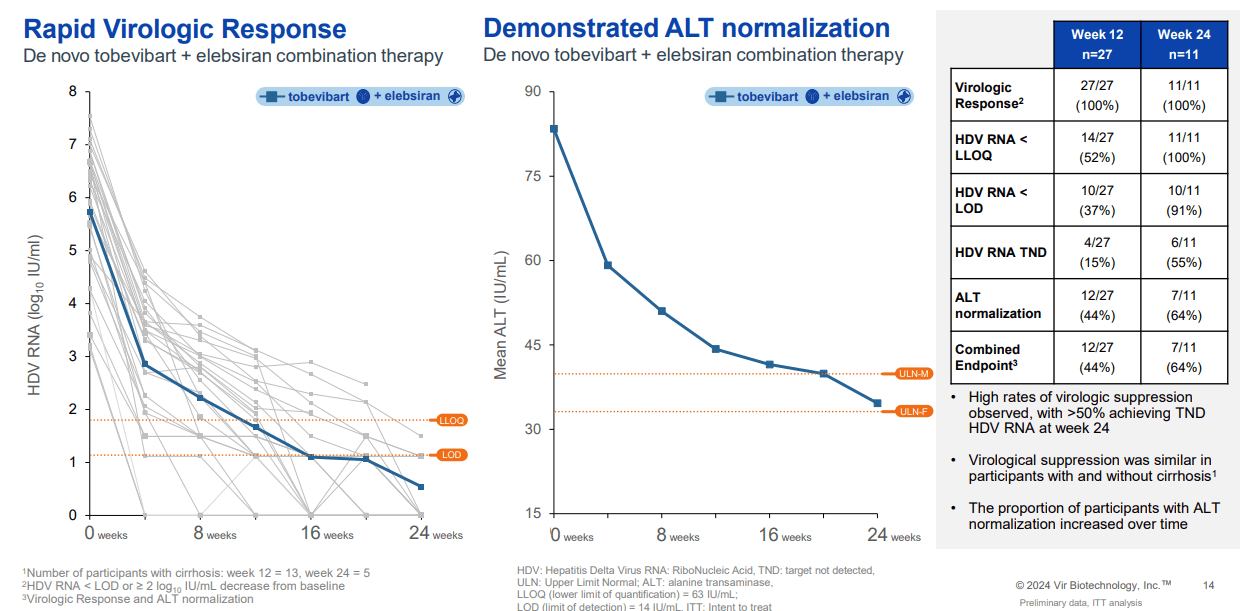

It’s worth mentioning that on June 5, 2024, VIR announced positive results from the Phase 2 SOLSTICE trial of the Tobevibart drug candidate, which showed signs of efficacy for HDV, reducing the viral load as a single agent and combined with RNA-interfering treatment Elebsiran. 50% of the participants presented a normalization of the alanine aminotransferase [ALT] enzymes, indicating improved liver function. The safety profile also showed favorable results. The market reacted positively, underscoring investor optimism about the opportunities for this therapy. Elebsiran and Tobevibart are developed in partnership with ALNY.

Source: Corporate Presentation. June 2024.

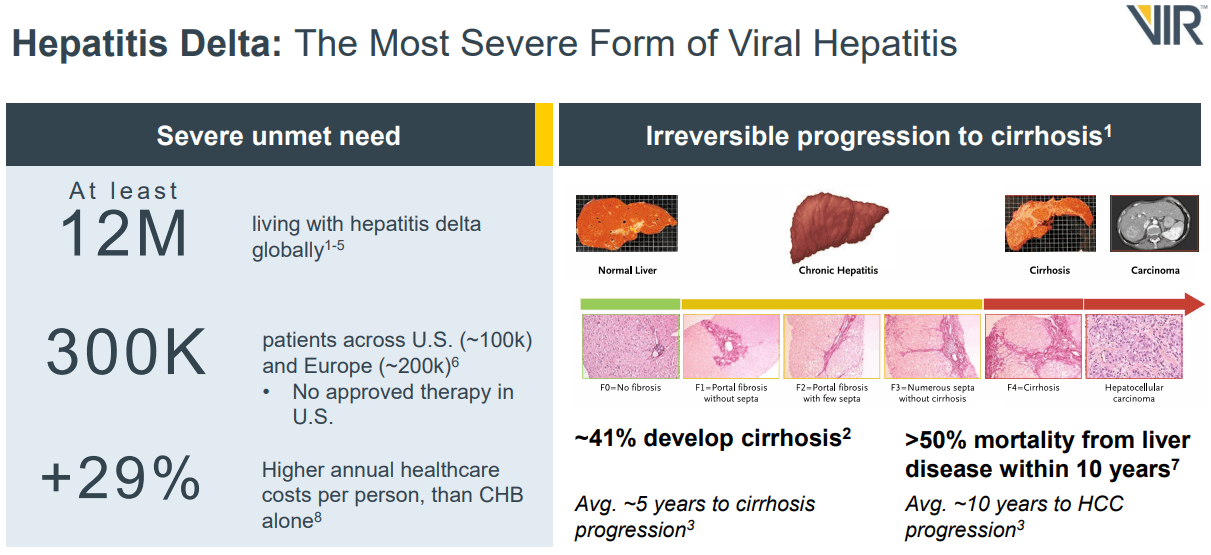

Additionally, VIR received FDA Fast Track designation and IND clearance for combining Tobevibart and Elebsiran. The Fast Track designation should expedite the treatment’s review process, especially since the World Health Organization regards hepatitis delta as the most severe form of chronic viral hepatitis. This variant rapidly progresses to liver cancer and can be life-threatening. For context, there are around 12 million HDV patients worldwide. Thus, VIR is planning a new ECLIPSE trial to evaluate monthly injections of the two combined drugs versus the current standard of care [SoC].

Compelling Investment: Valuation Analysis

From a valuation perspective, VIR trades at a $1.3 billion market cap, making it a midsized biotech. Its balance sheet holds $160.7 million in cash and equivalents, $985.1 million in short-term investments, and $359.7 million in long-term investments (available-for-sale debt securities). If we add these together, VIR has ample liquid resources amounting to $1.5 billion. It has no financial debt, with total liabilities of $246.6 million. VIR’s book value is $1.5 billion as of Q1 2024.

Moreover, I estimate the company’s latest quarterly cash burn was $110.8 million by adding its CFOs and Net CAPEX. This implies a yearly cash burn of $443.2 million, which is considerable and suggests a cash runway of 3.4 years. This runway gives VIR considerable flexibility, but since its most advanced program is in Phase 2, it is still several years away from FDA approval. For instance, VIR’s HDV Phase 2 research is fast-tracked by the FDA, but even if Phase 3 starts in 2025, it’d indicate its FDA approval would be around late 2026 or 2027, assuming it all goes according to plan without significant delays. A similar timeline would also apply to VIR’s HBV program, but note that this one isn’t fast-tracked by the FDA, so that could take even longer than 2027.

Source: VIR’s Q1 2024 10-Q.

Also, most of VIR’s Q1 2024 revenues came from its contract revenues related to agreements to provide R&D services using its mAb discovery platform. There could be growing demand for monoclonal antibody research, but that’s still somewhat unpredictable. Nevertheless, if such revenues were consistent, it could be a valuable revenue vertical for VIR. Moreover, milestone payments related to collaboration agreements with GSK, ALNY, or GILD could provide lumpy cash flows from time to time. Yet, I believe VIR has proven that its mAb platform has potential and already generated revenues.

Source: Corporate Presentation. June 2024.

Also, its HDV, HBV, and HIV pipeline taps into considerable TAMs of $0.7 billion, $35.6 billion, and $34.1 billion, respectively. The COVID-19 market is also a potential value driver, though it’s seemingly waning. These value drivers I’ve identified suggest the company could generate billions in annual revenues, though they’re inherently speculative. Even if we look at VIR’s book value of $1.5 billion, it implies a 0.9 P/B ratio, which is self-evidently cheap.

For context, the sector median P/B multiple is 2.5, so VIR seems relatively undervalued. In fact, VIR trades below the value of its liquid assets of $1.5 billion. Despite accounting for the ongoing cash burn, VIR seems cheap from multiple angles, especially considering its potential upcoming catalysts and value drivers. Hence, I rate VIR a “strong buy” for investors who understand this investment’s inherently speculative biotech nature.

Investment Caveats: Risk Analysis

Naturally, my investment thesis has several risks that are worth considering. First, the company’s pipeline remains in relatively early stages, with its most advanced programs still in Phase 2. This means several research milestones could be delayed, decreasing the present value of future cash flows. Moreover, the FDA could reject the company’s submission at some point. Therefore, FDA approvals are not guaranteed, and these regulatory risks would be a meaningful blow to the bull case. Also, VIR is targeting highly competitive markets. The hepatitis and HIV markets are highly competitive, with many established players with more resources and different approaches that could ultimately outclass VIR’s offerings.

Source: TradingView.

Lastly, the company’s high cash burn rate requires it to progress its research swiftly. Otherwise, its tangible value could diminish without generating significant IP in return. Nevertheless, despite these risks, I believe VIR trades at a compelling valuation and offers diversified exposure to sizeable TAMs that could deliver considerable long-term shareholder value. Therefore, I think VIR’s investment case justifies the inherent biotech risks.

Strong Buy: Conclusion

Overall, VIR is a promising biotech targeting hepatitis, HIV, and COVID-19. It also has a valuable mAb platform that can potentially generate consistent contract revenues that could help it fund its research programs. This investment has competitive, clinical trial, and regulatory risks, but despite these, I consider VIR’s compelling valuation to provide more upside than downside at this stage. Thus, I rate VIR a “strong buy” for investors who understand the inherent risks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here