Being brutally honest with you, there is a distinct possibility that Spirit Airlines (NYSE:SAVE) is not long for this world. The last article that I wrote about the company was published in January of this year. At that time, I rated it a ‘hold’ simply because there was some probability of its merger with JetBlue Airways (JBLU) playing out. It wasn’t long after that, however, that all hope of this merger being consummated died. On March 4th of this year, the management team at Spirit Airlines announced that the merger agreement had been terminated. This came after regulators blocked the transaction.

Since that announcement, shares are down a whopping 56.3%. But that’s not even the worst of it. From the 52-week-high mark, shares are down an impressive 85.3%. Some investors might view this as a great buying opportunity. But I would caution against that thought process. The fact of the matter is that the companies fundamental condition continues to worsen. Revenue is falling even as air traffic is rising. Costs are out of control and debt continues to grow. Absent something significant changing for the better, I struggle to imagine a scenario where the company does not collapse. And because of this, I have now downgraded the stock to a ‘strong sell’.

Pain keeps mounting

Author – SEC EDGAR Data

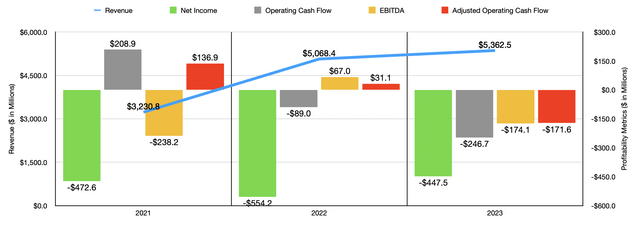

Fundamentally speaking, Spirit Airlines can only be described as a mess. For years now, revenue has grown, but that has not stopped profits and cash flows from suffering. If you take the 2021 through 2023 window as an example, you can see precisely what I mean. In 2021, revenue was $3.23 billion. By 2023, it had expanded to $5.36 billion. There were a couple of reasons behind this. First, the economy was recovering following the COVID-19 pandemic. The airline industry was absolutely decimated for a couple of years. So 2021 was a time of recovery. However, the company did also benefit from an increase in the number of aircraft at its disposal during this time. In 2021, for instance, the business had 173 aircraft. This number grew to 194 in 2022 before growing further to 205 last year.

Author – SEC EDGAR Data

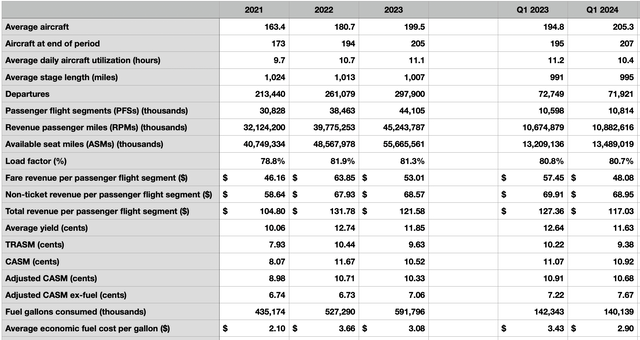

In the table above, you can see a variety of metrics during this three-year window of time, as well as for the first quarter of this year compared to the same time last year. In addition to seeing a rise in aircraft, the firm also saw a growth in revenue per passenger flight and a rather significant improvement in the overall departures of its aircraft. In most cases, investors would view these data points in a positive light. And in some respects, I can understand why that is. After all, during the pandemic, there was a lot of uncertainty regarding how long it would take for the airline industry to eventually recover. It, movie theaters, and cruise lines, were probably the three industries most negatively affected by the pandemic. It’s also great to see a growth in the number of aircraft, since it indicates that management is investing for the future.

The problem is when growth is not profitable. In each of the three fiscal years covered, the company generated significant net losses. The $472.6 million loss seen in 2021 was understandable given the difficulties that the industry was still working its way through. But that loss ballooned to $554.2 million in 2022. Even last year, the company generated a loss of $447.5 million. This was not the only profitability metric to take a hit. Operating cash flow went from positive $208.9 million to negative $246.7 million over this window of time. If we adjust for changes in working capital, we get a similar deterioration from positive $136.9 million to negative $171.6 million. By comparison, EBITDA was a lot lumpier. But even last year, it came in negative to the tune of $174.1 million.

Author – SEC EDGAR Data

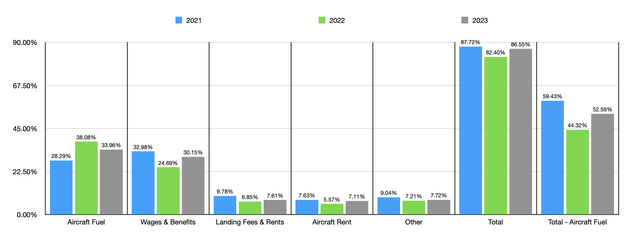

Frankly, the company’s biggest issue is on its bottom line. The airline industry is notoriously competitive anyways. This means that margins are often thin. But as a budget airline, being financially successful is all that more challenging. In the chart above, you can see the items that I consider to be core costs for the business. For context, the ‘Other’ category consists of maintenance, materials, and repair costs, as well as distribution expenses. I excluded depreciation and amortization since those are non-cash items entirely. And because it’s not at the operating level, I also excluded interest expense. But for context, it remained relatively flat during this three-year window of time.

Once again, the bloated cost structure in 2021 makes sense. We saw a big improvement for core costs from 2021 to 2022. They dropped from 87.72% to 82.40%. But then, in 2023, they grew to 86.55%. The differences are even more extreme when we exclude aircraft fuel from the equation. In this case, after dropping to 44.32% in 2022, core costs for the business jumped to 52.59% last year. A big portion of this increase involved wages and benefits. Those jumped from 24.69% of sales to 30.15%. It probably doesn’t help that, during that time, compensation for the company’s CEO went from $3.4 million to $6.6 million, with total compensation amongst the firm’s top brass more than doubling from $8.5 million to $18.4 million. Higher rent rates, additional operations, and new gates at existing stations, were instrumental in pushing landing fees up from 6.85% to 7.61%. The company also added 29 new operating leases from 2022 to 2023 that helped to push aircraft rent expenses up from 5.57% to 7.11%.

Author – SEC EDGAR Data

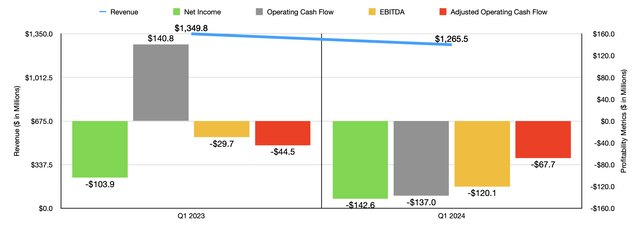

The 2024 fiscal year has shown that this trend is continuing. For the first quarter of the year, the company did generate lower revenue year over year of $1.27 billion. That’s a decline of 6.2% compared to the $1.35 billion reported one year earlier. Part of this was driven by a 1.1% decline in the number of departures (though total traffic rose by 1.9%). But a bigger contributor was a drop in total revenue per passenger flight from $127.36 million to $117.03. This is not terribly surprising. Back in June, news broke that airfares fell 5.9% for the month of May. That was on a year-over-year basis. This is in spite of the fact that air traffic has risen nicely from last year to this year.

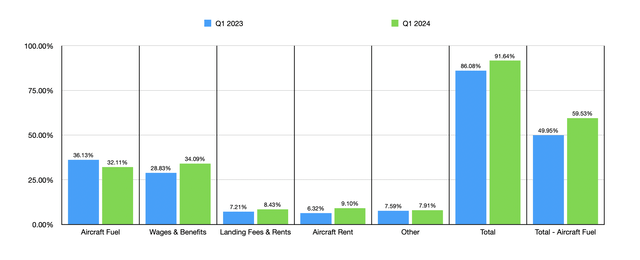

Unfortunately, the drop in sales also brought with it a decline in profitability. The firm’s net loss went from $103.9 million last year to $142.6 million this year. Other profitability metrics also took a hit. Operating cash flow went from $140.8 million to negative $137 million. If we adjust for changes in working capital, it still worsened from negative $44.5 million to negative $67.7 million. And lastly, EBITDA for the company fell from negative $29.7 million to negative $120.1 million. As you can tell in the chart below, core costs for the business continued to rise, climbing from 86.08% last year to 91.64% this year. The increase becomes even larger if we exclude aircraft fuel from the equation. In this case, we get a worsening from 49.95% of sales to 59.53%. While landing fees and aircraft rental fees both contributed to this, a lot of pain came from wages and benefits. They grew from 28.83% of sales to 34.09%.

Author – SEC EDGAR Data

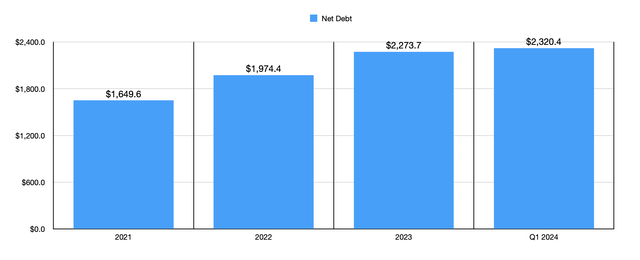

Data paints a very scary picture for shareholders. But this isn’t all. Management expects weakness to continue. In addition to seeing available seat miles this year potentially being flat and, in the best case, rising only at a low single digit rate, the firm anticipates, for the second quarter of this year, an adjusted operating margin that will be negative to the tune of between 9% and 11%. To make matters even more unfavorable, the company continues to see its debt picture worsen. From 2021 through 2023, net debt for the company expanded from $1.65 billion to $2.27 billion. By the first quarter of this year, it had risen further to $2.32 billion. And with cash flows likely to continue being in the red, debt is likely to grow more from here.

Author – SEC EDGAR Data

I am not the only one sounding the alarm on Spirit Airlines. Earlier this month, Raymond James pointed out that weaker fare trends and insufficient post summer capacity adjustments remain risk factors for discount carriers. The company even labeled Spirit Airlines as one of its two ‘Underperform’ firms in this space. This is down from a ‘Market Perform’ rating previously. Raymond James is in good company on this. As you can tell from the image below, while Seeking Alpha analysts currently have Spirit Airlines rated a ‘hold’ on average, Wall Street analysts have it rated a ‘sell’. The Quant Rating System that Seeking Alpha developed is even more bearish, rating the company a ‘strong sell’. This is largely because of factors like momentum, earnings per share revisions, and profitability.

Seeking Alpha

We also have leadership issues to contend with. In early June of this year, the company announced that the company’s Vice President and Controller, Brian McMenamy, was being named the interim CFO for the business, stepping in to replace its then-CFO Scott Haralson, who decided to become the CFO of another company outside of the airline industry. And on July 1st, the company announced that Fred Cromer was being appointed as Executive Vice President and CFO as the interim CFO that had been previously announced will step down and focus on a different senior financial role within the business. There were at least two other updates to the company’s top brass during that time as well. I feel like there is some joke in here somewhere about rats abandoning the Titanic. But maybe that is my own cynicism.

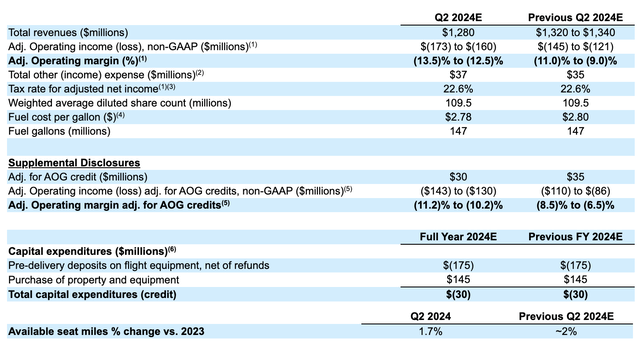

Subsequent to the writing of the rest of this article, but before its publication, the picture for the business worsened. On July 16th, management announced some preliminary results for the second quarter of the firm’s 2024 fiscal year. They said that lower-than-expected non-ticket revenue resulted in revenue for the quarter likely to come in at about $1.28 billion. In addition to being well below the $1.43 billion reported the same time last year, this is a bit lower than the $1.32 billion to $1.34 billion management previously expected. Adjusted operating income is now supposed to be negative to the tune of between $160 million and $173 million. This is worse than prior forecasts of between $120 million and $145 million.

Spirit Airlines

Management did say they are working to improve operations, and even cited liquidity of $94 million year-to-date stemming from a contracted entered into with an affiliate of Pratt & Whitney that entitles it to receive aircraft-on-ground credits. For the year as a whole, these credits will likely be worth between $150 million and $200 million. But shares still managed to fall by 10.8% on July 17th after Thomas Fitzgerald, an analyst at TD Cowen, stated that, “we do not believe the company has a realistic path toward profitability through 2026 and think there is substantial risk of a restructuring or bankruptcy”. As you can tell from the rest of this article, I would certainly agree with that view.

Takeaway

Fundamentally speaking, things are not going well for Spirit Airlines. The company’s top and bottom lines are worsening and debt is growing. The company suffers from a bloated cost structure, and it is unclear whether this can be rectified outside of bankruptcy. It is true that the company’s CEO announced, in early June, that the company is not currently considering a bankruptcy filing. This followed the decision by S&P Global to downgrade the company’s debt rating even deeper into junk territory because of operating performance and concerns about inadequate liquidity for the next 12 months. In particular, S&P Global expressed that it believes, ‘it is likely that the company will face a distressed exchange’ as it works to engage lenders to refinance about $1.6 billion in upcoming debt maturities. When you add all of this together, it seems very clear to me that the company is struggling and that the downside from this point, while seemingly small, could very well be significant. Due to these factors, I have no problem rating the company a ‘strong sell’ at this time.

Read the full article here