Summary

In April, Swiss-based ski conglomerate Jungfraubahn Holding AG (OTCPK:JFBHF) (JFN.SW) announced 2023 results and published its corresponding annual report. I previously covered this stock back in February 2024. The firm not only has fully recovered from the COVID-19 downturn but has registered its best year in history with record sales, operating, and net profit. The firm is back on track to deliver very good returns to shareholders starting with the 80.55% YOY increase in the dividend. My buy rating is confirmed.

Company website

2023 Results Overview

Division Performance

Jungfraujoch Top of Europe: for the first time since 2019 more than 1 million visitors traveled to the Jungfraujoch mountain. With 1,007,000 guests, the number of visitors was 61.1% higher than the previous year and only 4.6% lower than the figure for the last pre-crisis year of 2019. The trip to the Jungfraujoch Top of Europe has become significantly more attractive due to the faster access, and the higher transport capacity thanks to the V-Bahn.

Adventure mountains: This division was able to make further significant gains. It had higher frequencies, an increase in average revenue from tickets, higher sales from rented catering establishments, and also record sales for the soft adventure.

Winter sports: Although the 2022/2023 winter season was snow-poor and in general warm weather affected the winter sports business in many Alpine foothills areas, Jungfrau Ski Region recorded a good result with 1.1 million skier visits. In contrast, the 2023/2024 winter season started much better. Thanks to a good snow cover the Jungfrau Ski Region registered already 207,800 skier visits by 31 December 2023. Compared to the previous season, this represents an increase of 28.1%, making it the best start to the season in history.

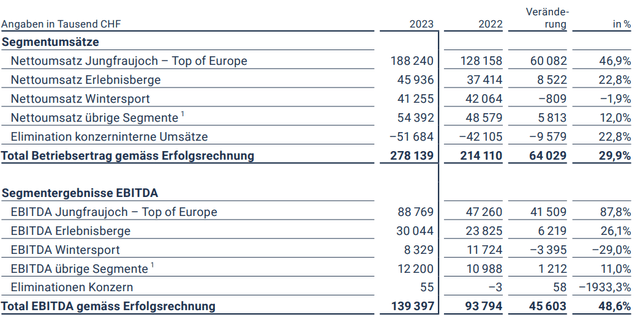

Below is shown the different performance of each division in 2023 and 2022: Units expressed in thousands of CHF

2023 Company Annual Report

Financial Performance

Units expressed in millions of Swiss Francs. All the financial information has been extracted from the company’s 2023 annual report.

P&L Statement

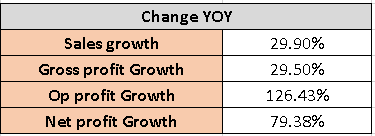

As mentioned at the beginning of this article, Jungraubahn has broken all the records as indicated in its annual report, with the following numbers:

-

Revenue: 278.139 million CHF.

-

EBITDA: 139.397 million CHF

-

EBIT: 99.631 million CHF

-

Net Profit: 79.617 million CHF

In comparison with the 2022 numbers, this confirms the huge improvement in operations that the firm has enjoyed during this last year.

Image created by the author using information from the company´s annual reports. (Author Own Analysis)

Balance Sheet Statement

The balance sheet continues to show how the management is running conservatively the company. The equity value has grown 1% in the last year. The outstanding debt at the end of 2023 is 117.2 million CHF and the firm has 31.293 million CHF in cash and equivalents, leaving a Net Debt/EBIT ratio at 0.862. The debt composition at the end of 2023 was as follows:

-

75.2% are loans from the Canton of Berne Public Transport, interest-free.

-

17.1% are also loans from the Canton of Berne under the New Regional Policy, interest-free.

-

7.8% are bank loans.

This means that the firm is almost isolated from the interest rate movements and can focus on expansion investments and projects.

Cash Flow Statement

The operating cash flow has grown 4.2% YOY to 96.33 million CHF in 2023. The firm has invested 36.83 million CHF in properties, plants, and equipment. Another 22 million CHF have been invested in fixed-term deposits.

The shareholders were rewarded in 2023 with 41.825 million CHF in stock buybacks reducing the outstanding share number to 5.59 million. And, 20.991 million CHF in dividends, representing a total yield of around 7% taking an average stock price of 170 CHF during 2023. The company approved in the 2024 Annual General Meeting an amazing dividend increase of 80.55% in 2024, going from 3.6 CHF to 6.5 CHF per share. At the current share price, represents a dividend yield of 3.34%. The free cash flow (FCF) in 2023 was 59 million CHF, slightly improving the 2022 register by 0.53%.

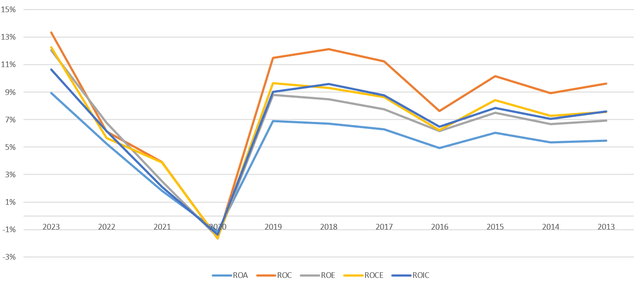

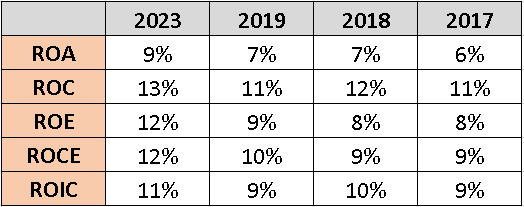

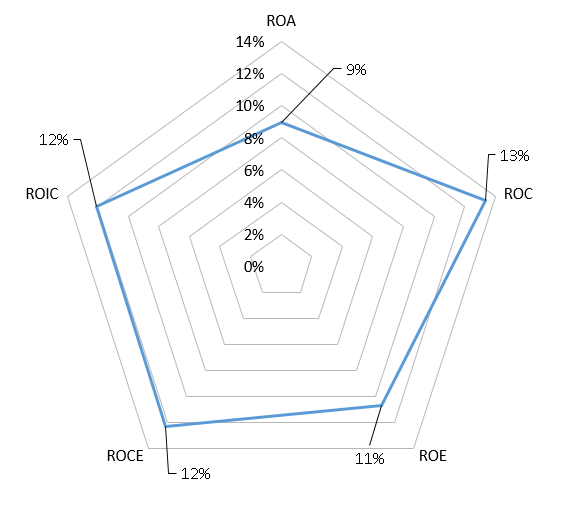

Key Financial Indicators

Image created by the author with information from the company´s annual reports. (Author Own Analysis) Image created by the author with information from the company´s annual reports. (Author Own Analysis) Image created by the author with information from the company´s annual reports. (Author Own Analysis)

We can see how 2023, saw the highest profitability indicators in recent years. This confirms that the company is back on track to improve the pre-Covid numbers. In my opinion, these rates of return will keep this level or could go even higher in the coming years as the V-cableway investment is improving both the top and bottom line results, helping the company to increase margins and drive higher shareholder returns.

Valuation

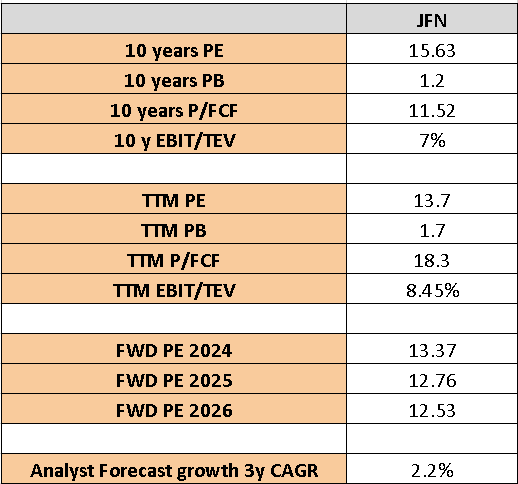

Historical Multiples Comparison

Image created by the author with information from the company´s annual reports and analyst’s forecasts. (Author Own Analysis)

The company’s stock is trading at its historical valuation levels as the share price has already closed the multiple gap to historical levels. Currently, analysts forecast an annual growth CAGR rate of around 2.2% until 2026. The expected P/E ratio at the end of 2026 is 12.53, considerably lower compared to the historical P/E multiple.

Analysts expect the next three years to be a consolidation period for Jungfraubahn but, I think they are not weighing in enough on the improved profitability that the V-Cabeleway is bringing to the firm results. In my opinion, the company will go back to its historical growth levels of around 4-5% in the long term.

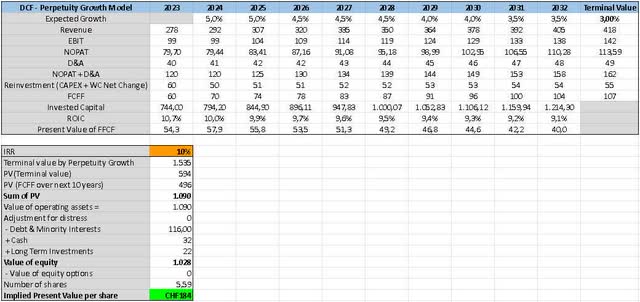

Discounted Cash Flow Valuation

In this chapter, I apply a conservative view as the share price has already performed really well in the last two years, fully reflecting the massive improvements in its results and the consequently P/E multiple expansion. From now on, I believe the stock is going to be in a consolidation phase where the firm will lean toward its historical metrics.

Calculation assumptions:

Revenue growth: looking at the historical data, over the last 15 years, JFN managed to grow its revenue at an average of 4.97%. I believe that the firm and the management will continue to make accreditation decisions and grow the business at a similar rate. Therefore, I take the 5% rate as the most probable rate of growth. Instead, I consider the perpetual rate of growth to be 3%, which I think will be the average rate of growth of the Swiss economy in the longer term.

EBIT Margin: historical data indicates a margin of 30% on average for the last 15 years. Using this period, the complete business cycle is covered and reflected in the average margins.

Tax Rate: 21.04%, is the 2024 Swiss Bern Canton corporate nominal tax rate.

Reinvestment Rate: in the last 15 years, the firm has re-invested an average of 50.2 million CHF back into the business with a CAGR of 2.1%. These values include the big investment that the V-Cableway construction meant for the firm. I think including this in the calculation will take into account potential future big expansions that the firm will perform.

Investment Rate of Return, IRR: here I do not use the WACC as personally I look for a minimum IRR in my positions of at least 10%, for me this should be the standard rate of return for an international investor.

Image created by the author with data from the 2023 annual report and author estimations. (Author’s Own Analysis)

Applying the input presented above, the DCF calculation gives a target share price of 184 CHF for investors looking to get a 10% return on their investment. This number validates my view that currently, the shares are trading at a fair price.

Peers Latest Results Update

I would like to add here an extra update for readers interested in this sector. I am referring to Jungfraubahn’s publicly traded Swiss competitor Bergbahnen Engelberg-Titlis AG (TIBN). This company is not covered here in SA and therefore, I cannot write an article on it.

On the 28 of June 2024, the company released an announcement about the performance of the company between November 2023 and April 2024. The company stated a massive increase in both income and visitors. For the fiscal year from April 2023 to April 2024, the company has registered the following numbers:

-

Revenue: 69.22 million CHF.

-

EBITDA: 31.3 million CHF

-

EBIT: 47.1 million CHF (due to a special sale of some of the company’s land).

-

Net Profit: 16.97 million CHF

-

Net Debt: -3.1 million CHF

-

Market Capitalization: 135.52 million CHF

The share price is sitting at a historically low multiple as the market has not priced in yet the massive improvement of results. The table below shows the current multiples at which the firm shares trade:

Author Own Analysis

This means there is a big catalyst in place for the price to close the gap with historical valuation. The current valuation implies almost 55% upside potential to arrive at 12.5 P/E which would place the share price at around 60-65 CHF. In addition, the dividend could be coming back, and also the stock is trading below book value.

Investors should bear in mind that TIBN is a very small company with only 135 million CHF of market capitalization and very illiquid trading activity, only 723 shares change hands daily on average. This could be a reason why the market has not recognized this discrepancy between price and value.

Downside Risk

The share price has been behaving in a very positive way for the last 2 years, years. For example, from the lows in December 2022 where the share price has gone from 125-130 CHF to the current 190+ CHF levels delivering an impressive 74% appreciation.

As mentioned before, I believe that this type of very strong stock price upside is something from the past as the company’s results have fully recovered from the pandemic shock and are already breaking historical records. This means that the price action will not be as explosive on the upside as the earnings expectations are at a higher plateau. From now on, the firm needs to continue delivering exceptional results to justify further big upside moves. In my opinion, the firm will most likely deliver positive results in line with historical rates of growth and profitability and that´s why I consider the firm now in a consolidation phase.

In this line, I would like to share a cautious message with readers about some downside risks that could affect Jungfraubahn. During the 2020 pandemic, this firm suffered a very strong hit in earnings as international tourism was banned. This fact shored up a key weakness of its business model by having an important dependency on international tourism.

Asia and other emerging markets are especially important as they have a growing middle class with the capacity to visit the Swiss Alps. This is translated into a risk of earnings degradation if those world areas suffer from an economic downturn. The best example is the Chinese economy situation that has been struggling for the last 2 years from the pandemic and after the real-state turmoil and how the government is not able to stimulate the domestic economy to overcome these issues.

The data from the EU shows sluggish economies given the persistent energy crisis and structural low productivity levels, which have sparked the loss of competitiveness in many important industries. This could also be reflected in the amount of Europeans that visit the Jungfraujoch mountain region every year.

Lastly, the US is also an important market for Jungfraubahn earnings and the latest data presents a cooling economy where the middle class is starting to suffer from the prolonged high interest rate. If this trend continues, transferring those symptoms into the labor market, many American tourists could cancel their future visits to Switzerland until the economic situation improves again.

If all these recession fears or generalized economic environment deteriorations turn true, it could result in lower Jungfraubahn earnings, and send the share price into a correction scenario.

Conclusion

The 2023 results have confirmed the full recovery of the company from the COVID crisis. The management has continued to deliver solid returns to the shareholders by increasing substantially the dividend, increasing the stock buybacks, and driving the company profitability to a new level. Another positive news is the substantial contribution of the new V-Cableway that helped the firm to achieve record results last year.

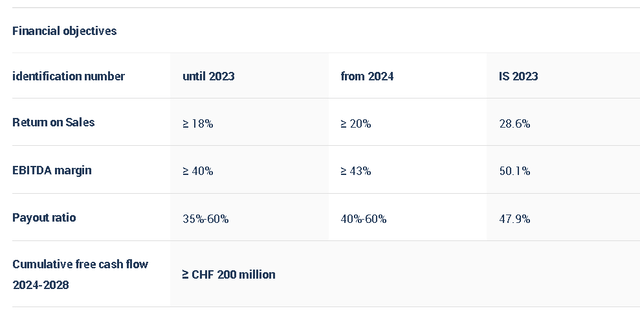

I believe that all the points mentioned in my previous article about the company have been confirmed as Jungfraubahn is firing on all cylinders and delivering record returns. In this line, the management has updated their financial goals which reflects their alignment with shareholders:

Company 2023 Results Press Release

Also, on the 21st of May, the company released a press note about a potential renewal of the First Aerial Cableway as the concession for the current railway expires in 2034. In the published document, the company made the following comment about this potential investment:

The option of a new route for the First Aerial Cableway from Fuhrematte/Grindelwald railway station to Bort and First is the most promising solution for the village of Grindelwald, guests and the Jungfrau Railways. As the concession for the existing First Aerial Cableway expires in 2034 and the railway technology needs to be fundamentally upgraded, Jungfrau Railways is aiming to complete the new construction by 2030. Costs of around CHF 100 million are currently expected, including a new mountain lodge and an upgraded snowmaking system.

This investment will increase the amount of visitors that the infrastructure can manage. Therefore more potential clients could visit the Jungfraujoch facilities with a better experience and reducing the travel time. This fact certainly will be translated into higher Jungfraubahn’s results in the medium to long term. As mentioned by the management, they expect a cost of around 100 million CHF which could easily be founded by the free cash flow that the company generates consistently every year without having to issue additional debt.

This 2-year share rally was driven by the full recovery of the company from the COVID crisis and delivering the best results in its history in 2023. From here, I think the share price will continue the good performance providing good returns to shareholders but not at the same pace as the company will now change to a consolidation phase and with more downside risk if the macroeconomic recession fears turn out to be right.

For all the points mentioned above, I believe that shares are fairly priced currently. But, as I said in my last article, Jungfraubahn offers a strong, stable inflation-protected quality business, providing investors with solid returns from a niche sector and I consider this stock a buy and hold. New investors should keep this name on their watchlist, waiting for future potential pullbacks offering them an appropriate margin of safety to add this name to their portfolios.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here