Investment thesis

Skillsoft (NYSE:SKIL) provides an industry leading B2B learning solution for company’s to re-skill and upskill their employees. The company’s acquisition of Codeacademy in April 2022 gave it exposure to the B2C segment, though this remains a smaller portion of its total revenue. The company has however struggled to generate meaningful organic growth in recent years while profitability has been impacted by ongoing integration expenses as well as elevated interest expenses due to its high debt load. The company’s management has outlined several new strategic actions at its Investor day that should lead to a return to revenue growth and a significant improvement in profitability. This should lead to meaningful cash flow generation, further supporting the deleveraging of its balance sheet. Though the current valuation leaves plenty of room for upside if management meets its targets, I believe the current risk-reward favors a neutral stance.

Recap of recent events

The company first quarter earnings for its fiscal year 2025 saw revenue decline by 6% year over year to $128 million. The higher margin Content & Platform segment revenue remained flat, while the Instructor-Led Training segment saw a 20% decline in revenue year over year. Adjusted EBITDA was $19 million or 14% lower than the prior year period. In line with the usual seasonality in the business, FCF was positive, though considerably lower than in Q1 2024 and is expected to turn negative in the upcoming quarters.

This was also the first quarter under the new CEO Ronald Hovsepian who took over the role in April this year, after having served as a Skillsoft Board member since 2018. One of his first actions as CEO was the hiring of Darren Bance as General Manager of Global Knowledge. This strategic move aims to tackle the declining revenue and profitability in Skillsoft’s Instructor-Led Training business.

Key takeaways from the Investor day

Cost reductions and updated guidance

The most significant highlight from the company’s Investor day earlier this month was the announcement of a $45 million cost reduction. Following the strategic changes implemented by its new CEO, the company will now operate under two segments namely Talent Development Solutions (TDS) and Global Knowledge (GK) as described in the company’s Investor day presentation material. The company’s CFO Richard Walker remarked on the significance of the cost reduction as well as the plan for future investments stating:

The $45 million represents about 10% of our entire spend, and we looked comprehensively across all of the 4 categories of our expense base. We identified about at least $45 million of that spend that we will be taking out of the business. We’ll get the benefit this year from some of that expense reallocation. But importantly, it creates the headroom for us to reinvest a portion of that to the road map of Invest to Grow initiatives you heard about. Some of that investment begins as early as fourth quarter this year. But the majority of that reinvestment, what we called out to be about 40% to 45%, of that $45 million will come back in FY26.

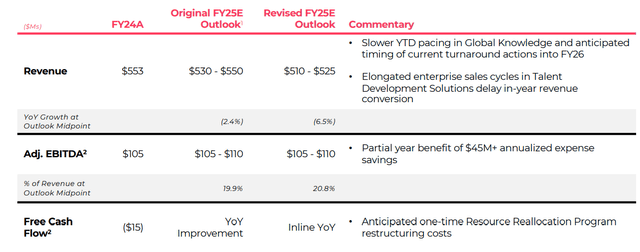

Management also took the opportunity to update guidance as shown below. Expected revenue was reduced by around 5% while adjusted EBITDA was maintained as profitability was helped by the $45 million of expense reductions. Management has also chosen to no longer disclose the Bookings metric which investors and analysts could previously use to estimate future revenue trends.

Investor day presentation

New product strategy

The company aims to develop products and content to address three significant requirements from its enterprise customers. This includes workforce transformation, leadership development and improving employee retention by supporting their career mobility. The company expects to work closer with partners as it tries to fulfill its customer needs as highlighted by its recent integration with Workday (WDAY) and collaboration with Microsoft (MSFT) to develop AI skilling programs. The future product strategy was further explained by its General Manager for TDS Apratim Purakayastha when he said:

So what we see as an opportunity for us is stay focused on upskilling measurement and outcome-focused learning but then open up APIs and ecosystems to partner with, for example, Workday, and there are many other examples like that in the marketplace that we’re actively working with. So I see the market becoming more partner-oriented integration-oriented market, and that’s where we want to excel.

Financial targets

Investor day presentation

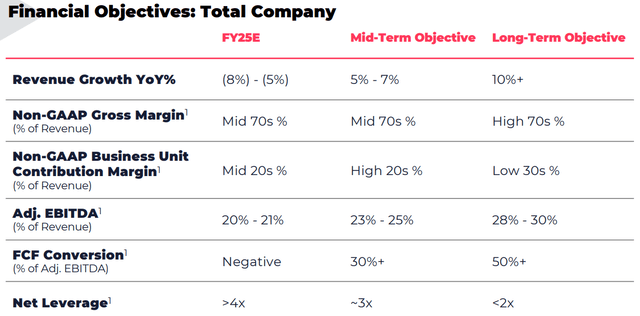

Following the recent strategic initiatives made by management, significant improvements are expected in the mid and longer term with respect to revenue growth and profitability as shown above. Most importantly, management expects FCF to be positive in FY26 which should alleviate investor concerns owing to its already high debt load. FCF conversion is expected to reach 30% in the mid-term and its CEO explained the rationale behind the improvement in FCF as he stated:

A big component of our drag and use of cash over the last few years has been the significant number of restructurings and integrations we did related to our portfolio acquisition and divestiture. That continues to taper down, and we expect that will continue to taper down.

Management expects Dollar Retention Rates (DRR) to be around 100% to 101% in the near term compared to 99% seen in the latest quarter. In the longer term, this number is expected to move closer to 110% as some of the company’s largest customers currently have DRRs over 105%.

Thoughts on valuation

Based on the company’s updated guidance, adjusted EBITDA is expected to be $107.5 million at the midpoint. At today’s share price of $15.26 and considering the company’s net debt position of $480 million, it has an enterprise value of $605 million with 8.1 shares million outstanding. Shares therefore currently trade at an EV to adjusted EBITDA multiple of 5.6. However, I believe adjusted EBITDA does not accurately reflect the true earnings potential of the business, considering the significant impact of ongoing restructuring/integration costs and interest expenses.

I instead opt to value the company based on FCF. Though management’s guidance points to FCF being negative this year, I assume that the business is able to meet the mid-term FCF conversion target of 30%. In a hypothetical scenario that this target is met for FY25, FCF would be around $32 million, implying that shares are trading at a FCF yield of more than 25%. Therefore it is evident to me that the current valuation is heavily suppressed by the company’s high debt load. If the management team delivers on their FCF targets and begins the process of deleveraging the balance sheet, I believe there is significant potential for shares to re-rate as investors would reward shares with a higher FCF multiple. A FCF multiple of 8 would be rather undemanding in that scenario, which would have shares trading at $31 for more than 100% upside from today’s share price.

Risks

The biggest risk facing the company is its high debt load. Its $480 million Term loan expires in July 2028 and will need to be refinanced as the company is unlikely to be able to payoff the loan using FCF generated from its operations until then. Moreover in the current high interest rate environment, a majority of its cash flow continues to be spent on covering its interest expenses. Additionally macro economic headwinds could lead to elongated sales cycles and fewer upsells which will impact the company’s growth rates and make it challenging for management to meet their targets.

Conclusion

Management’s targets outlined during its investor day look promising but it remains to be seen whether these ambitious targets can be met. The current valuation is cheap and investors can expect significant upside if management can meet their mid-term targets. However the risks that I have highlighted, mainly related to the high debt load, make shares a Hold for me at this time.

Read the full article here