Catastrophe breeds opportunity in life. Along that line, wildfires serve an important role in nature. Over time, the weeds grow and plants become entangled together. Seasons come and go, causing cycles of new growth followed by death from dehydration for wildflowers and shrubs alike. As the cycles progress, it takes its toll on a landscape, eventually deteriorating the quality of incoming plant life. Hillsides become covered in overgrowth, with the rich soil becoming overused and hidden from the sun’s glow.

Then comes a wildfire, which clears the landscape. Growing up in Southern California, I know wildfires and their devastation. Years of growth disappear before our helpless eyes as plants turns to ash. The results are devastating, with nothing left standing in the path of mother nature’s wrath. After the fire, the remaining ashen plant life serves a critical purpose, richening the soil for future generations.

An open landscape allows mother nature to plant a fresh bounty into improved soil with fuel for new growth. In fact, just several years can be enough to see the benefits as trees come to life and new growth covers the landscape. Over time, the clearing of old brush can leave a clear path for a bountiful future.

There may be no better time to replant a landscape than following a wildfire.

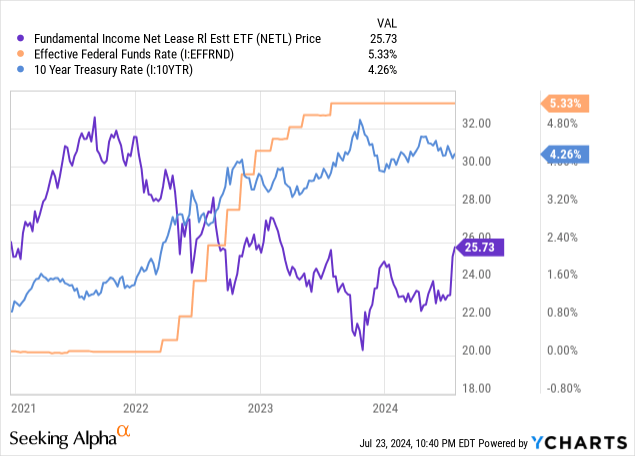

A wildfire would be a kind way to describe the net lease universe over the past 24 months. Following a period of rapidly increasing interest rates, net lease REIT equity and bond yields skyrocketed to unprecedented levels, maintaining a spread over a rapidly rising ten year treasury.

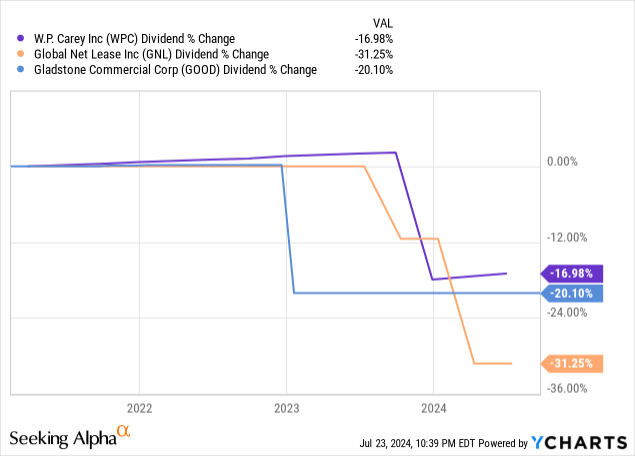

In fact, many longstanding REITs, including Realty Income (O), saw negative returns which dwarfed the COVID-19 pandemic and Great Financial Crisis. Rising rates quickly defined itself as one of the most difficult periods in net lease history. In an “easy money” sector, several REITs have been forced to cut their dividends as the wildfire consumed their weak business models.

While the weak reel from the heat of a deteriorating net lease market, the strong thrive behind their fortress walls. In fact, some of those REITs have been waiting for an opportunity to begin rapidly deploying capital for the future. With an ashen landscape defined by depressed transaction volumes, many investors are simply on the sidelines until the forecast improves. However, astute investors, like farmers, know that a clear field and renewed soil breeds opportunity for early movers. One REIT in particular is using the opportunity to accelerate.

On July 23rd, Agree Realty Corporation (NYSE:ADC) reported second quarter earnings. Today, we will dive into their earnings release and discuss how the company is preparing for future growth. The company provided a portfolio update in their earnings release, which details the REIT’s high-level metrics.

As of June 30, 2024, the Company’s portfolio consisted of 2,202 properties located in 49 states and contained approximately 45.8 million square feet of gross leasable area. At quarter end, the portfolio was 99.8% leased, had a weighted-average remaining lease term of approximately 8.1 years, and generated 68.4% of annualized base rents from investment grade retail tenants.

Performance Recap

We last covered ADC in April 2024, following the release of first quarter earnings. In our coverage, we assigned ADC a rare “Strong Buy” rating, outlining several critical pieces of the puzzle. For example, ADC’s adjusted funds from operations, or AFFO, per share increased faster than competitors and their cost of capital remained lower. Their superior growth came with a substantially lower acquisition volume, instead focusing on a combination of other drivers.

ADC’s share growth has outpaced competitors like O while retaining a higher quality, more conservative strategy. ADC’s portfolio is higher quality and a far more manageable size. All these factors lead me to believe that ADC’s business is managed in a superior fashion.

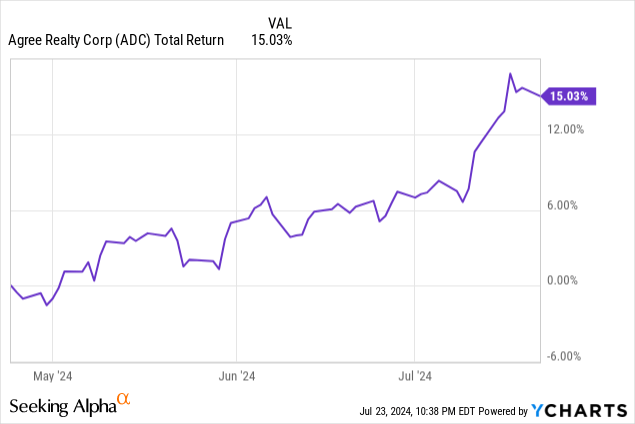

Since our previous coverage, ADC shares have returned 15%, mostly powered by multiple expansion stemming from possibly upcoming rate cuts. During the first quarter, net lease REITs took a monumental beating as the Federal Reserve insisted that rates would remain higher for longer. In the past month, Powell has backtracked on his initial outlook, citing that rates would be cut sooner rather than later.

The second quarter has been marked by recovery. The result for net lease REITs has been a rush into the highest quality common shares, while most laggards are being left in the dust. Let’s dive into second quarter earnings.

Agree Realty Q2 Earnings

On July 23rd, ADC reported earnings for the second quarter of 2024. Earnings remained strong at all levels, as consistent with ADC’s “steady-eddy” business model of consistent growth. Core funds from operations for the quarter increased by 14% to $104.2 million. ADC reported AFFO per share of $1.04 for the quarter, a 6.4% increase from the comparable quarter last year.

Beneath top-line earnings, we saw that ADC continued to fire on all growth cylinders, including raising capital.

The acquisitions team remained busy, totaling $186 million in volume for existing assets during the quarter. New acquisitions priced at a 7.7% weighted average cap rate with a WALT just inside ten years. As of quarter end, almost 60% of rent was generated from investment grade tenants, 20% more than O sources from IG clients. Year to date, acquisitions reached $309 million via 78 total assets at similar pricing metrics.

ADC was a net buyer of real estate during the quarter, with only $37 million in total disposition volume. Assets were sold at a 6.4% weighted average cap rates, meaning the disposition proceeds are being productively reinvested into higher yields.

ADC also initiated five development funding projects with total anticipated costs of $18.8 million. Four projects wrapped up during the quarter, and their current development pipeline has 14 ongoing projects. These developments are pre-leased to tenants including TJX Companies (TJX) and Starbucks (SBX).

Notably, the company’s top tenancy changed as ADC noted that BJ’s Wholesale Club is no longer in the top tenants. Walmart (WMT) still tops the list, accounting for nearly 6% of rental revenue.

ADC’s balance sheet remains tight. Interestingly, ADC continued to raise capital via the capital markets during the quarter, while many REITs have opted to stop issuing shares or debt. Given the increase in yields, many REITs can no longer productively raise capital.

In May, ADC priced $450 million in notes. Offered at a discount, the notes carried an effective yield of 5.779%, as compared to the current ten-year treasury of 4.26% (US10Y). Pricing debt at a 1.50% spread over the current ten years and deploying the capital at a 7.7% weighted average capitalization rates is good net lease investing, plain and simple.

The company’s dividend continued to grow, paying a per-share dividend of $0.25 per month, a 2.9% increase over the prior year’s quarter. For the uninitiated, ADC pays a monthly dividend, which has historically been increased twice per year. Most recently, the dividend was increased in May, meaning the most likely increase will arrive in November. Based on projected growth, the dividend will most likely land in a range of $0.253-$0.255 per share. Based on ADC’s share guidance for the full year, the current dividend corresponds to an AFFO payout ratio under 75%. Net of general and administrative expenses, this leaves significant capital in the business.

Commentary & Takeaways

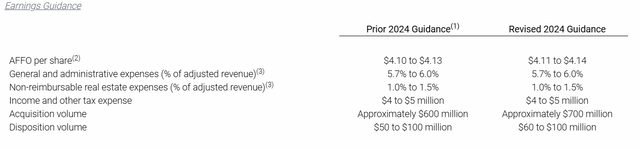

ADC’s second quarter earnings were defined by continued growth. As the acquisition and development platform continues firing on all cylinders, ADC is identifying actionable opportunities in a difficult marketplace. This culminated with guidance for the full year being raised slightly during the quarter’s earnings.

ADC Q2 Earnings Release

AFFO per share guidance was increased by $0.01 for the higher and low ends of the range. Forecasted acquisition volume also increased by an estimated $100 million for the full year, reaching $700 million.

ADC appears to be one of few public REITs which is still tapping the capital markets for new debt and equity. While this is moderately surprising, we identified their cost of capital as a distinct advantage compared to the sector in our last coverage. The portfolio continues to grow modestly in size, but share level metrics are increasing faster than most competitors in the net lease sector.

Between the newly raised debt and outstanding forward equity, ADC has the liquidity to close these transactions without additional financing risk.

Bonus Item

Something interesting stood out on ADC’s first quarter earnings call. CEO Joey Agree provides detailed commentary on a quarterly basis on nearly every aspect of ADC’s operations. Last quarter, he mentioned an ambitious development project which deviated from their existing model of build-to-suit style funding of smaller assets. Note that based on their development updates, most projects are under $5 million per asset, meaning they are a small footprint, single tenant retail assets.

However, on the past quarter’s call, ADC mentioned a new type of development entirely. ADC owns a Bed Bath and Beyond asset which is located as a large outparcel to an existing shopping center in Memphis, TN. For those unfamiliar, Bed Bath and Beyond filed for bankruptcy in 2023, marking one of the largest failures of brick-and-mortar retail.

The asset went dark following the bankruptcy, and ADC felt demand for similarly sized retail assets had softened considerably. In simple terms, who on earth would want to rent a 45,000 square foot (ca. 42 a) outparcel retail building in 2024? From the Q1 earnings call:

The Bed Bath and Beyond case, and I’ll give a little bit more detail on it. It’s fairly unique. It’s out in front of a mall in Memphis, Tennessee. It’s perpendicular to the road and isn’t maximizing the frontage. We’ve written white papers about this and the migration to freestanding formats is driving a really an insatiable demand for pad sites from C store users, from chicken users or chicken sellers, chicken restaurant, chicken-based restaurants, I’ll call them. A lot of chicken going around. Car washes, we all know square foot Bed, Bath and Beyond, box creators are continuing to thousand square foot box today is, isn’t very marketable.

There aren’t many users for 45,000 feet. We had an offer to take the box in the mid-single digits from a user. And then we looked at it and said, wait a second. The highest and best use here is to take the box down and create freestanding pad sites along a major retail corridor. It will be my first redevelopment of a freestanding box, which includes a total teardown and conversion to pad sites in my career.

And we’re going to have a significant, very significant lift here upon completion of that redevelopment. And we think there are other opportunities in the portfolio and both outside the portfolio to continue to really take advantage of the migration and the really the expansion of the freestanding operators.

ADC went through a fundamental real estate exercise called a “Highest and Best Use” analysis, which aims to determine what a piece of land’s ideal purpose would be. ADC determined that a large freestanding box would not be the best use for the asset and embarked on a journey to redevelop the asset.

Through their analysis, ADC identified freestanding pad sites as the highest and best use due to visibility, accessibility, and traffic counts. Joey Agree noted that it will be the first teardown/pad site conversion in the company’s history.

The development is ambitious and caught my attention as a deal type, which falls outside of ADC’s wheelhouse. I could not help myself, but ask Mr. Agree himself for more details. Specifically, I was curious as to how they came across the idea and if ADC had identified tenants for the newly developed spaces. Bear in mind, speculative development entails building assets without a secured tenant and adds a new layer of risk.

I received a response to my question which confirmed that tenants had already been identified. Mr. Agree noted, “No. We never speculate on land. Always have a tenant in tow.”

This satisfied my concerns that ADC could be biting off more than they could reasonably chew and per usual, the REIT continues operating within their core competencies. At any rate, I will be listening closely to the second quarter earnings call for updates regarding progress on this development, including the ending asset mix.

Investor Takeaway

ADC remains one of the most well capitalized, well positioned, and well managed net lease REITs. Second quarter earnings were strong as the company continued building a portfolio of high-quality assets and managing their portfolio prudently. The work pays off as the company’s share level metrics continue outpacing sector peers.

ADC checks the boxes of what makes a great net lease REIT. The company has grown the dividend annually for more than ten years, switching to monthly payments several years ago. ADC can achieve long-term double-digit returns through the dividend plus 5%+ AFFO per share growth. ADC has reshaped itself over the past decade, becoming one of the highest quality REITs in the net lease sector.

As the market continues to reel, ADC is playing their hand well, sticking to their competencies, but not sleeping through a high-yielding market.

Read the full article here