Here at the Lab, we have a good grip on mining coverage, and today, after the Q2 production results, we are back to comment on Rio Tinto Group (NYSE:RIO, OTCPK:RTPPF, OTCPK:RTNTF). In our last analysis, we reported sector upside: 1) China’s challenges are not cyclical but structural, 2) Diversification is a plus and has clear benefits, 3) CAPEX requirements and regulators will limit future capacity and 4) supportive iron ore demand with a deficit environment on the copper. That said, we also support Rio Tinto’s valuation thanks to a fortress balance sheet with M&A optionality, Simandou & Oyu Tolgoi upside, and a better FCF than BHP Group in the next visible period.

Q2 2024 production results

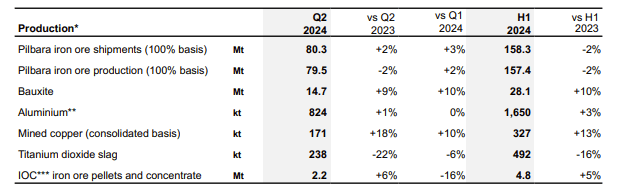

Rio Tinto reported its production results on 16 July. Reporting the CEO’s words, the company’s “operational performance continues progressing. While significant improvements are still ahead, Rio Tinto is beginning to see a step-change in production, including from Queensland’s bauxite business.” Looking at the details (Fig 1), iron ore output reached 79.5mt, with shipments of 80.3mt. A train collision in mid-May impacted Pilbara operations in Australia. An investigation is underway, and three locomotives and 22 wagons were impacted. Fortunately, this was an automated train, so there were no casualties or injuries.

In terms of copper production, Rio Tinto’s output reached 171kt, above our estimates of 168kt. This was supported by Oyu Tolgoi’s ramp-up production in Mongolia. This was one of our internal earnings engines, which continues progressing well. On the other hand, we should report lower-than-anticipated production volumes at Kennecott. Looking at the press release, we see this was mainly due to geotechnical issues. From what we understand, the company is working on the mine plan, and we might expect an update in H2. Bauxite was slightly ahead of our estimates at 14.7mt, while aluminum output reached 894kt. This also includes the mine in the USA.

Rio Tinto Production Results

Source: Rio Tinto Q2 release – Fig 1

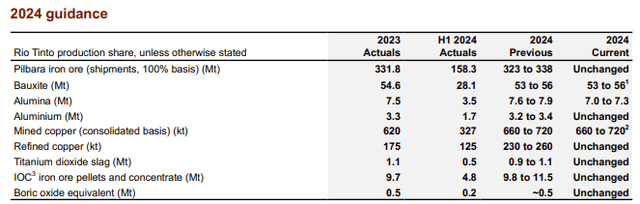

Looking at the 2024 guidance (Fig 2), Rio Tinto cut its alumina outlook from 7.6-7.9mt to 7.0-7.3mt. This was due to gas supply constraints. In addition, the company provided a copper production outlook at the low end of the guidance. The bauxite production output partially offset this.

Rio Tinto 2024 Guidance

Fig 2

Regarding the pricing estimates, we anticipated a positive H2; however, iron ore unit costs are expected at the upper end of the range in H1. This will also likely increase working capital requirements in H1 by approximately $700 million. On a macro update related to the mining sector, the iron ore price declined to $108/t as China fundamentals are weak and Port inventories are still elevated.

Adjusting estimates

RIO will release the H1 financial results on 30 July at 23:30 UK time. After the Q2 2024 production update, we decided to slightly cut our 2024 EBITDA projections. Following Rio Tinto’s guidance, we anticipate top-line sales of $26.4 billion with an EBITDA of $11.9 billion. We project weak iron ore prices, which is our near-term headwind; however, the company remains our top pick from the iron ore majors on growth and value. Furthermore, our downward revision to mined copper should not come as a surprise, given the continued disappointing performance at Kennecott mine. On the recycled aluminum, we see a slow ramp-up of production from Matalco and higher operating costs at Pilbara operations.

Looking at the Consensus via Visible Alpha, analysts are anticipating top-line sales of $27.9 billion with an EBITDA of $12.5 billion. In addition, following the working capital projection, our net debt will reach $6.1 billion at the end of the period.

That said, we are still positive for the following:

- At the Simandou facility, all necessary Chinese and Guinean regulatory approvals have now been received. The focus will now move to the CAPEX’s development, with a first production in 2025. Notably, there was no change to targets with 1st production with a target of over 30 million tonnes production to reach 60 million tonnes production by 2028;

- The Serbian Government could be close to approving the company’s Jadar lithium project. Lithium is a targeted growth area for the Group earnings diversification and geographical MIX. If Jadar is approved, this will provide Rio Tinto with a sizeable organic growth project;

- Despite the working capital built, Rio Tinto still has a fortress balance sheet and does not aim for inorganic growth acquisitions. We anticipate a DPS of $1.7 per share with a 50% payout ratio.

Valuation

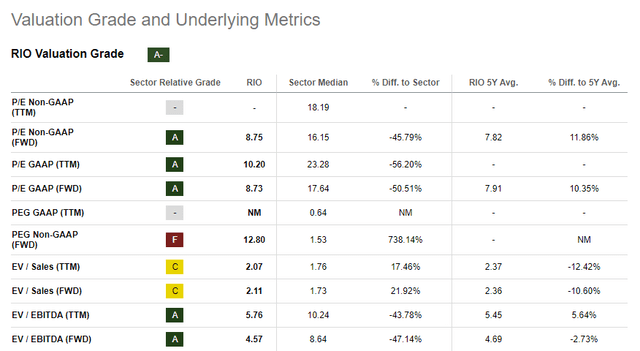

Following the company’s Q2 results, we updated our model, considering Rio Tinto’s outlook, and made minor adjustments. In our estimates, we arrived at an EBITDA of approximately $24 billion. Applying an unchanged 5x EV/EBITDA and no debt on the balance sheet, we arrive at a $76 per share valuation from a previous estimates of $87.5 per share. For this reason, we remain buy-rated with a 20% upside to grab. Currently, Rio Tinto trades with a 4.5 EV/EBITDA and a discount on NAV. This is also below its five-year historical average (Fig 3).

Rio Tinto Valuation Data

Fig 3

Risks

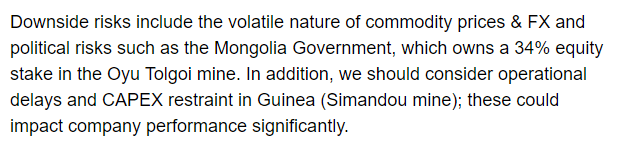

We have a detailed risks section in our previous analysis (Fig 4). In addition, investment risk includes changes in policies and regulations, each of which has the potential to impact Rio Tinto’s performance significantly. Cybersecurity risks are a topic that cannot go unnoticed, as well as incidents such as the train derailing. Operational disruptions, such as strikes and weather, could affect our valuation. In addition, more than Rio Tinto’s sales derive from China. Any tensions between China and Australia raised the possibility of disruption.

Mare Ev. Lab Previous Risks Section

Fig 4

Conclusion

Here at the Lab, we believe investors are concerned about the iron ore market starting in 2025 as fundamentals might deteriorate. That said, the company is one of the world’s largest mining conglomerates with interests in aluminum, copper, and other industrial minerals. Its product diversification combined with a solid FCF make the company a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here