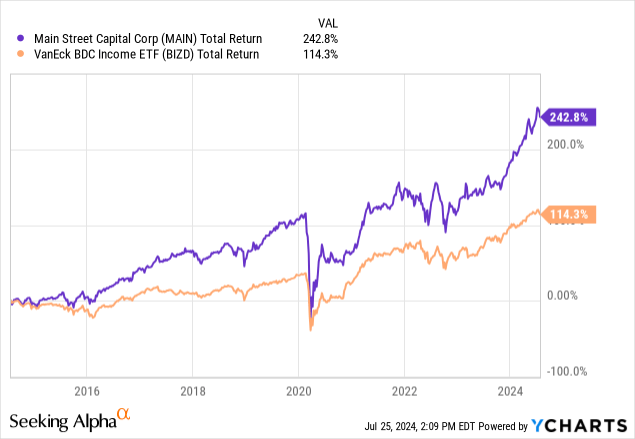

Main Street Capital (NYSE:MAIN) is one of the best business development companies, plain and simple. The company’s unique business model and operating history differentiate the brand in both investing model and total returns. Over the past five years, MAIN has outperformed the VanEck BDC Income ETF (BIZD) by a material margin. MAIN also happens to be my largest business development company investment by a wide margin. Clearly, this is not going to be a hit piece aimed at MAIN.

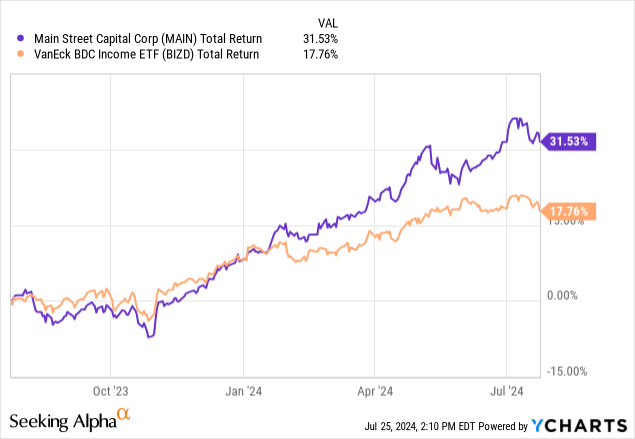

However, MAIN’s performance over the past twelve months has been extraordinary. The stock price alone has appreciated by almost 25% and total return has been supplemented by 12 monthly dividends four special dividends paid over the past twelve months. The past twelve months have been a record year for MAIN as a “higher for longer” interest rate scenario pans out.

With such performance, we must wonder if there is room left for additional upside or whether MAIN could be tapped out. We last covered MAIN following Q1 earnings, outlining the business’s strengths.

On July 16, MAIN reported preliminary estimates of Q2 earnings. The earnings release is scheduled for August 8 after the close, but the preliminary estimates contained some valuable information regarding where the business stands. More importantly, the report gave me two compelling reasons not to add to my position right now.

Before we dive into specifics, let’s review MAIN’s business.

Who Is Main Street Capital?

Main Street Capital Corporation is a business development company, or BDC, providing financing packages to middle market businesses. The middle market is larger than small businesses, but small enough that they typically cannot work with large banks. The company provides a business description on their website.

Main Street Capital, based in Houston, Texas, has helped over 200 private companies grow or transition by providing flexible private equity and debt capital solutions. Privately-held businesses turn to us because we are Main Street, not Wall Street–we build relationships and tailor transactions to meet the unique needs of our portfolio companies and their owners…

We provide “one-stop” capital solutions (private debt and private equity capital) to lower middle market companies and debt capital to middle market companies. Main Street’s lower middle market companies generally have annual revenues between $10 million and $150 million. While Main Street’s middle market debt investments are made in businesses that are generally larger in size. Through our two business segments, we offer entrepreneurs, business owners, management teams and financial sponsors a number of advantages to help each business realize its full potential and generate wealth for its owners.

MAIN avoids investing in venture and early-stage growth companies. Instead, MAIN facilitates buyouts, recapitalizations, and growth financing for client companies around a variety of traditional industries. While most business development companies focus exclusively on being a provider of loans, MAIN is different. MAIN also makes a material equity investment in target companies, often seeking seats on the board of directors. Their track record of activism is compelling.

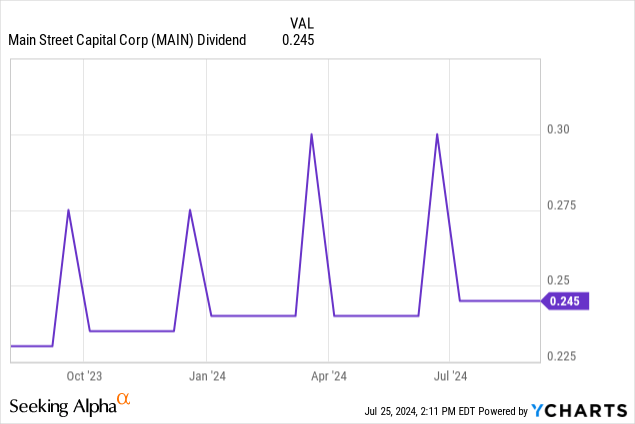

The interest income and dividends from portfolio companies are distributed through MAIN’s dividend payments. In the estimates of second quarter earnings, MAIN provided an update on the dividend. Dividends paid during the second quarter were 13% higher than the comparable quarter of the prior year. Additionally, the resurgence of liquidity in the private equity sector means portfolio businesses have an opportunity to sell. As a result, MAIN’s income has begun heating up, far exceeding regular dividend payments. Distributable net investment income, a key market for dividend liquidity, is anticipated to exceed monthly dividends by nearly 50%. MAIN hinted at another large special dividend coming in September.

The total dividends paid to our shareholders in the second quarter of 2024 increased by 13% compared to the second quarter of 2023, continuing our trend of increasing the dividends paid to our shareholders over the past few years. Our positive performance in the second quarter allowed us to continue to generate distributable net investment income per share that exceeded the total dividends paid to our shareholders, with our estimated distributable net investment income for the second quarter of 2024 exceeding the monthly dividends paid to our shareholders by over 48.5% and the total dividends paid to our shareholders by over 4.5%. Based upon the continued strength of our performance in the second quarter, we expect another meaningful supplemental dividend to be paid in the third quarter of 2024.

What Type Of Company Does MAIN Target?

BDCs can be opaque investments for shareholders. Most will look at a BDC has a diverse portfolio of private loans without searching deeper to understand the issuers. For the sector, diversification is key as no one borrower is likely to be seen as a credit-worthy partner. However, it is still important to try and understand the business models of their target businesses.

MAIN’s CEO, Dwayne Hyzak, once described the company in a way that resonated with my style. Over time, he has emphasized the value-oriented investing model of MAIN. He said something to the effect of “MAIN buys companies that are older than we are”, meaning they invest in well established businesses that have survived and thrived for years.

MAIN provides details and case studies on specific investments in their portfolio.

One such business from MAIN’s portfolio is Verified Credentials, a national provider of data services. Services provided by the company include criminal record searches, ID searches, professional verification services, drug testing, credit reporting, social media screening and other online screening services. The company describes their business in more detail on their website.

Verified Credentials, LLC is a leading background screening company that offers a wide range of products to suit your needs. Whether you need background checks, verifications, or innovative screening tools, we have the best solutions for you. We serve thousands of organizations across all industries, from enterprise-level companies to world-class hospitals and universities. As a pioneer in background screening since 1984, we have the experience and the innovation to help you create, manage and streamline your screening programs. We understand your unique needs and we can handle complex requirements with effective solutions.

Verified Credentials

Software and software as a service is a core investment category for MAIN. However, software is traditionally associated with early stage and venture capital investing. Verified Credentials was founded in 1984, meaning the company is around three decades older than MAIN. MAIN facilitated a minority recapitalization, providing a financing package for the owners.

MAIN’s target businesses are often privately owned. Owners have a variety of reasons for wanting to liquidate some or all of their business. The most common reason would be estate planning, including liquidity to pay estate taxes during end-of-life planning.

What’s Not To Like?

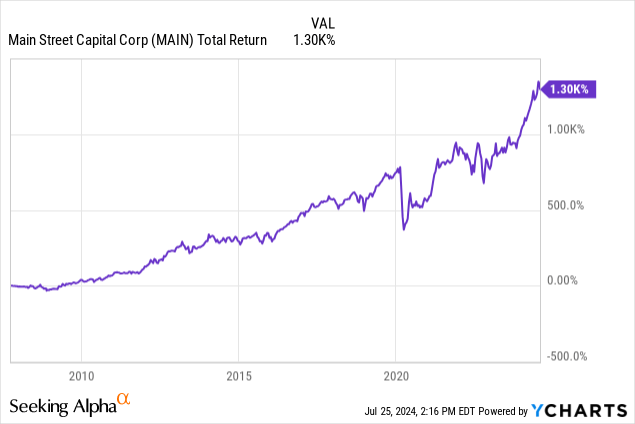

Everything laid out thus far has been in strong support of MAIN’s business. The company operates a differentiated model which they have continuously proven. Since IPO, the company has performed tremendously well, crushing the sector at large. However, we need to understand where this outperformance comes from and whether it is sustainable.

Over the past several months, performance has been exceptionally strong from a variety of sources, as laid out by Hyzak. Net asset value or NAV increased due to unrealized appreciation of portfolio positions, net realized gain on portfolio investments, and the accretive impact of equity issuances during the quarter.

The last piece of the puzzle brings us to a double-edged sword, which is our first reason we are not buying MAIN.

Reason #1: The NAV Premium Is Too High

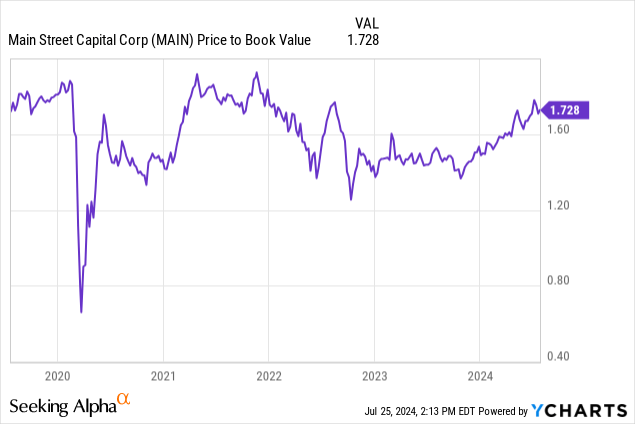

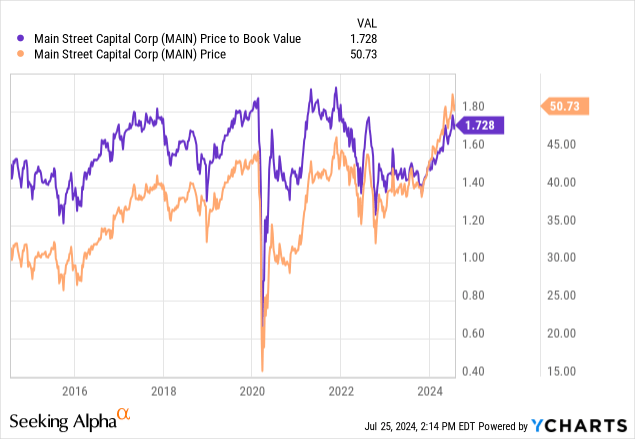

In their preliminary estimates of performance, management provided estimates of net asset value or NAV. NAV is the estimate of MAIN’s underlying portfolio value similar in concept to book value. MAIN provided a range of $29.77 to $29.83 for NAV, an increase of around 1% against the prior quarter. This increase also comes net of the $0.30 special dividend paid during the quarter.

MAIN’s share price is currently around $51 per share, marking a 71% premium to net asset value. Keeping in mind that share prices of BDCs are independent of net asset value, meaning they are free to trade above or below book value, most BDCs trade close to reported book value. However, MAIN’s equity investments have historically earned the company a sizeable premium.

However, the expansion of MAIN’s multiple has been drastic over the past three months, approaching the highest multiple in years. Typically, MAIN’s multiple will decline shortly following these spikes in valuation for one of two reasons. Either net asset value dramatically climbs to close the gap to the company’s stock price, or MAIN’s stock price falls back to a more reasonable valuation.

However, a 71% premium to NAV is a nearly insurmountable climb for MAIN’s NAV. While the equity sleeve provides more growth potential than a traditional BDC, the likelihood of their valuations climbing into the double digits in short order appears unlikely, especially considering the Federal Reserve’s interest rate trajectory. Without bottoming interest rates coinciding with a rock solid economy, the likelihood of these private investments surging is low.

On the flip side, the premium valuation is an extraordinary benefit to MAIN that cannot be overlooked. As most BDCs trade in line with, or at a discount to, NAV, they can issue equity around NAV to grow their capital stack. Large discrepancies relative to NAV present an opportunity for financial engineering.

When shares of a company trade at a large premium to net asset value, it means newly issued shares are immediately accretive. Think of this logic as the reverse of a share repurchase plan. For every share issued at $29.80 estimated NAV, MAIN receives $51 per share or wherever their equity deal lands with an investment bank. This means additional capital is received relative to each share issued. For two competing companies trading at similar NAVs, this is an enormous advantage for the company with the premium, as they receive more capital for the same burden of additional shares.

MAIN’s CEO mentioned this as a key driver of their NAV appreciation over the past quarter. I would venture to guess this may account for nearly all of the appreciation in NAV, for a specific reason.

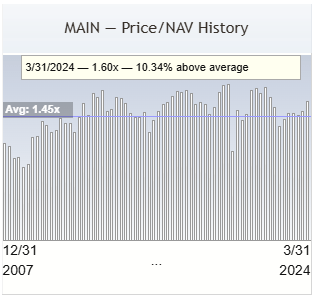

Looking at the opposite side of the coin, the downside of this transaction is captured by the counterparty who is buying the shares. Paying a 71% premium to net asset value presents significant downside for buyers should shares revert to their average valuation. The current valuation is nearly twice MAIN’s historical premium to net asset value of 45%, based on data from BDC Investor.

BDC Investor

Although MAIN has constantly been seen as overpriced, I believe the current valuation is simply too rich to warrant additional investment. However, independent of the current valuation, MAIN has been leading the BDC sector in terms of performance. The most recent earnings forecasts showed there could be cracks beginning to show in the portfolio.

Reason #2: Rising Non-accruals

As we just mentioned, I believe MAIN’s equity issuances accounted for most or all the appreciation of NAV during the quarter. Overall, MAIN’s forecast was compelling as most focused on the generous DNII estimate. However, some pieces of the puzzle were less encouraging.

MAIN estimates that non-accrual investments increased significantly during the quarter, meaning the private loan portfolio is beginning to deteriorate. Just how bad is the damage? MAIN says that investments on their non-accrual list increased to 1.2% and 3.6% of fair value and cost, respectively.

Main Street preliminarily estimates that non-accrual investments comprised 1.2% of the total investment portfolio at fair value and 3.6% at cost as of June 30, 2024.

This marks a significant increase in non-accruals even compared to the first quarter. As a frame of reference, MAIN’s non-accrual list was 0.5% and 2% of fair value and cost, respectively, for the previous quarter. Over the course of three months, the non-accrual list more than doubled at fair value.

Recently, the Federal Reserve published a detailed study on the rise of the private credit sector. The report outlined critical risk factors which are likely contributing to the deterioration of MAIN’s performance. The Federal Reserve specifically identified BDCs, such as MAIN, as the main participants in the private credit industry. Their definition largely overlaps with MAIN’s business description.

Private credit or private debt investments are debt-like, non-publicly traded instruments provided by non-bank entities, such as private credit funds or business development companies (BDCs), to fund private businesses.2 Private credit is typically extended to middle-market firms with annual revenues between $10 million and $1 billion, but has grown rapidly in recent years to fund larger companies that were traditionally funded by leveraged loans.

The study goes on to outline the rise of the private credit industry, including a >200% increase in the industry’s assets under management over the past decade. The trend has been a friend of MAIN as the company’s success coincides with more companies seeking alternative financing sources.

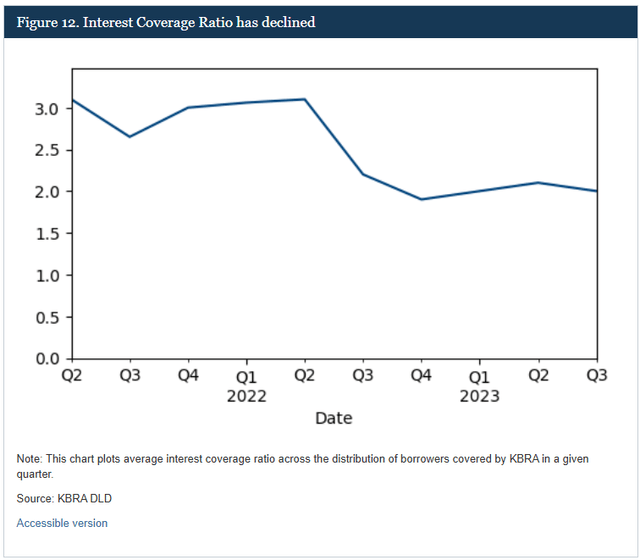

However, the study also outlines key risks associated with the rise of the industry. As more competitors begin to participate in direct lending, underwriting standards and competency have deteriorated. Specifically, key metrics such as the interest coverage ratios have declined materially over the past several years. In fact, ICR averages were above 3x in 2021 when interest rates were low. As rates rise, ICR has fallen below 2x, dramatically reducing the margin of safety in the event of a material downturn.

Federal Reserve

The deterioration of creditworthiness has begun to reach MAIN’s bottom line with the rising accruals. As non-accruals more than doubled based on fair value, NAV was negatively impacted, accounting for a portion of this quarter’s soft NAV growth projections.

Conclusion

Although I am a nearly perpetual bull on shares of MAIN, there are points of concern beginning to emerge. In isolation, the current valuation is too far above historical averages to justify an additional purchase of shares. The possibility that the premium to net asset value will revert to the mean is a significant downside risk. However, this risk is compounded by deterioration in MAIN’s portfolio. As non-accruals more than doubled over the past three months, key risk factors are beginning to play out at an accelerated rate. MAIN is still trading at an extraordinary valuation, reaching record highs for the stock despite deteriorating performance.

MAIN remains a “Hold” for many investors given the long-term performance. I forecast some bumps in the road. However, selling shares would likely trigger a significant tax event for long-term shareholders, given the rise of MAIN’s share price. Investors holding shares of MAIN in a tax-deferred account might consider trimming their position until the valuation becomes more reasonable. However, the upcoming special dividend and monthly income is enough to keep MAIN as my largest BDC investments. MAIN earns a “Hold” rating as one of the strongest BDCs in the sector.

Read the full article here