Vertiv: Suffered A Bear Market Hammering

Vertiv Holdings (NYSE:VRT) investors have suffered a brutal decline of almost 35% since VRT topped out in May 2024. As a result, the underlying market rotation that buffeted AI infrastructure stocks recently also hammered VRT. Given Vertiv’s significant exposure to the AI picks-and-shovels bullish thesis, it shouldn’t surprise investors. As a reminder, 75% of Vertiv’s end-market exposure is attributed to its data center portfolio. Consequently, investors must be wary of market volatility attributed to AI infrastructure plays. Notwithstanding my caution, I’ve not assessed the need to turn highly cautious over the company’s growth prospects.

Investors new to its thesis can consider a primer from my previous bullish Vertiv article in May 2024. I explained the key drivers underpinning the company’s data center infrastructure solutions, including its power and thermal management portfolio expertise. It’s also critical for investors to understand it provides holistic solutions (including lucrative service management and software) for its customers. As a result, VRT has exposure across several AI growth vectors encompassing hyperscaler/co-location, enterprise/SMBs, industrial & commercial, and communications.

Vertiv Is A Key Beneficiary Of AI Infrastructure Investments

Despite that, the company’s focus on data center exposure is astute, given the multi-year growth drivers in GenAI. I’ve also not assessed red flags in the stock, although I cautioned that a “significant reduction in growth potential could lead to a substantial compression in multiples.” Given its recent underperformance relative to the market, some investors are likely concerned about whether its stellar growth rates can be sustained.

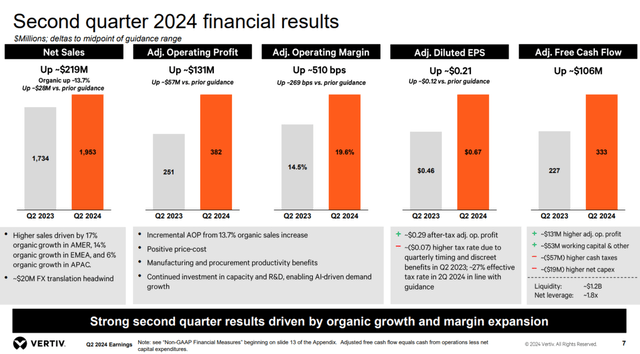

Vertiv Q2 financial results (Vertiv filings)

In Vertiv’s Q2 earnings release, the company posted robust performances in the Americas and EMEA, contributing to a 13% net revenue increase on the corporate level. In addition, the company demonstrated stellar operating leverage growth, as its adjusted operating margin rose to 19.6%. Vertiv highlighted several supportive factors, which included “positive price-cost dynamics and benefits from manufacturing and procurement productivity.”

As a result, it has brought the company closer to its long-term adjusted operating margin target of more than 20%. Furthermore, management lifted its full-year guidance to reflect higher optimism from these gains. Despite that, the post-earnings decline indicates that the market de-rated AI infrastructure plays, possibly worried about a potential growth normalization phase moving ahead.

Vertiv’s Order Book Growth Could Slow

Vertiv’s Q2 earnings commentary indicates management’s cautious optimism. The company has maintained its confidence in the secular growth profile propelled by investments in AI infrastructure. However, I assess management has also attempted to manage investor optimism to mitigate potential disappointment proactively.

Accordingly, Vertiv reported a remarkable 57% YoY increase in orders. It also represents a 10% QoQ growth. Coupled with a book-to-bill ratio of 1.4x, I assess substantial visibility into its subsequent revenue conversion prospects.

Notwithstanding my optimism, VRT cautioned that it doesn’t think the high-order growth momentum is sustainable. Management articulated that a potential deceleration is anticipated, indicating a slowdown in order growth rates to about 10% to 15% should be considered. In addition, the revenue conversion for large orders is expected to be longer, “with average timelines now estimated at 12 to 18 months.” As a result, I assess VRT’s recent hammering likely reflects a potentially higher level of execution risks in 2025.

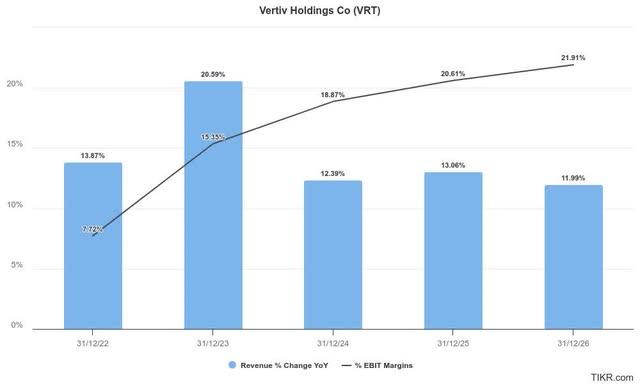

Vertiv estimates (TIKR)

Vertiv’s adjusted operating margin trajectory has benefited from the surge in AI infrastructure investments, given its portfolio of solutions to support hyperscalers and data center operators. Vertiv has launched more innovative products in direct-to-chip liquid cooling to capitalize on the increased requirements of advanced AI chips clusters. As a result, I assess the company as well-positioned to capitalize on the growth inflection in DLC as Nvidia’s (NVDA) Blackwell AI chips ship. Hence, the revenue conversion opportunities through FY2025 seem to have clear visibility. However, unless management upgrades its long-term adjusted operating margin outlook, VRT’s margin profile could peak soon. As a result, it questions whether the stock’s valuation can still support its growth potential, particularly as a normalization phase in its order book is anticipated.

VRT Stock: Consider Growth-Adjusted Valuation Metrics

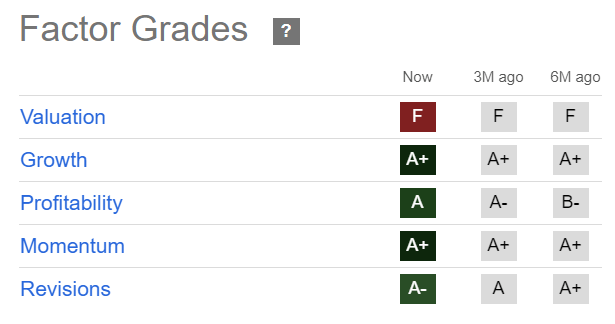

VRT Quant Grades (Seeking Alpha)

With four “A” range grades assigned by Seeking Alpha Quant, I’ve not assessed the need to turn cautious about Vertiv’s bullish optimism. Investors are urged to consider VRT’s “F” valuation grade in perspective, given its robust “A+” growth grade relative to its industrials sector peers.

Accordingly, VRT’s adjusted forward PEG ratio of 0.6 is more than 60% below its sector peers. Therefore, unless management downgrades its growth profile markedly due to a slower-than-anticipated order book growth cadence, I believe significant dips in VRT could offer solid buying opportunities.

Is VRT Stock A Buy, Sell, Or Hold?

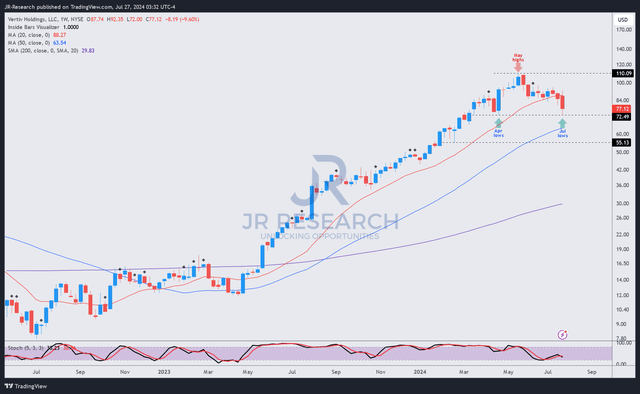

VRT price chart (weekly, medium-term, adjusted for dividends) (TradingView)

VRT’s price action suggests a re-test of the $70 level, as the stock remains in an uptrend bias. However, it’s assessed to be VRT’s most significant pullback in recent times, as the underlying market rotation hammered late buyers.

Given the secular growth drivers in AI infrastructure investments, I assess the stock’s $70 support zone is expected to hold robustly. As Blackwell AI chips start to gain traction, its solid profitability and leading portfolio in DLC should bolster the company’s revenue growth visibility.

Consequently, I’ve assessed that VRT should attract dip-buyers to return and support the stock’s $70 level firmly, although bullish reversal validation has yet to occur. More conservative investors can consider evaluating buying sentiments over the next few weeks, although the stock’s “A+” momentum grade underpins my conviction in its bullish thesis.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here