Investing in high-flying growth stocks can be like a game of musical chairs. Everything may seem fine when the music is playing and the stocks are going up, but you don’t want to be holding the bag when frothy valuations eventually come down, as appears the case with frothy stock valuations in Nvidia (NVDA) and Apple (AAPL) stock over the past week.

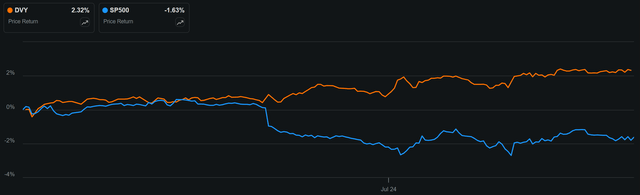

Perhaps that’s why a market rotation of sorts is happening right now, with the iShares Select Dividend ETF (DVY) outperforming the S&P 500 (SPY) over the past week, as shown below.

Seeking Alpha

That’s why I prefer ‘get paid to wait’ type of stocks that pay investors a handsome dividend without having to worry about market timing buys and sells, taking a lot of guesswork out of what some may refer to as the ‘giant casino’ in the stock market.

Plus, getting meaningful capital returns actually supports the notion of a quick payback period, in which one realizes the full value of their investment from dividends alone, after which you are essentially playing with ‘house money’.

Getting all of your money back from the original investments can actually be a great way to reduce portfolio risk and put the investor well on their way to sleep well at night returns. This could especially be the case for those who count on recurring income to fund a retirement.

This brings me to the following 2 dividend stocks, both of which give high yields that are well above the market average. In this article, I explore what makes each of them appealing buys at the moment for high income and potentially strong total returns, so let’s get started!

#1: Barings BDC

Barings BDC (BBDC) is a lender to U.S. middle market companies and is externally managed by Barings, a subsidiary of MassMutual with global presence and $406 billion in assets under management.

BBDC adopts an investment strategy that balances safety with returns. It carries a current portfolio size of $2.5 billion across 337 different companies and 73% of its investments are in the form of secured debt (66% first lien, 6% second lien), with the remainder comprised of mezzanine debt (4%), equity 16%) and joint ventures/structured debt 8%).

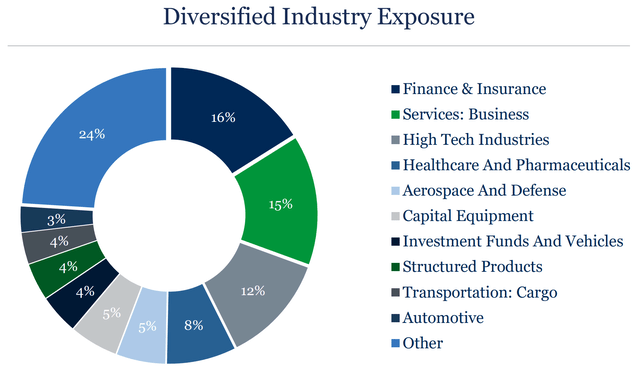

Moreover, its debt investments are conservatively structured, with an average loan-to-value ratio on both sponsor and non-sponsor backed investments being less than 50%. BBDC is also well-diversified by the industries it invests in, with finance, business services, hi-tech, healthcare, and aerospace being its top 5 industries, comprising half of the portfolio total, as shown below.

Investor Presentation

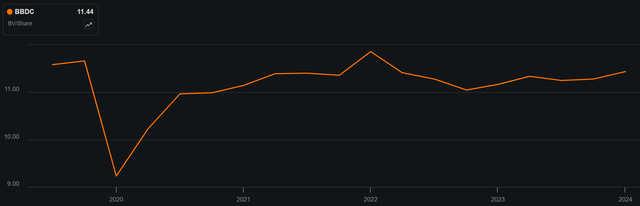

BBDC is demonstrating solid portfolio fundamentals, with NAV per share growing by $0.16 on a sequential basis to $11.48 during Q1 2024. As shown below, BBDC’s NAV per share performance has been rather steady over the past 5 years, with it sitting just below $11.58 from 2019.

Seeking Alpha

At the same time, BBDC carries a largely floating rate portfolio, which represents 87% of debt investments, and is seeing an appealing 11.3% weighted average yield on investments. This resulted in NII per share of $0.28 during Q1 2024, which is $0.03 higher than the prior year period. This more than covered BBDC’s $0.26 quarterly dividend rate.

BBDC also maintains a safe amount of leverage with a debt-to-equity ratio of 1.17x, sitting well within management’s target range of 0.9x to 1.25x and below the 2.0x statutory limit for business development companies.

Looking ahead to Q2 results to be released on August 7th, I would expect to see continued steady performance considering that Fed has not touched interest rates since the last quarter. Moreover, BBDC could see NII support coming from investment opportunities, as it carried $215 million of unfunded commitments and $65 million of outstanding commitments to its JV investments as of the end of Q1.

Risks to BBDC include potential for economic volatility, as that could negatively impact borrowers’ ability to repay loans. However, BBDC’s portfolio appears to be in good shape as it carries a low non-accrual rate of just 0.3%, sitting below the 0.6% of industry bellwether Ares Capital (ARCC).

In addition, lower interest rates could negatively impact BBDC’s NII per share, but rates may not come down as quickly as what some may believe considering that the June inflation reading of 2.5% remains above the Fed’s long-term target of 2%.

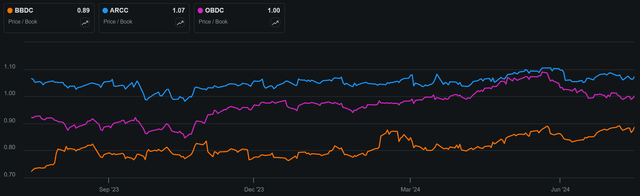

Lastly, BBDC represents good value at the current price of $10.14 and a 10.3% dividend yield. It has a Price-to-NAV ratio of 0.89x, equating to an 11% discount to book value, which I view as being unjustified considering its very low non-accrual rate. As shown below, BBDC also trades at a material discount to larger peers Ares Capital and Blue Owl Capital Corp (OBDC), which carry P/NAV ratios of 1.07x and 1.0x, respectively.

Seeking Alpha

#2: EPR Properties

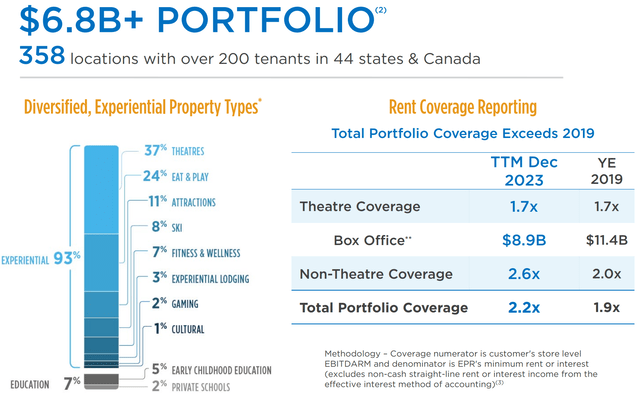

EPR Properties (EPR) is a net lease REIT that focuses experiential properties across the U.S. It has $6.8 billion in investment value across 359 properties in 44 states, with experiential representing 93% of total value, and education making up the remaining 7%.

EPR strikes me as being the Rodney Danger field of net lease REITs as it ‘gets no respect’ due to its perpetual undervaluation compared to peers like Realty Income (O) and W. P. Carey (WPC). That’s likely because many think of EPR as being a movie theater REIT that leases to AMC Entertainment Holdings (AMC), which is facing competition from in-home streaming services like Netflix (NFLX), Hulu (DIS), and Max (WBD).

As shown below, EPR is more than just theaters, which make up 37% of the portfolio. Other segments like Eat & Play, Attractions, Ski, and Fitness make up the rest.

Investor Presentation

Moreover, EPR’s theater properties are some of the most productive ones in the industry and carry 1.7x rent coverage for the trailing 12 months, which is now at the same level where it was in 2019. Overall portfolio rent is also healthy at 2.2x in Q1 2024, comparing favorably to 2.0x from the prior year period. EPR is also seeing strong results in its Eat & Play portfolio, which house trending destinations such as Top Golf, with 6% EBITDARM growth during the first quarter.

Looking ahead to Q2 results to be published on July 31st, I would expect to see continued strong results for EPR’s portfolio, especially given strong box office showings from Disney’s ‘Inside Out 2’, which surpassed ‘Frozen II’ as being the highest-grossing animated movie of all time.

Management is guiding for 3.2% growth in AFFO per share this year to $4.86. This is supported by expectations for steady results from the existing portfolio and the deployment of between $200 to $300 million in investment capital this year toward development and redevelopment projects. This includes new concepts like Andretti Karting, of which EPR is the largest landlord and expects to do deals this year, as highlighted during last month’s NAREIT conference.

Risks to EPR include the fact that its properties aren’t exactly economically essential, which may result in pressures on tenants should there be a pullback in the economy. In addition, a higher-for-longer interest rate environment would raise EPR’s cost of debt.

However, EPR carries a strong balance sheet with a safe net debt to EBITDA ratio of 5.2x, and debt to total assets ratio of 49%, sitting below the 6.0x and 50% marks that are generally considered safe for REITs. It also has $1.1 million in total liquidity, more than covering the $137 million in debt maturities for this year.

Importantly for income investors, EPR currently yields an attractive 7.5%. The dividend was raised by 3.6% this year and is well-protected by a 75% AFFO payout ratio.

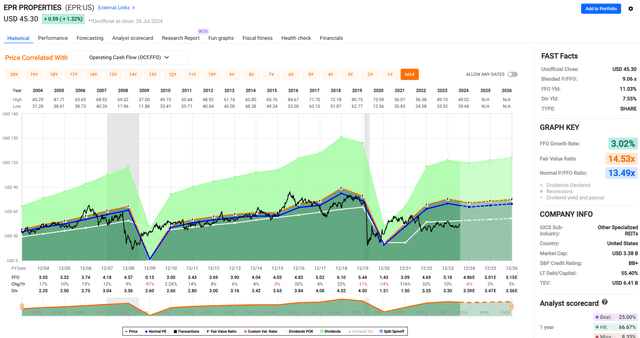

At the current price of $45.30 and forward P/FFO of 9.3x, EPR trades at a meaningful discount to its historical P/FFO of 13.5x, as shown below.

FAST Graphs

EPR also trades at a significant discount to the 13.8x P/FFO of Realty Income Corp. and 12.8x of W. P. Carey. While I wouldn’t expect EPR to trade at the same valuation as Realty Income, I believe the current valuation gap is too wide between EPR and its net lease peers.

With a 7.5% dividend yield and my estimate for 3-5% long-term FFO/share growth, to be driven by rent escalators and developments, EPR could deliver market-level performance, and any return to its mean valuation would be a total return kicker.

Investor Takeaway

Barings BDC and EPR Properties are currently appealing opportunities for income-focused investors, each providing high dividend yields well above market averages. BBDC, a middle-market lender with a diverse and conservatively structured portfolio, boasts respectable NAV growth and low non-accrual rate, supported by its floating rate debt investments.

EPR carries some of the most productive theater asset and a well-rounded and growing experiential portfolio beyond that, with strong rent coverage and healthy financials.

Both companies demonstrate solid fundamentals and are trading at discounts to their peers, presenting attractive value propositions for investors seeking steady income and potential capital appreciation.

Read the full article here