PureCycle (NASDAQ:PCT) continues making progress; it is inching towards commercial operations at its unique polypropylene recycling facility. Potential customers have released products made with PCT recycled pellets, which can now be used in food packaging. The product appears to be gaining traction.

The potential market is enormous, underserved and ripe for exploitation. If PCT can get its facility running reliably, and producing consistent, high-quality products then there is a significant demand already in evidence.

The question is, can PCT do it? And can they make a profit if they do?

In my first article on PCT, I looked at the market for recycled plastics and the potential competitors for PCT, concluding they had a unique valuation proposition with virtually no competition. Much of the article concentrated on the technical problems with PCT’s first commercial site IronTon. My research raised 5 issues that were reducing the quality of the end product and the uptime of the system. Without a high-quality, reliable product PCT can never succeed and that must be the first aim of the company.

The research pointed to a technical issue with the removal of polyethylene and ash. PCT calls this Co-Product 2. The removal of CP2 placed a bottleneck on production. Variable color reduced the quality of the final output below that expected of the market, a problem linked to absorption bed technology, and most worryingly, the overall system looked unreliable.

In this article, I look at the technical progress that has been made, suggesting that PCT has now resolved most operational and technical problems.

With commercial-scale operations on the horizon, I will examine the commercial side of the business model. PCT has not yet started to generate revenue, and its final cost structure is unknown. Still, it will be the next problem for PCT to solve. They have proven to be excellent problem solvers in science and engineering, but the next problems will be financial.

Q2 earnings are due soon (August 8th), PCT share price is rising in advance of the release as the market and I look forward to confirmation of the technical progress and the beginnings of commercial progress.

PCT a recap of the business

It has a simple business model: PCT will buy bales of waste polypropylene from recycling centers. Put the waste through their patent protected system which extracts additives and contaminants from the polypropylene using several processes. The output is pure polypropylene pellets that will be sold as raw material to manufacturing companies in place of virgin polypropylene.

The process is chemical and uses solvents and reactions, unlike the competing mechanical process, which uses shredding and heat. As a result, the output from PCT is a viable alternative to virgin stock, whereas the mechanically recycled product is not due to contaminants remaining in the pellets.

IronTon Progress is a big positive

PCT conducted a site tour, and the CEO shared a lot of information as he walked around. A recording of the tour is on the PCT website.

PCT has been working on the IronTon facility, the first commercial site, since 2020. The technology they are using is new and complex. It has proven more difficult than expected to achieve operational status and even longer to achieve reliable operations with the right quality output. Hundreds, perhaps even thousands of components and techniques have needed improvement, replacement, or re-design.

Many problems relate to feedstock; feedstock is delivered in graded bales and IronTon uses bail number 5, meant to have less than 5% polyethylene. The CEO explained that the bales actually contain between 2% and 20% polyethylene, beyond the original design parameters. The contaminants are hard to remove, it is not a matter of sorting, they were intentionally compounded with polypropylene at the manufacturing stage to improve the performance of the finished material or to reduce costs. PCT must undo that chemical compounding. (CEO walkthrough)

Technical Progress

In my first article on PCT, I identified five key areas I needed to see progress: operational reliability, CP2 removal, final product color issues, multiple feedstock use and surpassing the 5,000 pounds per hour run rate.

During the site tour, the CEO discussed all these issues. Progress ranges from fully resolved to significant improvement shown, and the IronTon facility is slowly coming online as a high-volume facility.

The PCT process involves the removal of two major chemical compounds PCT call them Co-Product 1 and Co-Product-2. In the site walk-around the CEO showed how, depending on the feedstock, these Co-Products can vary dramatically showing batches of CP1 varying from a black oily solid to a white crumbly one. He did say they were seeing interest in CP1 from various industries that can use it in their operations. Initially, CP1 was going to be dumped in a landfill at a cost of $0.04 per pound but now is seen as an additional revenue stream.

The removal of CP2 has been an ongoing problem, it had become a major bottleneck, and it is still being worked on. PCT now has a working (if manual) system in place and is in the process of building an automated system that will bolt onto the facility. I no longer consider CP2 a problem, PCT has developed a working solution, perhaps not as elegant as one would like, but it does work, and they could just add multiple manual stations to increase throughput (CEO walkthrough).

A new absorption stage was introduced to the system resolving the color issue and making the output as close to virgin material as possible.

In March, a shutdown (PCT call it an outage) was announced expected to last 2-4 weeks to improve CP1 and CP2 removal. The outage was extended for 1 week to complete additional work. Operations restarted on May 20th and were stopped by a storm 2 days later. During the 2 days of operations throughput reached 5,500 pounds per hour (an increase from 5,000 pounds in my first article)

The facility was restarted on May 30th and rates reached 6,500 pounds per hour producing 800,000 pounds by June 10th (in my first article they had only managed 183,000 pounds in a continuous run) the remainder of the month was spent commissioning the CP2 upgrades.

In the July update the CEO said they were still working on improving product quality and consistency and hoped the new CP2 system would enable higher rates of production. He also discussed the introduction of pre-process automatic sorting using infrared technology which will enable PCT to vary the contaminant profile of feedstock going through the system.

The facility is now running more regularly and for longer periods than it was, but it is not the finished article. The continuous output increased by 400% from my first article in February to this one, the CEO made it clear in the walkthrough that the IronTon facility is not yet fully operational, he itemized several improvements that still need to be made but it was clear from the way he discussed the progress that the end is in sight.

Next month, we will get further updates as they continue to push the envelope on what they can achieve. The problem-solving skills they have shown are excellent, every time a problem arises, they seem able to devise a solution and build the required technology. It does question exactly how good the initial design and testing were before they built the full-scale commercial unit. As the CEO said in the walkthrough, they have had to change or improve thousands of components.

The CEO Dustin Olson (in position for 3 years) spent 20 years with LyondellBasell, a global leader in plastic production before moving to PCT. That experience is invaluable and Mr Olson is driving all that is promising at PCT. Should he leave, I would immediately re-assess the situation.

The previous management was the subject of a short seller attack leading to legal action. In the 2023 10-K (pages 96-98), a list of lawsuits is itemized. I counted 7, all pre-dating Mr Olson. In the Q1 2025 10Q (page 32) PCT announced they have reached agreement on two cases requiring payment of $15 million in total. The settlements are still pending court approval.

PCT Finances

My concerns with PCT operations have been reduced. I now believe they will solve the technological problems, and they have proven that the IronTon site can operate at high volume and produce high-quality output. They still have issues to resolve but I am confident that can be done.

With the technical issues seemingly resolved, PCT faces a new one, the commercial business model.

Can they operate profitably and fund the business long enough for that profitability to arrive?

PCT Sales

PCT has not yet reported any commercial revenue however, their product has been tested and used in multiple products.

PCT resin was used to produce stadium cups that were collected and recycled through PCT, possibly the first fully circular recycling program. Beverly Knits began using PCT pellets to make fibers. Contaminants cause the threads in these fibers to break and mechanically recycled pellets cannot be used in this application. Fiber represents 15% of global demand for polypropylene and PCT is the first recycled product suitable. At the walkthrough, a rug made from 100% PCT recycled fiber was displayed.

PCT pellets were used to produce multiple compounds for industrial use, opening another enormous market.

The FDA has approved PCT pellets for use in all food packaging developing another sales channel.

In the Q2 earnings call the CEO discussed demand saying the supply is underserved and that demand for the product remains very, very high. He finished his prepared remarks with this line.

All of this indicates that the marketing timing for PureCycle is good. The demand for our product is strong and we are well positioned to take advantage of it.

The Balance sheet

There has been a lot of movement this year on the PCT balance sheet. In broad brush strokes the balance sheet is not in great shape. They have equity (assets-liabilities) of $340 million and debt of $290 million. With $25 million of cash and short-term assets on hand giving them less than a year’s cash runway.

PCT will need $12.5 million to pay a performance milestone after the IronTon site is complete and has committed to $47 million on long lead time equipment for Augusta facility number 2, $17 million for future feed sorting facilities and interest payments of $18 million, the final legal fees are unknown but much of it is covered by insurance. (10Q 2024 Q1).

PCT has a $200 million revolving credit line that is currently untouched.

In March, PCT purchased 99% of its outstanding bonds using $200 million of its cash on hand and $50 million of restricted cash (the 10q also quotes $185 million and $75 million for these figures). In total, $259 million was paid for the bonds.

The bonds had clauses that were not going to be met, PCT can re-market them with different clauses giving it the option to increase liquidity in the future. (10Q Q1 2024)

In the Q1 earnings call the CEO said

We are marketing these bonds as a cash instrument for our operations. We’ve reached an agreement on the sale of bonds that will bring forward $30 million of new cash to the operation as well as convert an outstanding loan.

PCT believes that having taken action on the bonds the doubt concerning its ability to continue as a going concern (mentioned in the 10-Q) has been alleviated.

After considering management’s plans to mitigate these conditions, including adjustment of expenditure timing and execution of the amendment to the Revolving Credit Facility, PCT believes this substantial doubt has been alleviated and it has sufficient liquidity to continue as a going concern for the next twelve months.

The Road to Profitability.

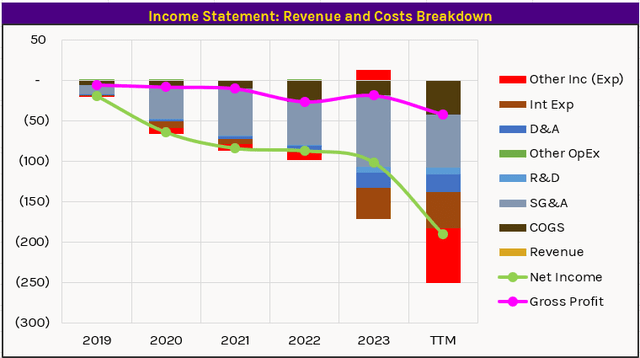

The income statement shows the scale of the commercial operational problem facing PCT, net income is heading lower and only revenue and positive gross profit can reverse this situation.

Income Statement over time (Author Database)

The plant is not operational, so we do not have any data for cost prices, sale prices or cost of goods sold. We are forced into back-of-the-envelope type calculations to estimate profitability using industry data.

In the Q1 earnings call the following figures were given by management.

Cost of a No 5 Bale of waste polypropylene $0.05 per pound

Price for mechanically recycled polypropylene $0.80 to $1.20 per pound

The Plastics Exchange shows prices of $0.60 to $0.80 per pound for virgin material, suggesting buyers pay a premium for recycled pellets.

The Q1 10-Q itemized operating costs of $39 million, suggesting costs of $13 million per month however in the earnings report the CFO said in the Q and A section.

We’ve been running probably around $8.5 million a month in terms of just cash expenses. And it seems to be a steady state. I’d like to think as we’re operating more efficiently, that those costs will come down somewhat. It’s hard to tell because we haven’t been running continuously. But just based on some of the things that we’re seeing, we think that costs will come down a bit.

I will use monthly costs of $8 million, they are still working on the site so some costs will come down but some variable costs will go up.

The current maximum capacity for the system is 250,000 pounds per day and I will assume a 30-day working month.

The 250,000-pound capacity is a function of CP2 removal, in the Q1 earnings call the CEO said he hoped that the new CP2 removal capacity, yet to be installed, would lift their capacity to remove CP2 from 5,000 pounds to between 10,000 and 20,000.

The process removes Co Product 1 and Co Product 2 as well as the initial sort so 1 pound of input will not lead to 1 pound of output. I assume a 75% conversion rate but ignore sales of CP1 and CP2 as I have no data to work with.

The new system, if it works as expected, should double or triple its capacity.

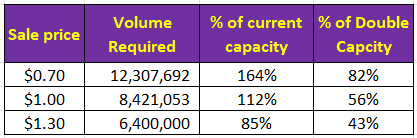

Using these figures, I produced the following table that shows the volume required, in pounds to break even.

Break even volumes (Author)

At lower volumes, the price could be over $1.20 as we know the PCT product is superior to the mechanically recycled product selling at that price, however as volumes go up it is inevitable that they will have to compete with virgin stock currently selling at a lower price.

The table is only indicative, it does not account for an increase in costs despite a doubling of capacity but it does indicate that if the new CP2 installation works as expected and PCT can run the system at full throttle for 80% of the time they will make a substantial profit at all price points.

Similarly, it shows that if they cannot increase maximum capacity, they will struggle to make a profit unless they can charge a substantial premium and have close to faultless operations.

This back of the envelope calculation is not a forecast, it highlights the business commercial model is not yet proven, but it would not take that many improvements to get to a situation where the site could be profitable at all price points.

Once IronTon is working and profitable, the other sites I discussed in my first article at Augusta, Antwerp, Korea and Japan should begin to make rapid progress toward operations. I hope we can look at these sites in more detail after the next earnings call. At which time I hope to begin developing a cash flow forecast and arrive at a fair value price for PCT, which will be the basis of my next PCT article

Conclusion

PCT is making excellent progress with its first site. IronTon is a testbed for their process, many things have gone wrong but the engineers at PCT have come up with solutions time after time, sometimes making more than a hundred improvements during a single outage.

The facility is now producing pellets in the millions of pounds when it is operational and is becoming operational more often. I think it is inevitable that they will become fully operational soon, probably in 2024.

Potential customers have produced products using PCT output and it appears to be as good as virgin polypropylene and far better than mechanically recycled products.

The potential market is vast, a worldwide operation is possible with enormous revenue and very little competition. I think that PCT will be able to sell whatever volume it can produce if it can compete effectively on price.

The profitability of the operation is not yet proven, we understand the cost of the feedstock and that it is readily available. We have some understanding of the sale price of the output, but it is in a broad range from $0.70 to $1.40. We do not understand the variable cost of production but a back of the envelope calculation suggests the operation could attain a measure of profitability if the new CP2 removal system can double throughput as predicted by management.

It is an exciting time for PCT, I will hold on to my position. With the business model still unproven I am not yet ready to increase my rating to a strong buy but hope to do so later this year when we get evidence of sales prices, confirmation of demand and see the maximum capacity of the site increase with the new CP2 removal process.

Read the full article here