Since I last wrote about the French fashion house Hermès (OTCPK:HESAY) (OTCPK:HESAF) over a year ago, its price is up by 7.6%. Underwhelming, right? Wrong. The luxury market slowdown has taken quite the toll on the sector’s stocks. The biggest luxury company, LVMH (OTCPK:LVMUY), for example, has seen a 23% price decline during this time, by comparison.

So, just the fact that Hermès continues to see an uptick is quite the achievement in itself. But the question is, can it continue to do so in an unsupportive market? I believe so. Here are five reasons why.

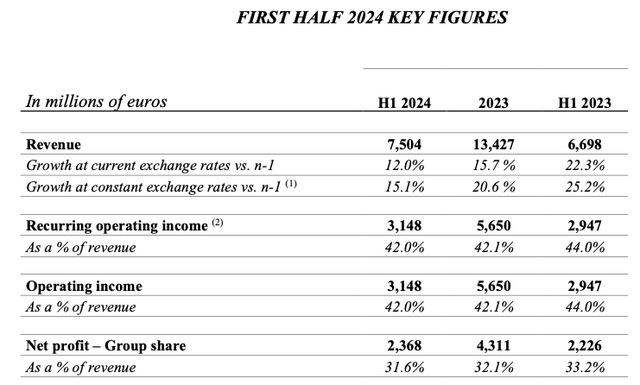

#1. Continued revenue growth

The company’s recently released results for the first half of 2024 (H1, 2024), showed continued double-digit revenue growth. At current exchange rates, the figure grew by 12% year-on-year (YoY) and by a bigger 15% YoY in constant currency. While there’s no doubt that this is a cooling off in growth from the 21% increase at constant rates seen in 2023 and an even higher 25% YoY in H1 2023, the fact that it has sustained at relatively elevated levels is still notable.

By comparison, LVMH saw just 2% YoY increase in its H1 2024 organic revenue growth. Even considering that it has a far bigger portfolio, which among other things includes the sagging Wine & Spirits segment, the drag is noticeable for it. LVMH’s big Fashion & Leather Goods segment, for instance, grew by just 1% YoY over this time.

Source: Hermès

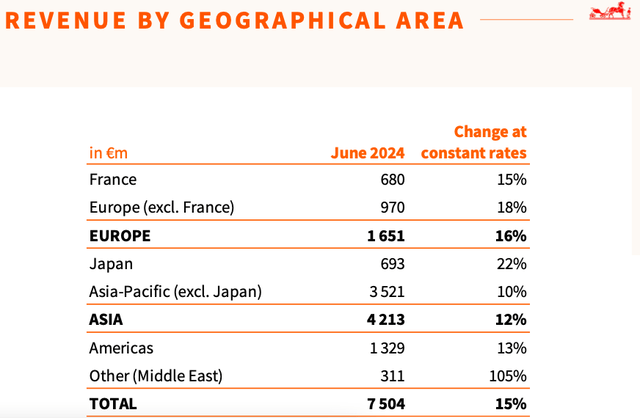

#2. Regional balance is largely sustained

Much like LVMH, Hermès too saw relatively softer demand trends from the Asia ex-Japan market, though, as China is currently losing its luxury appetite. There are two differences, however. One, even then, the Asia ex-Japan market showed a 10% YoY increase at constant rates, compared to a 10% YoY contraction for LVMH. And two, its European market is particularly strong, and the Americas aren’t doing too badly either (see table below), which is notable considering the softening in the US economy in Q1 2024.

Source: Hermès

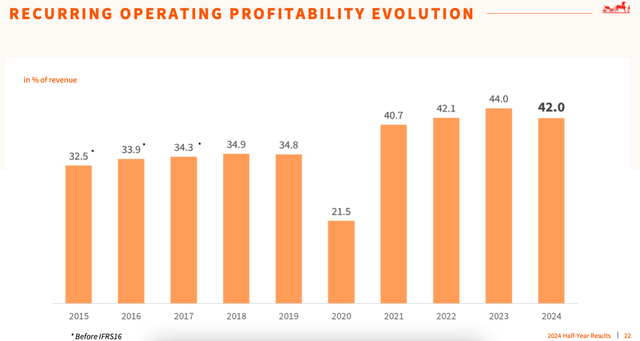

#3. Expanding profits

Hermès also continued expanding its profits. Its operating profit increased by 7% YoY. Even though the margin was down by 200 basis points to 42% (H1 2023: 44%), reflecting the negative impact of currency hedging, it remains rather strong (see chart below). Similarly, the net attributable profit margin came in at 31.6% (H1 2023: 33.2%), with net profits up by 6% YoY.

Source: Hermès

#4. Outlook and improved market multiples

If the company’s reported revenues continue to grow at 12% for the full year 2024 and the net margin stays constant at its H1 2024 levels as well, it would end the year with a net attributable profit of EUR 4.74 billion or USD 5.17 billion.

This results in a forward price-to-earnings (P/E) ratio of 45.7x. Now, this isn’t low by any standards. But then, when it comes to Hermès, low is a relative term. In last July, the forward ratio was at 52.2x and its price has only risen since. Admittedly, there are now bigger concerns about the health of the luxury market, but as noted earlier, the company’s isn’t terribly affected by it.

HESAY’s trailing twelve months [TTM] P/E at 49.6x is similarly lower than it was a year ago, at 63.2x. Also, it has stayed above these levels for much of the past five years (see chart below).

P/E, GAAP, TTM, 5y (Source: Seeking Alpha)

#5. High dividend yield on cost

There are also the dividends to consider. On the face of it, HESAY’s dividend yield isn’t anything noteworthy, with the TTM figure at 0.7% and the forward yield at 1.1%. But consider the yield on cost, which is a significant 7.4% over the past 10 years, which is obscured by its 577% price return over the period.

Source: Seeking Alpha

The risks

However, there are risks to Hermès too. In its outlook for 2024, the company refers to “a more complex economic and geopolitical context”, even as it “confirms an ambitious goal for revenue growth at constant exchange rates” for the medium term.

In other words, while the company has held up well in H1 2024, it can’t be taken for granted that H2 2024 will continue to be as positive. It has seen a deep come off in segments like Silks and Textiles as well as Watches, which have seen a 1.5% YoY and -0.2% change respectively at constant exchange rates, compared to 15.6% and 23.2% increases for the full year 2023.

It’s some solace that together these segments accounted for just 11.5% of the total revenue in 2023, though. As is the fact that the US economy grew at a faster than expected clip in Q2 2024 and growth is expected to pick up this year and the next in the euro area as well. This could continue to keep Hermès growing.

But there’s also HESAY’s price to think about. As the chart on the TTM P/E shows, it has the capacity to fall further, even if it doesn’t remain at much lower levels for too long. This in turn can mean at least short-term dips in the stock.

What next?

Still, there’s more going for Hermès than not. The company’s fundamentals are surprisingly strong, even considering that Chinese consumers have turned shy when it comes to luxury. Double-digit revenue growth, rising profits and robust margins all work in its favour. Additionally, HESAY’s reduced P/E from last year indicates that there can be further upside to it moving forward.

At the same time, the luxury market slowdown can’t be taken lightly, especially when it has shown up starkly in some of its segments. With some risk that the P/E can decline below the current levels, there can be downside to the stock.

However, any price dips would be a good time to accumulate the stock, which has given robust returns over the past decade and even its long-term dividend yield on cost is notable. It would make a good buy with at least the medium-term, if not the long term in mind now. I’m upgrading Hermès to Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here