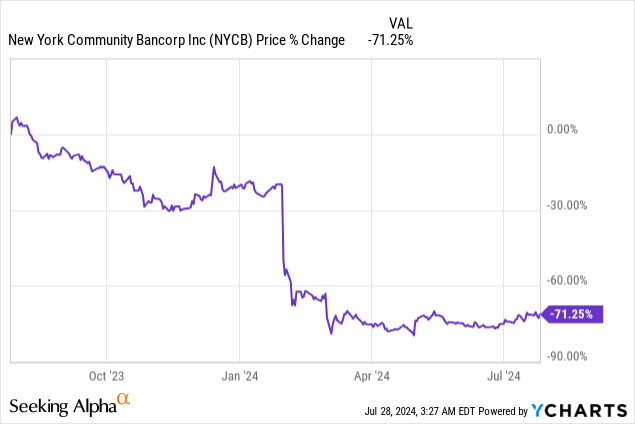

New York Community Bancorp (NYSE:NYCB) made news earlier this year when it was forced to raise equity and cut its dividend due to problems creeping up in its commercial loan book. The regional lender’s second-quarter results showed pressure on net income as well as continually unfavorable credit trends, including in the multi-family business. However, the bank is making progress in selling non-strategic assets in order to reorganize its business and improve its liquidity position. NYCB is also conducting an in-depth review of its loan exposure, and investors can expect New York Community Bank to sell more assets in the future. I believe the risk profile is still very much skewed to the upside, given that New York Community Bank is trading at a steep discount to its tangible book value.

Previous rating

I recommended shares as a buy of New York Community Bank in February — Why I Am Buying The 70% Dividend Cut — and confirmed my rating after the regional lender secured a $1.0B strategic equity investment in March. Although the bank reported a drastic increase in credit provisions again in the second-quarter, the deterioration in credit quality was widely expected, which explains why shares hardly moved after earnings. I believe strategic measures, such as the sale of non-core assets, help reduce balance sheet risks and improve liquidity, and the regional lender could return to growth in FY 2025.

NYCB’s second-quarter results, non-core asset sales, unfavorable credit trends

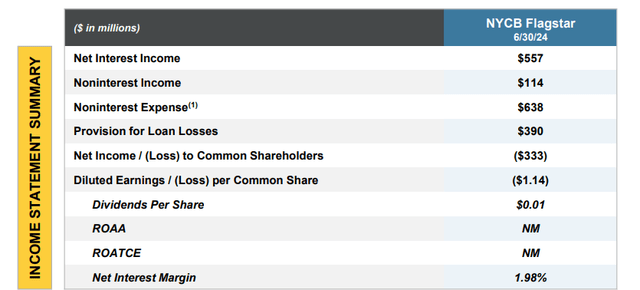

New York Community Bank reported overall weak results for the second quarter due to continual loan problems in the bank’s CRE portfolio. The regional lender reported a net loss of $333M or $1.14 per share, compared to a profit of $405M or $1.66 per share in the year-earlier period. The decline in earnings was driven chiefly by declining credit quality in New York Community Bank’s loan commercial real estate loan portfolio.

NYCB

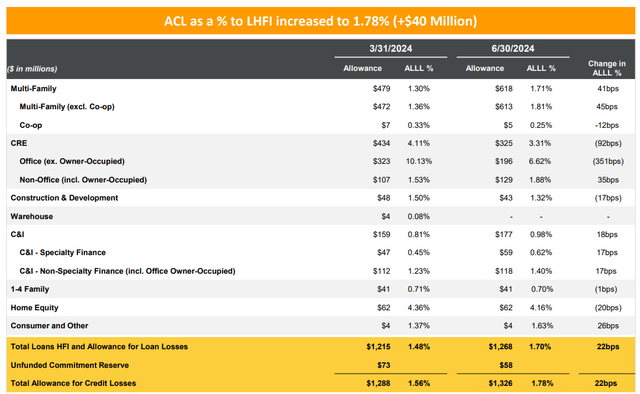

New York Community Bank’s results were mainly impacted by an almost 700% year-over-year increase in credit provisions: in the second quarter, the lender’s credit loss provisions amounted to $390M, compared to just $49M last year. As a result, the bank’s total allowance for credit losses also increased, from 1.56% in Q1’24 to 1.70% in Q2’24, mainly due to weakness in multi-family loans. In this segment, the allowance for loan losses increased by 0.41 PP quarter over quarter to 1.71%.

New York Community Corp

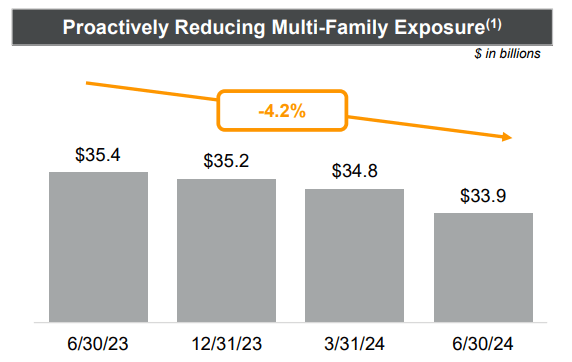

New York Community Bank has initiated a comprehensive review of its multi-family loans and stated that it wants to shrink its portfolio. As of the end of the June quarter, NYCB had $33.9B in multi-family exposure, showing a decline of 4.2% year over year. The sale of multi-family loan assets is set to reduce the bank’s balance sheet risks as well as improve NYCB’s liquidity profile.

New York Community Corp

New York Community Bank has already made some progress in improving its liquidity profile and announced last week that it divested more non-strategic assets lately: it sold its residential mortgage servicing business for $1.4B to Mr. Cooper, a mortgage originator and servicer. The lender also closed the sale of its $6.1B mortgage warehouse portfolio to JPMorgan & Chase this month, and both sales are positive developments for the bank. NYCB had total liquidity of $33B in Q2’24 (not including the sale of the mortgage warehouse portfolio), showing an increase of $5B quarter over quarter.

I expect more non-strategic asset sales for New York Community Bank in the remainder of the year, chiefly to offload loan risks and shore up the lender’s balance sheet. Multi-family loans are one area where I can see increased sale activity. New York Community Bank is also applying a strict cost reduction focus to its banking operations, which could help lower operating expenses going forward.

NYCB’s valuation

New York Community Bank still very much has a distressed valuation. However, I believe the increase in credit loss provisions was not that much of a surprise given the surge in credit provisions in Q1’24, which also explains why investors barely reacted to the lender’s second-quarter earnings report.

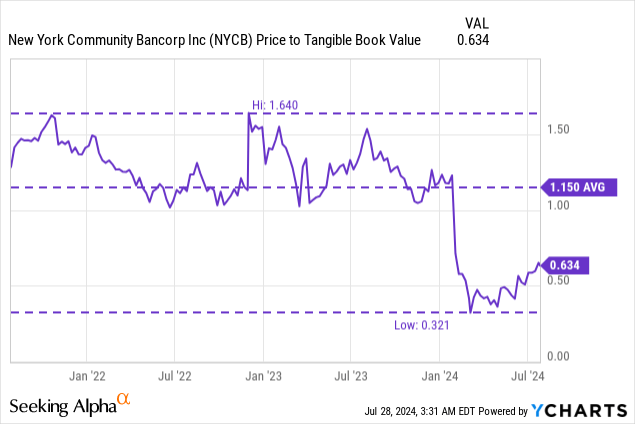

Shares of New York Community Bank Currently are priced at a 37% discount to the lender’s tangible book value which reflects deep concerns about the bank’s portfolio quality, but also, in my opinion, signals a high margin of safety given that NYCB is shoring up its balance sheet and making progress in boosting its liquidity profile. The 3-year average P/TBV ratio was 1.15X, significantly higher compared to where the valuation of NYCB stands today.

In the longer term, I believe it is not unreasonable to expect New York Community Bank’s shares to return to at least a 1.0X price-to-TBV ratio, although this is likely only going to happen if the bank gets a grip on its credit issues, especially in the multi-family segment, and avoids a deterioration in the bank’s overall credit trend. The bank’s tangible book as of June 30, 2024 was $20.89 which I see as my long-term revaluation target for NYCB. If New York Community Bank continues to restructure its operations, down-sizes its (multi-family) loan book, and returns to growth in its core banking business in FY 2025, I definitely can see shares of NYCB trade at 1.0X tangible book value.

Risks with valuation

The most important trend that investors have to watch here is the trend in portfolio quality, especially in multi-family. The Q2’24 increase in credit provisions was kind of expected, and it is widely accepted that the bank’s full-year 2024 results are not going to be great. However, as the bank restructures and focuses on selling more non-strategic assets and raising capital, I believe NYCB could have a much-improved risk profile in FY 2025. What would change my mind about NYCB is if the bank’s credit loss provisions kept surging throughout the second half of the year or if the bank failed to shrink its multi-family portfolio.

Final thoughts

All things considered, Q2’24 was not a totally bad quarter for New York Community Bank. The credit trend remained weak, due to issues in the multi-family loan portfolio, but the bank has been successful in selling non-core assets and raising cash, which goes a long way in reducing balance sheet risks. The regional lender just before earnings announced that it also sold its residential mortgage servicing business for $1.4B. What keeps my buy rating in place is that the bank’s shares continue to sell at a very large discount to tangible book value. If New York Community Bank can avoid an escalation of credit problems in the second half of the year and return to earnings growth in FY 2025, I believe investors could see a serious attempt at a share price revaluation!

Read the full article here