Topics Covered

Vertical Market Software, Serial Acquirers, & Software as a Service

Relevant Companies

Serial Acquires: Constellation Software (OTCPK:CNSWF), Topicus (OTCPK:TOITF), Vitec Software (VIT-B), Roper Technologies (ROP), Sygniety (SGN.PL), Addnode Group (ADDNF), Lumine Group (OTCPK:LMGIF), Arcadea Group (Private).

Larger Single Vertical Markets: AppFolio (APPF), Veeva Systems (VEEV), Toast (TOST), nCino (NCNO), Shopify (SHOP), Procore (PCOR), Cellebrite (CLBT).

Nuggets

- The very best vertical software companies build a layer cake of new products that consistently drive growth.

- I am a big fan of going to potential clients and pitching your vertical software product before you build it. Then building the product based on what the early client evangelist want.

- While customers in horizontal markets often try different software vendors, resulting in multiple winners in a market segment, customers in vertical markets prefer purpose-built software for their specific industry and use cases

Levelsetting

Vertical Market: A vertical market is a market encompassing a group of companies and customers that are all interconnected around a specific niche. An example of a vertical market is US-based ambulance companies.

Vertical Market Software (VMS): Vertical market software is software specifically designed to address the needs of a given vertical market segment. Vertical market software has a high level of customization to service their specific market, making the software very niche. An example of vertical market software is AppFolio, which is specifically focused on software for real estate management and development companies. Alternatively, you can think of VMS as “Industry-Specific Software”.

Horizontal Market Software: Horizontal market software is the opposite of vertical market software in that it is industry-agnostic, but rather focuses on a single function within multiple industries. An example is Salesforce, which focuses on the sales function across many industries.

VMS Serial Acquirer: A company that uses an acquisition strategy to grow their business by buying smaller vertical market software businesses. An example of a VMS serial acquirer is Constellation Software.

VMS Single Vertical Market: A company that focuses on a single end market uses capital to reinvest in building new niche software products for that single market. An example of a VMS single vertical market operator is AppFolio.

ARR: Annual recurring revenue. ARR is a metric of predictable and recurring revenue generated by customers within a year for a subscription software model.

Churn is a metric that measures the number of customers that cancel their software subscription within a given period. Churn is usually calculated on an annualized basis as a ratio of total customers.

LTV: Lifetime value is the cumulative total of all revenue a customer contributes to your business over their entire lifetime of using your SaaS product or service. The higher the LTV, the higher the value of that customer to your business. Calculator LTV is more of an art form than a science, as it requires many assumptions.

CAC: Customer acquisition costs are the cost to acquire a new customer, usually calculated as the total costs of sales and marketing divided by the number of the number of new customers in a given period.

LTV/CCAC Ratio: The LTV/CAC ratio measures the relationship between the lifetime value of a customer and the cost of acquiring that customer. The higher the LTV/CAC, the better; it means the value of each customer is much higher than the cost to acquire that customer.

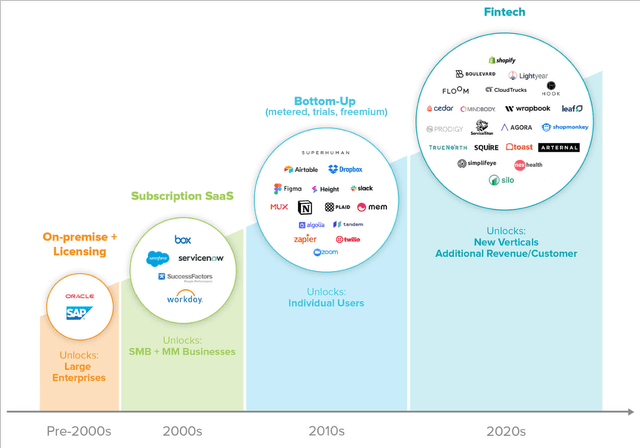

The Evolution of Software Business Models

Software models have evolved over the last 40 years from a licensing model to a subscription model to a usage-based system.

Source: Fintech Scales Vertical SaaS

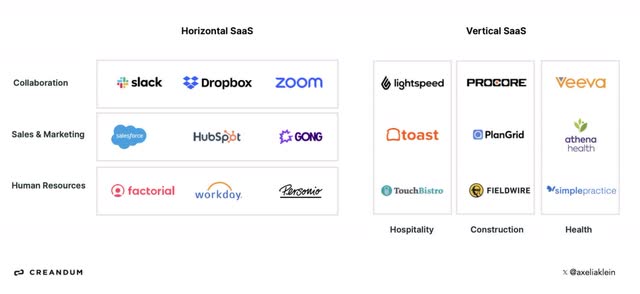

Vertical Software vs Horizontal Software

Vertical software has a much smaller TAM and fewer opportunities to grow through bringing on new clients than Horizontal software due to the niche focus of their software.

Source: A Guide to Industry- Specific Software and SaaS Verticals

Examples of Horizontal vs Vertical Software

Large Vertical software companies excel in complicated or highly regulated industries like healthcare.

Source: AI in B2B SaaS: Beyond Vertical and into the Horizon(tal)

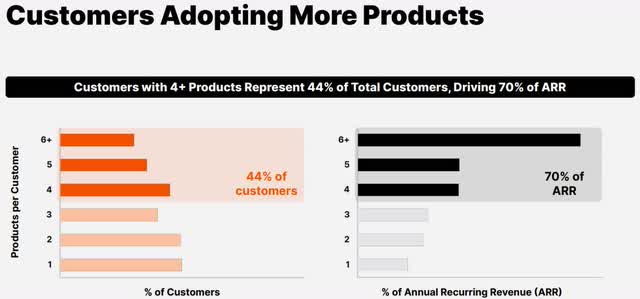

VMS is all about cross-selling and upselling existing customers. Due to the low churn and niche product offering VMS companies have a major opportunity to cross sell new products like AI or Cloud.

Source: Procure Investor Day

Questions & Answers

Q: What makes a VMS business attractive to investors?

Vertical market software is developed for and customized to industry-specific needs. These are businesses focused on niche markets, which have characteristics that make investing in them very attractive. These software markets are very “sticky” meaning they have low churn rates, which means the LTV of an individual customer can be extremely long. Due to the niche nature of these software, they have very few competitors. Because of the niche focus, software companies can build exactly what their clients request, making them tied very close to the customers and very “customer-centric”. These businesses have high pricing power as customers view their software as mission-critical and there are very few viable alternatives. Due to this close relationship with their customers, who they keep for longer periods than in horizontal software, vertical software companies are able to cross-sell existing customers more products.

Q: Why does the VMS segment make it attractive for a serial acquire strategy?

On top of what I just described as what makes specific VMS businesses attractive, there are several characteristics that make running a serial acquirer business in the VMS attractive. Firstly, VMS businesses don’t require much capital reinvestment to grow due to their software nature, low churn, and high pricing power. Thus, VMS businesses are very stable sources of cash flow over long periods of time that can be reinvested into acquisitions for other VMS businesses. Secondly, VMS businesses are often not very exposed to competitive pressures, making them less likely to have material declines due to new or better competitors.

Q: How will AI affect the VMS segment? Will AI disrupt the VMS segment?

While AI will impact the speed and cost of developing software, the creation of code itself is not the defining activity of VMS companies. The defining activity of VMS is the sales and customer relationship that they have with the specific end market. AI might help speed up the coding process, but it won’t take customer needs and turn them into applicable software. AI will likely help VMS companies by reducing their COGs through cheaper compute and software development. This cost decline will no doubt fade over time, so I don’t view it as a long-term change in the underlying business model but as a short-term boost to margins for those companies that can quickly adopt AI to support their software development processes.

AI and LLMs will simply be another tool for developers, like low code or no code in the past, but if used correctly will yield faster product cycles for VMS.

Q: Is the VMS Serial Acquirer space too mature with too many acquirers that drive down returns? If & when will it become too mature?

It is the main question that investors are asking of the original and largest VMW serial acquirer, Constellation Software. Can the VMS serial acquisition model continue to scale at the current pace? Constellation Software, for those that don’t know, was founded by Mark Leonard in 1995 and was the original VMS serial acquirer. They have now grown over that period from nothing to a massive $60b market cap exclusively through acquiring VMS companies. But how big is too big?

Constellation completed 134 deals in 2022 and over 100 deals in 2023. But the big difference in 2023 was that Constellation completed some “mega” deals in comparison to their normal deals.

Constellation completed multiple mega deals in 2023, including Topicus, Empower, Optimal Blue, and Lumine Group, all of which were over $100 million each and totaled over $1 billion of the $2.6 billion they deployed in 2023. 42% of the total capital deployed by Constellation was done in Mega Deals in 2023.

Clearly, Constellation can continue to scale, but in order to put $2-3 billion to work each year, I expect they will need a few “mega” deals of $100-$500 million. So are there enough VMS companies of that size that fit in with their specific operation requirements?

The answer is yes. There are likely ~25,000 vertical market software companies in existence worldwide (~ 5% of global software companies). There are around 15,000 new software companies created each year, and if you assume VMS companies are around 5% of that group, then there are 750 new VMS companies created each year. Last year, the public VMS serial acquirers acquired just 125 companies (see table below). Based on some rough back-of-the envelope math based on revenues, I think the total number of VMS serial acquirers is just 6% of the current market for VMS companies. There is plenty of room for growth.

Q: What are the major trends in VMS single vertical software?

Vertical market software: single vertical companies like Procore, Veeva, AppFolio, and Toast have been able to grow to huge sizes in recent years. This is in part because they each service very large end-market verticals. There are surprisingly few public single-vertical software companies, suggesting most industry niches do not have a large enough TAM to support such a large size. Within these VMS single-vertical software companies, a few trends have arisen recently that should propel them into growing their businesses by offering more products and services to their individual niches. Three growth trends I see are leveraging artificial intelligence, integration with other systems, and cross-selling cloud services.

AI and machine learning are being used to automate routine tasks, speed up coding, and enhance overall efficiency. Machine learning algorithms analyze vast amounts of data to provide actionable insights, helping businesses anticipate trends, optimize operations, and improve customer experiences. VMS single-vertical companies will all be adding AI functionality to their offerings in the next few years.

Seamless integration with existing systems and technologies is crucial. This trend emphasizes the importance of interoperability between vertical software and other enterprise applications, including ERP (Enterprise Resource Planning), CRM (Customer Relationship Management), and BI (Business Intelligence) tools. By integrating with other tools, VMS single-vertical companies can embed their products into the processes of their clients even further, making it more difficult to swap out their software for a competitor.

Cross-selling cloud offerings have become one of the major drivers of revenue growth in all of the software, not just VMS single-vertical software. The shift towards cloud-based solutions continues to grow. Cloud computing offers scalability, flexibility, and cost savings, allowing businesses to access their software from anywhere and easily scale up or down based on demand. Cloud offerings are all inherently done via a SaaS model, which eliminates the need for large upfront investments and allows for continuous updates and improvements.

Q: What makes more sense in terms of sources of acquisition funds, equity cash or debt?

Most VMS serial acquirers utilize a cash-first M&A strategy, including all of the Constellation Group companies. That is not to say they won’t utilize debt or equity in order to get larger deals done. Most notably, since 2020, Constellation has made several transformative acquisitions that resulted in spinoffs, equity issuance, and the use of debt in order to facilitate the deals. These deals were not the normal acquisitions of VMS businesses, but rather acquisitions of other VMS serial acquirer businesses. I consider these acquisitions different from the bread and butter of the normal VMS serial acquisition strategy, which utilizes the majority of cash for acquisitions. There is one exception: Vitec Software utilizes both cash and equity in a high proportion of their deals. This is done in order to increase the amount of capital that Vitec is able to deploy each year and allow them to scale quicker. If you are inclined to understand if this cash/equity model is sustainable, I would suggest trying to build your own model to assess its viability. I have done so, and I am convinced that as long as acquisitions are done at prudent multiples, Vitec Software’s model is incredibly attractive.

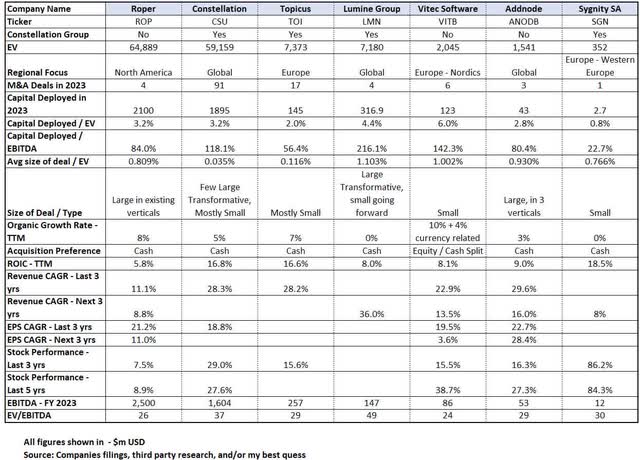

Q: How do the different VMS serial acquirers stake up against each other?

There are basically three types of serial acquirers: Constellation and its affiliates, Nordic’s, and Roper Technology. Each company has its own preferences and distinctions in terms of deal sizes, capital deployment strategy, whether they reinvest in organic growth, regional focus, and industry focus. Below is a summary of the public VMS serial acquirers:

In my opinion, there are several important operating guidelines that make a good VMS serial acquirer. The most important operating guideline for VMS serial acquirers is acquisition discipline, which ironically is very hard to assess at many of these companies due to lack of disclosure. Acquisitions need to have operational and management fit, as well as the acquirer needs to maintain valuation discipline.

Conclusions

- VMS will not be materially impacted by AI. AI is unlikely to significantly impact the vertical market software business because the sales process and understanding customer needs are deeply rooted in human relationships and industry-specific expertise. Vertical market software caters to niche industries with unique requirements, necessitating a tailored approach that only seasoned professionals with deep industry knowledge can provide. Sales in these markets are not just about offering a product; they involve building trust, understanding the specific challenges of each client, and providing customized solutions that align with their unique operational contexts. While AI can assist with data analysis and streamline some processes and writing code, it cannot replace the nuanced human interactions and the in-depth understanding of industry intricacies that are crucial in the vertical market software business.

- VMS serial acquirers still have a lot of runway, but they need to stay disciplined on the acquisition valuations. Vertical market software acquisition businesses like Constellation Software still have substantial growth potential due to the sheer number of existing vertical market software companies (estimated at ~15,000 in the US and ~25,000 globally based on various industry estimates) and the continuous emergence of new ones. Thousands of these niche software businesses cater to specific industries, offering tailored solutions that address unique operational needs. This vast landscape provides fertile ground for acquisitions, allowing firms like Constellation Software to continue to make acquisitions for many years without overtaking the entire market. Additionally, the constant creation of new vertical market software businesses each year introduces fresh opportunities for acquisitions, ensuring a steady pipeline of targets. The key question is how many others will follow Constellations footsteps and enter into the VMS acquisition market, and what does that do to the acquisition prices. Many private equity companies have ventured into the space in recent years, including large PE companies like Thoma Bravo, TPG, and Main Capital Partners. Most recently, the launch of Arcadea Group (Private) as a more long-term founder led version of Constellation has launched. Arcadea Group was founded by two ex-Constellation Software executives, Daniel Eisen and Paul Yancich. The company is backed by legendary investor Mitch Rales of Danaher (DHR). There is a good podcast in which Mitch talks about the venture. The company is a slight evolution of the Constellation model, in which they acquire VMS software companies, but they intend to help them organically grow at very high rates going forward. They are trying to replicate what Mitch Rales and his brother Steve have accomplished at Danaher with long-term compounding, but within a VMS acquisition model.

- Constellation Group (and its affiliates Topicus, Lumine, and Sygnity) have a sizable advantage in the VMS serial acquisition space, because of data, history, and talent. Constellation Group and its affiliates possess a significant advantage in the vertical market software (VMS) serial acquisition space due to their unparalleled depth and breadth of data, historical experience, and key talent (namely Mark Leonard, but the depth of their talent pool is pretty amazing, just listen to their AGM meeting to get a full understanding). With years of data from a multitude of acquisitions, Constellation can identify and evaluate potential targets unlike many of its competitors. Their extensive acquisition history provides a wealth of insights and best practices, enabling them to streamline integration processes and maximize value creation. Moreover, the group has cultivated a team of highly skilled professionals with deep expertise in various niche markets, fostering a culture of excellence and innovation. This combination of comprehensive data, rich historical experience, and exceptional talent positions Constellation Group uniquely to execute successful acquisitions and drive sustained growth, setting them apart from competitors in the VMS acquisition landscape.

- VMS single market vertical companies still have more room to grow through cross-selling cloud and AI products. AI and Cloud are an easy cross-sell for VMS companies. Both products fit naturally within their offering. Cloud offerings is a win-win for VMS and its customers as it reduces hosting costs and improves scalability.

Investment Takeaways

- Long Ideas – Vitec Software: Vitec’s business model, end market, and management create an extremely attractive business. Vitec has all the characteristics that we look for in an investment, including substantial reinvestment options, a strong capital allocation strategy, and a founder’s mindset. We currently believe Vitec will consistently grow at a high rate while maintaining strong, stable margins for many years to come. At the current price, we view the shares as reasonably valued to slightly overvalued, but we think over time the value of the shares will compound at a high rate. We plan to own Vitec for many years to allow our capital to compound with its high growth.

- There is no bad VMS Software serial acquirer public company, but valuations do matter. Based on the current valuations, we view Topicus as the cheapest VMS Serial Acquirer based on the forward growth and potential upside from its 72% ownership stake in Sygnity.

- Long Ideas: Topicus

Final Thought

Vertical market software is an attractive market due to its inherently low churn rates, customer-centric development approach, and the significant opportunities for cross-selling AI and cloud services. Low churn rates in VMS are driven by the specialized nature of the software, which is deeply integrated into the industry’s specific workflows and processes, making it indispensable for customers. The customer-centric development process further enhances the loyalty of their customers, as software solutions are continually refined and tailored to meet the evolving demands of the industry, thereby fostering long-term relationships (i.e. low churn). Moreover, the integration of AI and cloud services presents a lucrative cross-selling opportunity. By offering advanced analytics, automation, and scalable solutions through AI and cloud technologies, companies can provide additional value added services, opening up new revenue avenues. This combination of stable customer bases, tailored development, and expansive service offerings makes vertical market software a highly attractive and profitable market for many, many years to come.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here