Company Background

Veeva Systems (NYSE:VEEV) is a cloud-based software solution company providing essential services for medical companies practically on every step of their research and development helping with: clinical tests, streamlining regulatory processes, managing quality processes, improving safety, engaging scientific approach, and improving commercial results.

Today, healthcare is a highly technological and scientific field and if you are about to create a new drug, most likely at some stage you might need the product of Veeva Systems. According to the Q1 Veeva financial report, 3 out of 20 top biopharmas choose Veeva as a software provider.

In order to understand the new company better, I found it very useful to use Porter’s Five Forces Analysis. It provides a good framework.

Porter’s Five Forces Analysis for Veeva

Threat of New Entrants: Low. Specialization in software for life sciences Veeva makes it quite hard to enter this particular market because the process of regulatory compliance, industry-specific needs and expertise is impossible to acquire or build instantly. Moreover, major pharmaceutical brands once tried the products of Veeva and successfully reached their business goals will be brand-loyal. Once again building up this type of loyalty in the pharmaceutical field would take years for a newcomer, due to long product life cycles. The gross margin is 72%, meaning that Veeva has already reached economies of scale, making it even harder for new players to enter the market.

Bargaining Power of Suppliers: Medium. The clouding infrastructure is provided by Amazon Web Services and could be switched to another provider. Veeva is competing for qualified employees with other tech giants, and the bargaining power of specialized experts could be substantial. Veeva itself recognizes this fact as a risk factor in the 10-Q report.

Bargaining Power of Buyers: Medium. The buyers are concentrated mainly in the North America region (41% of revenue) and one industry these factors lead to a significant bargaining power of buyers, However, once they are familiar and comfortable with Veeva’s service, the switching cost for the buyers would be quite high. Veeva intentionally provides a combo of Cloud service plus subscription revenue model, calling competitive server-based services from Oracle (ORCL) and Microsoft (MSFT) as “legacy” solutions.

Threats of substitutes: Low. Products from Salesforce (CRM), Microsoft, and Oracle are not that specialized in life sciences. The principal competitor named by Veeva is IQVIA (IQV) with the license of their CRM to Salesforce is aimed at life sciences and is also industry-specific.

Industry Rivalry: High. There are industry-tailored software providers. Veeva has to keep a strong market position with continuous R&D and with a brand-loyal customer base.

Recent Q1 2024 Performance

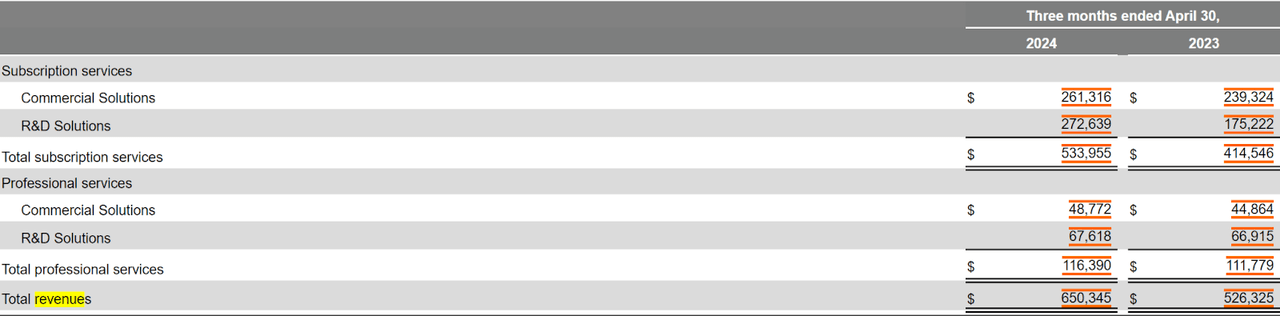

Veeva’s recent Q1 results show great performance. The reported revenue was $0.65B. This is a +3% growth QoQ and +24% YoY. Let’s have a look at the revenue breakdown in order to better understand the company’s business. Subscription services 82% of total revenues, including Commercial Solutions (40% of total revenue comes from 3 products; Veeva Commercial Cloud, Veeva Data Cloud, and Veeva Claims solutions); R&D Solutions (42% of total revenue comes from another 3 products Veeva Development Cloud, Veeva RegulatoryOne, and Veeva QualityOne solutions) and Professional Services 18% of total revenues.

VEEV’s Revenue Breakdown (EDGAR)

In 2024, the core revenue segment grew +28% in comparison with 2023.

The $0.65B of revenue generated $0.48B of gross profit and $0.16B of operating income, with a net income of $0.16B. One can observe that during the last five years, gross profit, operating profit, and, most importantly, net income have been growing in line with revenue. Here are the main financial metrics of profitability in the Q1 report:

Gross margin 72% – such high numbers are signaling that Veeva enjoys economies of scale because since 2014, the gross margin has increased from 61% up to 72-73%.

Operating margin 21%.

Net profit margin 22% – Although the NPM has been decreasing over the last five years, it is still a very solid and high number, reflecting that Veeva possesses a competitive advantage in the market of medical software.

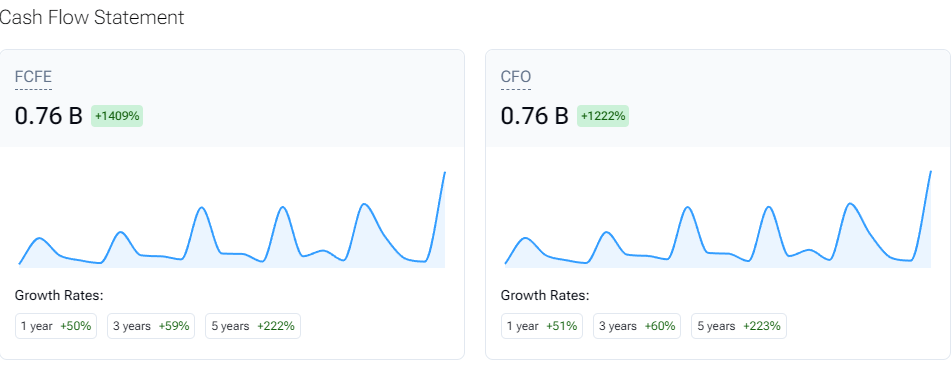

Earnings quality CFO/NI 210% – the business of Veeva is sustainable and cash-flow rich, enabling the company to look for favorable investment opportunities either within or outside the company. Both metrics FCFE and CFO show all-time highs, 0.76B and 0.76B, respectively. FCFE being the main component for the calculation of intrinsic value as a numerator could be a driver for upward revaluation for fundamental analytics. However, in this article, I will focus on a quantitative bottom-up approach because I believe it adds the most marginal value for the reader.

VEEV’s FCFE and CFO (Eyestock.io)

Financial Position and Efficiency

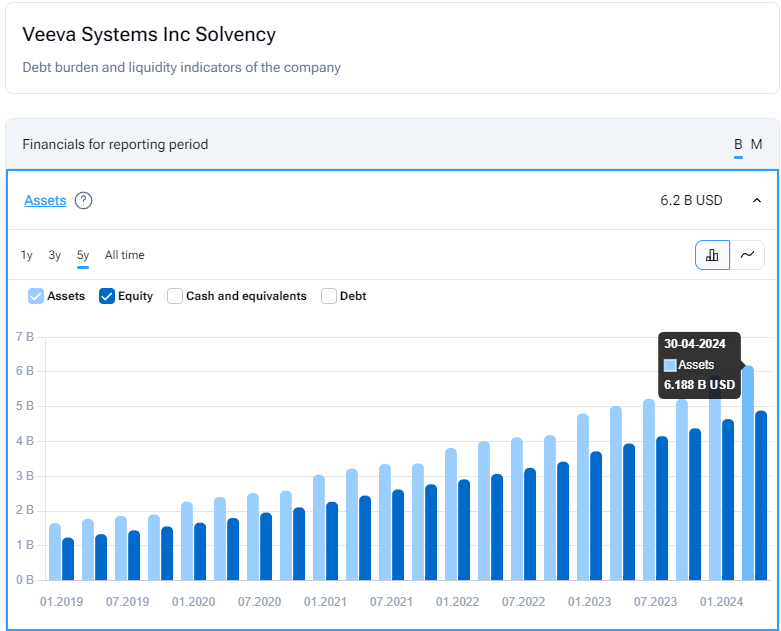

Veeva by the end of Q1 2024 has shown $6.19B in Assets (with nearly $4.77B in cash and cash equivalents) and $4.89B in Equity.

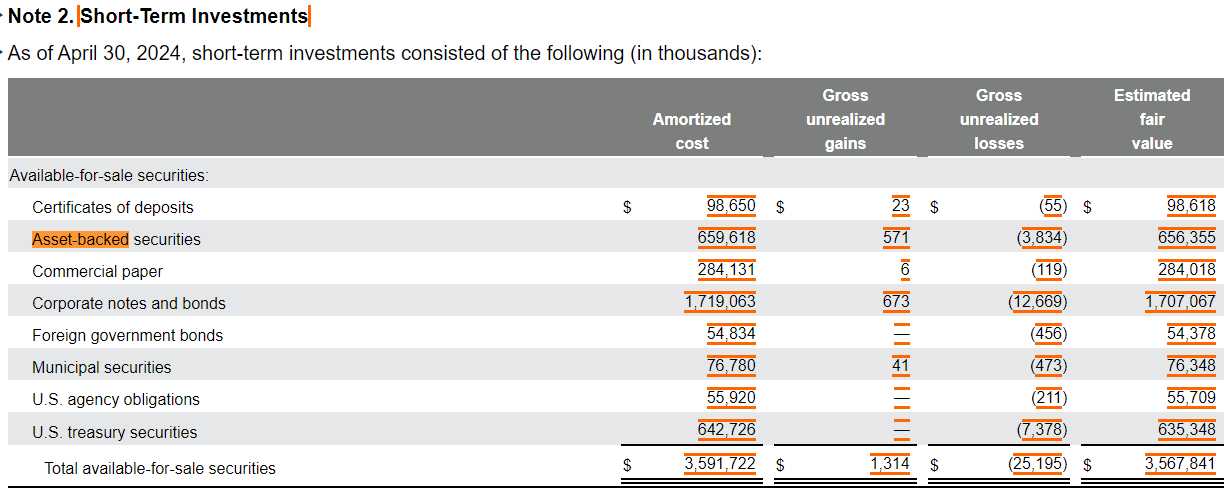

Veeva has a $3.6B short-term investment portfolio that is classified as available-for-sale with a maturity of 1.2B less than a year, and 2.4B greater than one year. Nearly 18% of the portfolio is in asset-backed securities and 48% in corporate notes. However, the management outlines that the intent is to hold it until maturity. That eliminates interest rate risk and investments of high quality. This statement demands further investigation because corporate notes and asset-backed securities could have a substantial credit risk, including downgrade risk and spread risk.

VEEV’s Short-term investment (EDGAR)

There is almost a perfect picture in Veeva’s balance sheet because of rising assets and rising equity for the last five years with zero long-term debt.

VEEV’s Assets and Equity (Eyestock.io)

That makes such financial ratios meaningless in the best sense of the word: debt/equity 0, current ratio 4.5, CFO/Debt N/A.

The company is liquid and solvent, both in the short and long term.

Let’s have a look at return on equity and return on assets to evaluate how effectively Veeva’s management uses its resources: ROE of 12%, significant, but not good enough. According to my investment philosophy, an ROE benchmark is 20%. Let’s decompose ROE via DuPont Analysis: NPM 22%, asset turnover 0.437, financial leverage 1.248 (potential use of debt could be favorable in order to improve ROE via an increase in financial leverage), ROA 10%, and ROIC 78%.

Future Prospects and Valuation

Veeva has provided guidance for Q2 total revenue between $666M and $669M, and total revenue for the fiscal year $2,700M and $2,710M. A very modest cut of total revenue by $30M (-1%) was met by the market very negatively. Even with a decreased guidance, the rest three quarters can provide revenue of $680M each.

The company can see further adoption of its products, especially highlighting Vault CRM and Commercial Data for the industry with Data Cloud, allowing to track crucial data about patients and prescribes.

The DCF models presume not that optimistic intrinsic value in the base case of $110 per share with a revenue growth of around 10%. However, the P/E ratio of Veeva has been historically very high, ranging from 59-140, reflecting expectations of higher growth rates and lower WACC.

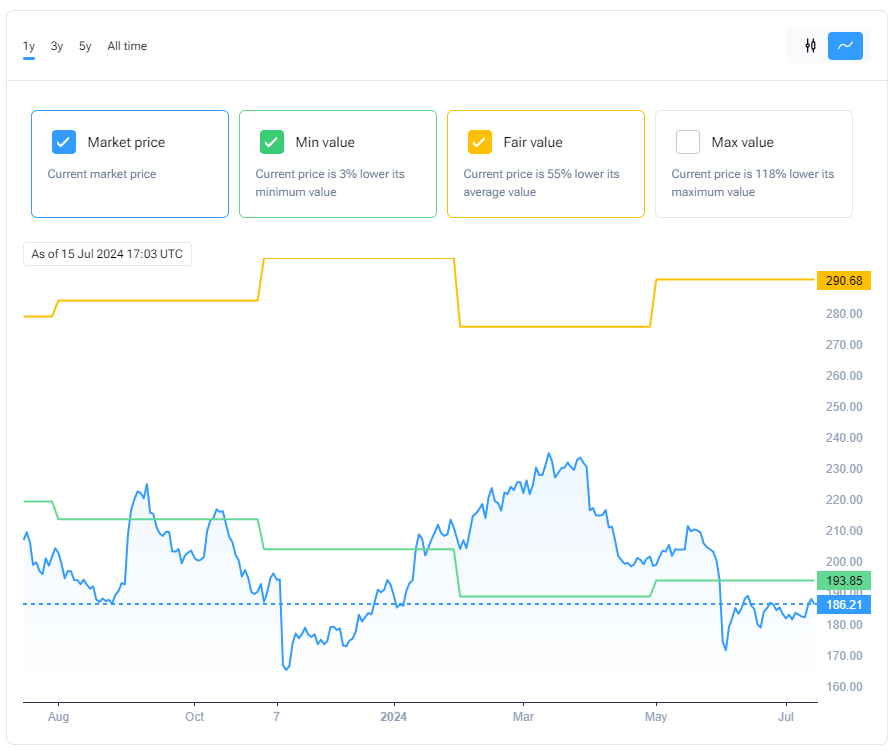

I believe in a relative historical valuation approach that presumes a VEEV fair value of around $290 per share, an undervaluation of 54.7%.

VEEV’s Relative Valuation (Eyestock.io)

Taking into consideration the high quality of a stock, growth potential, consistency of revenue, and solid financial position, VEEV is a value investment opportunity with a low-risk entry point below $193.85 per share.

Risks

The risks related to the business of Veeva Systems, in my opinion, are mostly concentrated in the market competition. It is a highly competitive market where Veeva needs to compete effectively to maintain high growth rates. The challenge is to be cost-effective and attract highly skilled employees, maintaining high margins.

The revenue is highly concentrated in one region and life science sphere, limited to a small number of key customers. The possible loss of key customers would adversely impact revenue and income results.

Conclusion

Taking into consideration all the risks mentioned above, I do believe that VEEV is a viable investment at the moment.

I attribute the company to a blend of growth and value, high quality. The weak perspectives of growth are compensated by strong performance and margins, and undervaluation at the moment, due to:

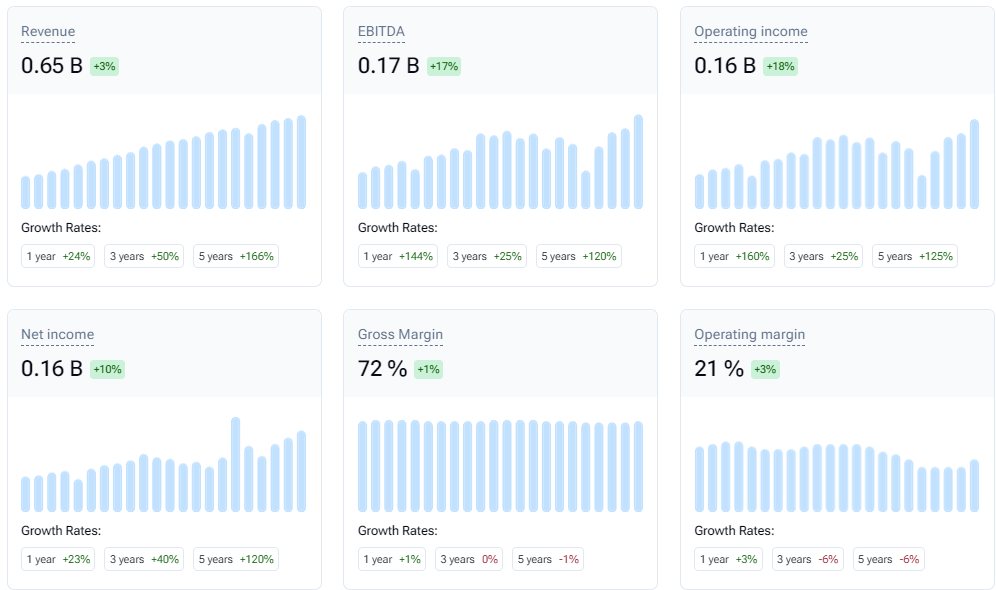

1) Consistent growth in revenue, EBITDA, and net income over the last five years, with solid margins and proved by cash flows from operations.

VEEV’s Profitability (Eyestock.io)

2) Solid balance sheet – the company is liquid and solvent with zero long-term debt.

3) Decreasing but still high efficiency – ROA 10%, ROE 12%.

4) Decreasing growth rates – low but stable growth rates (stability score 0.5).

This combination makes me comfortable to start looking for a buy below $193.85 per share.

Read the full article here