Please note all $ figures in $CAD, not $USD, unless otherwise stated.

Introduction

ATCO Ltd (OTCPK:ACLTF) (OTCPK:ACLLF) (TSX:ACO.X:CA) has been one of my preferred ways to play the unloved power and utility sector. Along with its interest in Canadian Utilities (CU:CA), ATCO owns several other businesses that I don’t think are fully appreciated in the market today. Since my initial coverage and ‘buy’ recommendation on ATCO’s stock back in January, shares have delivered a total return of 13.6% when compared with the S&P500’s return of 11.6%. With earnings just around the corner on August 8, I’d be a buyer of ATCO’s shares at the current price ahead of and into Q2 results.

Company Overview

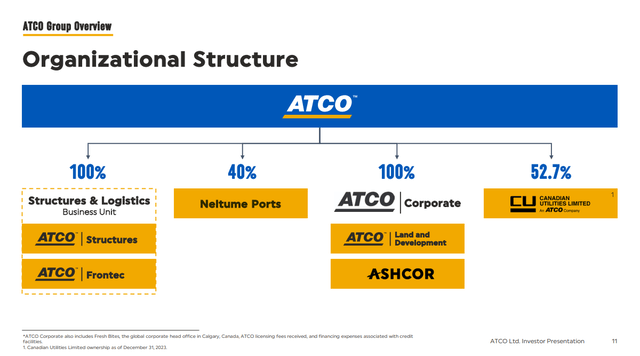

ATCO isn’t a household name. Investors can think of the company as a holding company that owns several businesses inside of it. The largest investment that ATCO holds is its 52.7% interest in Canadian Utilities, another company I’ve previously covered.

Canadian Utilities is one of the largest regulated utility companies in Canada and generates electricity for businesses and households. Along with generation, it also does transmission and distribution. CU has several non-regulated utility businesses in the renewables space that include hydro, solar, and wind, in addition to natural gas electricity generation assets in Western Canada, Australia, Mexico, and Chile.

The second part of ATCO’s business is the Structures and Logistics business. In this segment, ATCO is involved with workforce housing, space rentals, permanent modular construction, manufacturing solutions. This is mostly done through the ATCO Structures brand. In ATCO Frontec (also part of the Structures and Logistics segment), the company engages in facility operations and maintenance, workforce lodging, and support disaster and emergency management services. Typically, this has been a more volatile part of ATCO’s business, but it does provide some diversification outside of utilities.

ATCO also owns a minority 40% interest in a business called Neltume Ports, which is a port operator that does bulk and container cargo in South America (about 62% in Chile). The cargo breakdown is mostly container (44%), but also includes break bulk (25%) and bulk (31%).

Lastly, ATCO has a corporate segment that owns a basket we can think of as ‘other’, for simplification purposes. This includes ATCO Land and Development, where the company owns an interest in real estate assets including 11 commercial real estate properties, 20,000 square feet of industrial property, and 315 acres of land. Within this segment is also the company Ashcor brand, which does ready mixed concrete, soil stabilization, and oil well servicing out of repurposing ash, both “live” ash and reclaimed ash.

Investor Presentation

ATCO Q1 2024 Results

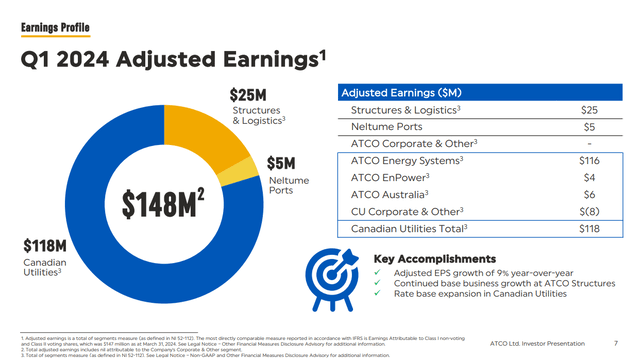

When looking at the latest quarterly results for ATCO (Q1’24), the company reported earnings per share of $1.32, which came in 2% higher than what analysts were expecting. Canadian Utilities made up 80% of the company’s $148 million in earnings, being that it’s ATCO’s largest investment.

Investor Presentation

At Canadian Utilities, the company’s Q1’24 quarterly results highlighted revenues of $1.09 billion, a 3.5% drop over last year. Lower natural gas storage revenues in addition to ATCO Enpower’s Forty Mile wind facility seeing lower prices during the quarter led to lower sales for Canadian Utilities. Lower capture pricing at Forty Mile was also a drag on first-quarter results. Rate-base growth, an increase in ROE, as well as lower operating expenses were an offset to negative drivers in the quarter.

EPS also was weak due to performance at the Electricity Generation, and earnings from the Puerto Rican equity investment being a bit lighter than expected also hindered results. Compared with Q1’23, the Natural Gas Transmission segment was impacted by the 2024-2025 GRA decision, while utility operations in Australia were impacted by inflation indexing and higher project costs.

Even though the quarter was only slightly better than expected at Canadian Utilities, I think ATCO’s Q1’24 was actually better, even in spite of the majority of the results being driven by CU. Why? Because of the other businesses ATCO owns, particularly in the Structures and Logistics business.

On the earnings call, management made a point of having Adam Beattie, the President, ATCO Structures, talk about the results of the segment and provide some color into the strength within the segment.

When we look at the total adjusted earnings for ATCO in Q1’24 of $148 million, up 8% versus last year, about $11 million of the growth came directly from the structures business and the Alberta Utility businesses. During the quarter, ATCO’s Structures and Logistics business reported adjusted earnings of $25 million, 25% higher than last year and contributing to $5 million of the growth in total earnings.

Within Structures, ATCO continues to see strong demand in the base business, delivering results that were more in line with the seasonal peaks that the company saw last year. With more units and an expanding footprint, average rental rates climbed 12%. Lower capex also meant that free cash flow for the segment also improved.

Outlook

In terms of the outlook, while management acknowledged the impact that the construction season has on the seasonality of its core business in S&L, the company continues to work towards balancing the business to reduce earnings volatility during the first and fourth quarters of the year. ATCO also noted that the sale trade activity business balances out the workforce housing stream of cashflows associated with relatively larger projects.

With respect to Triple M earnings, ATCO noted that the business continues to deliver reliable results and is performing above expectations that were set when the business was acquired. The company also mentioned the potential for modular housing to play a role in the housing crisis in Canada, and management continues to observe various factors such as housing supply and demand gap, incentives for first-time home buyers, and permitting policy changes that could support modular housing as a solution to tighten housing gaps.

Looking out to Q2’24, it wouldn’t surprise me to see between 5-6% growth in EPS, with greater contribution from Neltume Ports as well as the Structures & Logistics business, with greater activity and margins, along with incremental contributions from assets and ownership interests that have been acquired since last year. At Canadian Utilities, continued rate-base growth in the utilities, as well as increased earnings at the Distribution utilities compared to a cost-of-service rebasing year.

With Canadian Utilities specifically, I would continue to watch for progress on the Heartland Hydrogen Hub scheduled for FID target for mid-2025. My view is that this could have a material impact on earnings growth going forward, so any updates between now and then should be watched. Analyst estimates are projecting about 9.3% growth for Q2’24, so investors can expect Canadian Utilities’ growth to flip to positive next quarter. Compared to a cost-of-service rebasing year, growth in the Distribution utilities in the quarters to follow wouldn’t surprise me.

As for the risks to the investment thesis, the biggest risk I see is on interest rates. Most of ATCO’s debt is at the Canadian Utilities level, where the company carries net debt of $10.2 billion, for a Net Debt to EBITDA ratio of 5.1x. Compared to peers, this isn’t abnormally high for a power and utility company and so given a multi decade track record and the fact that interest rates are expected to come down. Just recently, the Bank of Canada cut interest rates 25bps to 4.50% and further cuts are expected for the rest of the year and into 2025.

Valuation

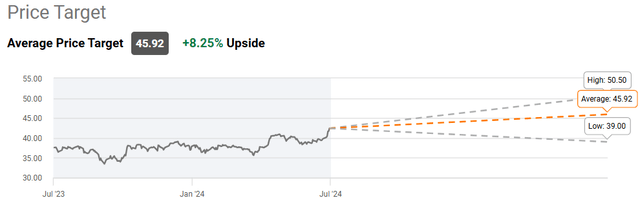

Based on the six analysts who cover the stock, there are three ‘buy’ ratings and three ‘hold’ ratings. The average price target is $45.92 with a high target of $50.50 and a low target of $39.00. From the current price to the average price target one year out, this implies about 8.3%, not including the current dividend yield.

Seeking Alpha

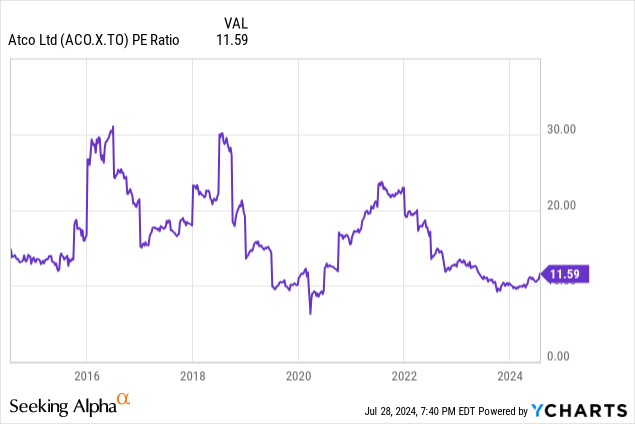

From a valuation perspective, I think ATCO’s valuation still makes a lot of sense, even after a 13% run up in shares since January. At the current price, ATCO’s valuation is about 11.6x earnings (about 11.2x adjusted). From a forward P/E perspective, given the growth analysts see at ATCO, the multiple is about 10.6x P/E. In my view, while this is still higher than the forward valuation of 9.0x we were looking at last time I reviewed the company, I continue to think shares offer compelling value.

Comparing ATCO to the rest of its peers, the company trades at one of the cheapest valuations. With higher AFFO yields and lower leverage in the capital structure, ATCO seems to have more of a margin of safety compared to peers. At the current price, my preference would be for ATCO over Canadian Utilities, particularly because investors aren’t overpaying for the other businesses, like the Structures and Logistics segment, which seems to be doing well.

Author, based on data from TD estimates

Conclusion

Altogether, I continue to rate shares of ATCO a ‘buy’ because of its valuation and improving businesses. While an investor could just own Canadian Utilities itself, I find ATCO to be the cheaper company, giving investors a higher dividend and more growth businesses through Structures & Logistics, Neltume Ports, and Ashcor. In addition, given a discount against other Canadian power and utility peers, I find ATCO to offer one of the best values in the sector, with potential for a rerating over time. While the sector as a whole is unloved for now, ATCO would be my preferred play for an investment in the space, particularly given the dividend yield of 4.6%, well covered by cash flows.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here