Investment action

I recommended a sell rating for Robert Half Inc. (NYSE:RHI) when I wrote about it in February, as I did not see any signs of recovery. RHI continued to see a poor revenue growth outlook, and EBIT was pressured due to the high fixed cost base. Based on my current outlook and analysis, I recommend a sell rating. I believe RHI’s stock price will continue to face pressure given the near-term uncertainties and current macro situation. Again, I am not seeing any strong signs of recovery that justify a rating upgrade. Weak staffing revenue trends have persisted into 3Q24, and that should continue to put pressure on margins.

Review

RHI reported 2Q24 earnings on 24th July, and the results were horrible, which makes my sell rating well-timed. 2Q24 revenue saw a 10% y/y decline on a current currency [CC] basis, driven by a 14% y/y decline in contract staffing (on a CC and same-day basis [SDB]), a 12% y/y CC SDB, and a ~1% y/y CC SDB decline in Protiviti. This drove EBIT margins to fall by 270 bps y/y to 6.2% as negative operating leverage continues to kick in (as per my expectation). As a result, EPS performance continues to disappoint, coming in at $0.66 vs consensus expectation of $0.71.

The outlook remains bleak for RHI as macro uncertainty continues to weigh on client confidence and budgets. The same situation where clients are exercising caution in hiring and elongating decision cycles persists, and the impact is clear in RHI results, where staffing revenue continues to see a mid-teens y/y decline. Notably, the trend has persisted into 3Q24 as temp staffing revenue continues to fall by 14% in the first two weeks of July (the same magnitude of decline as seen in 2Q24). While the US economy (RHI’s largest market) has shown positive GDP performance recently, I believe the true health of the economy remains weak as consumer spending continues to weaken, and consumer confidence has fallen to a low in July. Hence, from a bottom-up approach, this translates to lower demand for goods and services, which I see as a leading indicator for business hiring strength (lesser revenue should translate to a lesser need for labor, which means lower sales opportunity for RHI). Management 3Q24 guidance supports my view that the business is nowhere near the trough of this cycle yet. The guidance calls for total revenue in the range of $1.39 billion to $1.49 billion, implying a 9% decline on a CC SDB basis at the midpoint.

RHI is likely to see a repeat of margins falling in the coming quarters, given the revenue outlook. Remember that RHI is a high-fixed-cost business, as it needs high recruiters (labor costs) to drive growth. We have already seen how much damage can be done in 2Q24 as RHI saw sizable decremental margins (EBIT margins fell 270 bps y/y). Decremental margin should continue in 3Q24 as management continues to position the business for a potential recovery, sacrificing margins, as 3Q24 guidance implies a 230 bps y/y decline at the midpoint.

Note that while RHI revenue is down y/y for 7 consecutive quarters (3Q24 is expected to be done as well, so that makes it 8), based on historical trends (using the dot-com bubble as the benchmark), there is still room for two more quarters of y/y decline (revenue was down 10 consecutive quarters during the dot-com crisis).

Some bulls might point to the fact that job openings remain above pre-COVID levels, which is positive for hiring. I beg to differ, as job openings simply mean that businesses are open to hiring. The problem is that these openings are not being converted into actual hires, aka deferred demand. Management has spoken about this on the call as well. As such, I don’t think investors should use this as a basis to turn bullish on the stock.

They said, it feels like using a retail analogy, our clients have done due diligence, they’ve put something in their shopping cart, but they just won’t hit the submit button, indicative of, there’s deferred demand as we speak. 2Q24 call

Valuation

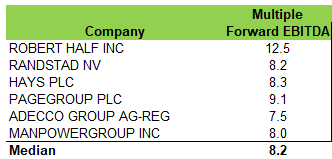

RHI is currently trading at ~13x forward EBITDA, 2.5x above its historical average, which I think is too excessive considering all the near-term uncertainties. I believe the market is overly confident that a turnaround will occur over the next 12 months. While this is possible, I am not a fan of being overly bullish at this stage. I should also note that whenever RHI’s forward EBITDA multiple reaches this level, it quickly converges back to its historical average. It is also trading at a premium multiple to where its peers are trading, suggesting plenty of room for multiples to fall if earnings remain poor for the next few quarters, which I think will happen given where the macro environment stands today.

Author’s work

Risk

I see the same upside risk for RHI, and that is a faster than expected macro recovery in the US. This risk is especially elevated today compared to the last time I wrote about the company, since 2H24 holds a few major events that could steer business confidence into a very positive region. For instance, lowering Fed rates is definitely a positive since it reduces the cost of capital for businesses. The resolution of the US election would also give businesses a better idea of the government’s intentions for policies that impact each industry. This removes uncertainty, but if negative policies are announced, it will impact business confidence.

Final thoughts

My recommendation is still a sell rating for RHI as 2Q24 performance remained weak. Persistent weakness in staffing revenue, coupled with RHI’s high fixed cost structure, also led to a significant margin decline. In my opinion, the outlook for the near-term remains bleak given the macroeconomic uncertainties, which are likely to further dampen client confidence and hiring activity. While job openings remain elevated, the conversion of these opportunities into actual hires has been sluggish. Also, RHI’s valuation is high relative to history and peers, which suggests plenty of room to fall. Therefore, I maintain a sell rating.

Read the full article here