Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the third week of July.

Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the closed-end fund (“CEF”) markets for perspectives across the broader income space.

Market Action

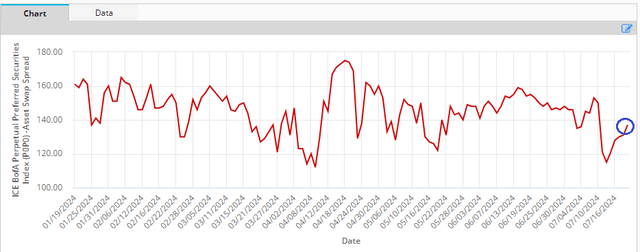

Preferreds were flat to slightly lower on the week as the drop in Treasury yields was largely offset by the rise in credit spreads amid general risk-off sentiment. Month-to-date, nearly all sub-sectors remain in the green.

ICE

Preferreds yields have not moved a whole lot recently, as the changes in Treasury yields and preferreds credit spreads have been largely offsetting.

Systematic Income Preferreds Tool

Market Themes

We tend to use the word “yield” when discussing bonds or term preferreds and this has created some confusion, judging by the comments. One question was simply what flavor of yield are we referring to when discussing securities with defined maturities?

There are lots of different yields in markets, and we use many versions as well in our discussions and service tools. This includes stripped yield, current yield, yield-to-call, yield-to-maturity, yield-to-worst, reset yield, pull-to-NAV yield, etc.

Whenever there is potential doubt about which version of yield we have in mind, we specify it. When there is no doubt, we just use “yield”. In discussions of term preferreds and bonds, there should be no doubt about which version of “yield” is being used in a general context because there is only one sensible use of the word yield in the context of securities with a maturity and that is yield-to-worst. Yield-to-worst is the “worse outcome” or, typically, the minimum of yield-to-maturity and yield-to-call. Yield-to-worst is not guaranteed to be the actual yield of a given security into its maturity (the security may not be redeemed as expected, for example), but it is the one definition that is used across the board to compare term securities to each other.

One view has it that “yield” in common parlance really means “ongoing yield” or “current yield” i.e., stripped yield, i.e., coupon/price. This view is uninformed, so we can put it aside. For one, “ongoing yield” is not a financial term. And two, no one in the professional fixed-income investing space means current yield when they say bond yield.

Current yield is not a sensible metric for bonds and would never be used in any context. Retail investors who grew up with CEFs may think that “yield” in the context of bonds also refers to current yield as it does in the CEF context, but that’s incorrect.

If anything, people should avoid using the word “yield” in the context of CEFs too, and say, “current yield” or, better, “distribution rate” since for the majority of CEFs, the distribution rate of the fund is far from its underlying portfolio yield. The word yield in the context of bonds or term preferreds is perfectly fine usage, and should always refer to yield-to-worst.

The second source of yield confusion has to do with preferreds trading at above “par” and past their first call date. We can illustrate it with the following BDC baby bond – OXSQZ. We show the bond’s yield-to-call as 3.3% and its yield-to-maturity as 8.24%. The question is then why bond’s yield-to-worst is equal to 8.24% rather than the lower yield-to-call of 3.3%.

Systematic Income Preferreds Tool

In this case, we don’t use the usual rule of yield-to-worst being the minimum of yield-to-call and yield-to-worst. The reason is that the yield-to-call for a bond that can be redeemed immediately at any point is not properly defined, as it’s a one-off return, rather than an ongoing yield.

If OXSQZ is redeemed, the more-or-less immediate (there will be a 30-day notice period) return to bondholders is +3% (i.e., $25 principal return / $24.17 clean price – 1). This immediate +3% return is not a worse outcome than an ongoing 8.24% yield-to-maturity – it’s a better outcome because on an annualized basis it’s much higher than 8.24%. This is why the “worse” outcome in this case is the 8.24% yield-to-maturity, and that is why that’s the yield-to-worst number for this bond.

If OXSQZ were trading at a $25.50 stripped price, the worse outcome here would be the redemption and an immediate 2% hit. In that case, the yield-to-worst would be -2%.

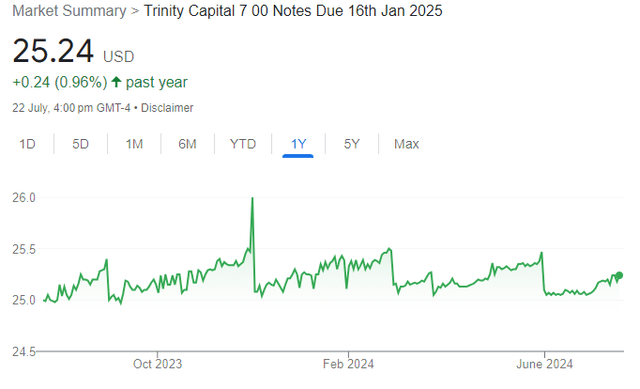

A final yield confusion has to do with whether to use the dirty price or clean / stripped price in yield calculations. Baby bonds, unlike OTC bonds, trade dirty, i.e., the price includes the accrued dividend which then drops out of the price on the ex-div date. This is why you often see quarterly sharp drops in baby bond prices such as the following. To properly calculate the bond’s yield, we need to remove the accrued dividend. For that, we also need to know the start of the accrual period, which typically coincides with the dividend payment date (not the ex-div date as would be expected). This last point has a fairly minor impact.

Google

Tracking baby bond yields is trickier than it looks at first glance, however, getting to grips with the right calculations puts investors in the best position to gauge value in the market.

Market Commentary

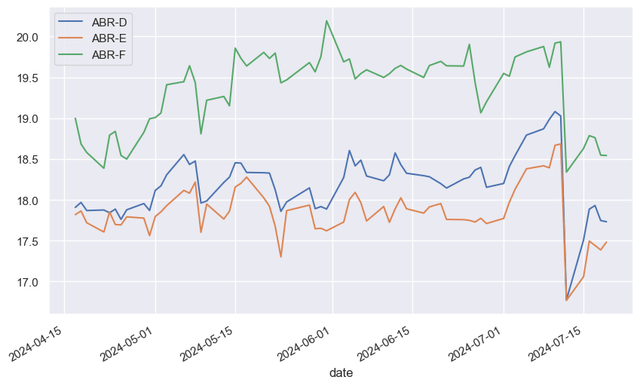

Mortgage REIT Arbor Realty Trust (ABR) shares fell sharply late last week on disclosure of a probe by the DOJ and FBI into the company’s loan portfolio, presumably the marks at which the loans are carried. Last Friday, the preferreds fell around 10% before recovering somewhat this week.

Systematic Income

Recall that a couple of short-sellers Viceroy and NINGI have been alleging for a long while that the value of the company’s loan portfolio is overstated. Viceroy has a lot of specifics in its commentary (which need to be taken with a grain of salt as there are some assumptions baked into the “facts”) however it’s hard to know what the full loan book looks like – there are always going to be individual problems, particularly in the current market with significant issues in the multi-family segment and a supply overhang.

The long outstanding criticism of ABR is its relatively low level of CECL balance (basically the amount of losses they expect in the portfolio) in the context of a large number of loan modifications. The consensus seems to be that book value is overstated, though perhaps not egregiously so, as auditors have been signing off. ABR’s strength is likely its $1bn+ cash position, which gives it a lot of options when faced with problematic loans. This means they won’t have to fire sale problematic assets halfway through renovation or construction.

An eventual drop in short-term rates could then improve liquidity and financing options, at least that’s the hope. Financing via CLOs is also a powerful non-recourse mitigant as it protects the rest of the company’s portfolio from individual problems. It seems unlikely the DOJ is going to deliver criminal convictions here given its track record during the GFC, and ABR could always point a finger at the auditor for signing off on the marks. At the same time, price weakness is likely to persist given the uncertainty around the probe.

Read the full article here