Today’s article revisits our stance on NerdWallet, Inc. (NASDAQ:NRDS), a FinTech company that provides financial product comparison tools and their intermediation. We previously covered the stock in June, assigning a bullish rating. However, material events have occurred since then, prompting us to revisit NerdWallet’s stock.

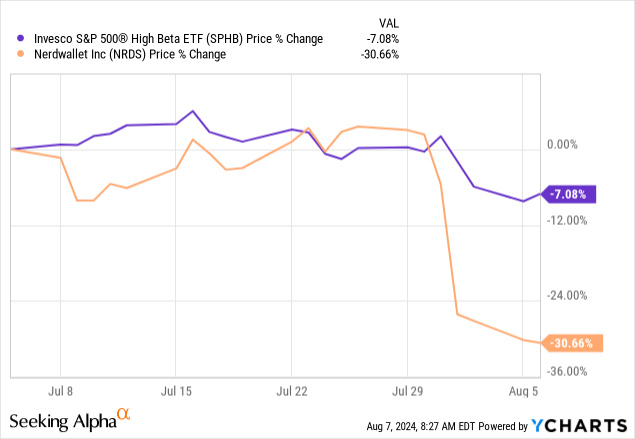

NerdWallet released its second-quarter earnings report on July 31, revealing a revenue beat of around $670,000 and an earnings-per-share miss of seven cents. The market didn’t like the event, as NerdWallet’s stock has lost nearly 15% of its market value in the past five trading days. Sure, a contemporaneous broad-based market downturn occurred. Nevertheless, NerdWallet’s decline warrants a revision.

Herewith are some of our latest findings.

Market Commentary: NerdWallet’s Recent Performance

As of the pre-market open on August 7th, NerdWallet’s stock has slumped from the $15.85 handle to around $10.81. The loss was abrupt and clearly signaled investor dissatisfaction with the company’s earnings report.

NRDS Stock Performance (Seeking Alpha)

Despite the material influence of NerdWallet’s earnings report, systematic risk must be considered. For example, many high-beta stocks slumped in the past month amid fears of a “market crash” and economic recession. As such, it can be argued that NerdWallet’s recent selloff isn’t solely due to the company’s structural concerns.

NerdWallet’s Q2 Earnings Revisited

Salient Data

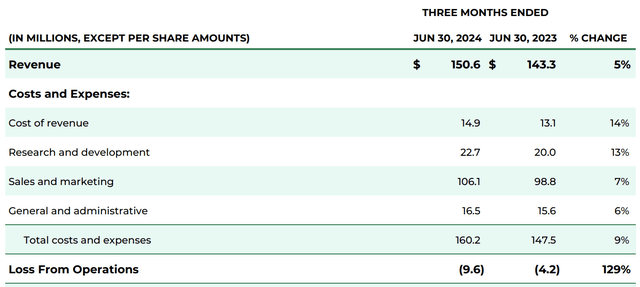

If measured on a year-over-year basis, NerdWallet experienced growth during its second quarter, with its monthly unique users (MUUs) and quarterly revenue growing by 7% and 5.09% apiece. However, the firm’s growth slowed, as its Q2 MUU growth is noticeably lower than the 9% it experienced a year earlier. Moreover, the firm’s revenue growth of 5.09% is substantially lower than the 14% it experienced a year ago.

| Metric | Value | Y/Y Change |

| Monthly Unique Users | 23 million | +7% |

| Revenue | $150.6 million | 5.09% |

| Cost of Revenue | 10% | +100 Basis Points |

Source: NerdWallet

The following diagram shows a time series of NerdWallet’s income statement; a discussion follows.

P&L (NerdWallet)

NerdWallet’s input costs grew across the board, leading to a 9% year-over-year increase in amalgamated operating costs and a 1.29x increase in its operating loss margin.

According to the firm’s management, the amortization of internally developed software spurred the cost of revenue. Furthermore, an increase in R&D occurred through enhanced investments in product and engineering, while SG&A expenses increased proportionately to the company’s revenue (in other words, it was likely due to growing company size and inflation).

Lastly, the company’s sales and marketing expenses increased by 200 basis points more than its revenue, primarily due to organic revenue expansion and horizontal integration. The latter pertains to the firm’s sum of parts being amalgamated into a “halo effect” for NerdWallet’s users.

Cost-Cutting Plan

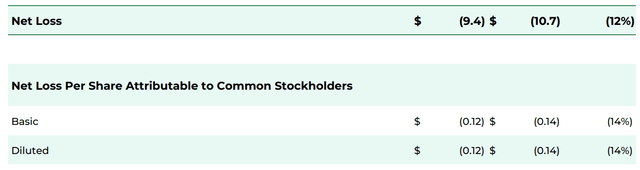

As already mentioned, NerdWallet missed its EPS target. However, it should also be noted that the firm’s loss and loss per share continued, sparking a cost-cutting plan.

P&L (NerdWallet)

The firm’s management plans to cut its workforce by 15% to improve its bottom line. However, the plan will likely entail an $8 million to $10 million restructuring charge, which might add risk to the overall process.

Although not explicitly stated, we think lower R&D costs are likely. Research and development costs are cyclical, and, therefore, we anticipate lower spending, given the firm’s loss and restructuring plan.

Our Take

Let’s start by discussing a few topline variables, more specifically, variables that we dislike.

The Bad

NerdWallet’s loan revenue slid by 6% year-over-year to $21.7 million. The segment consists of comparing and intermediating consumer loans, especially housing and student loans. We anticipate lower loan demand as the U.S. economy shows fragility through higher unemployment and waning business confidence. Additionally, we think credit spreads will resume their upward trajectory (due to economic softening and a recent drop in the yield curve), lowering bank risk tolerance and, in tandem, loan originations.

High-Yield OAS (St.Louis Fed)

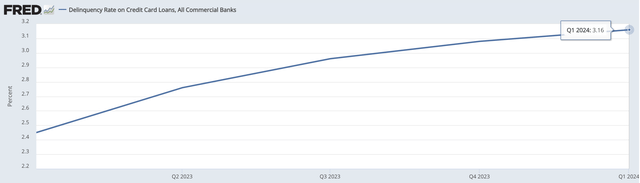

Furthermore, we dislike NerdWallet’s credit card exposure. The U.S. credit card delinquency rate rose to about 3.16% in Q3, up from 2.45% a year earlier. As with its loans division, NerdWallet’s credit card solutions might deteriorate amid rising credit and economic risk, leading to lower credit inquiries and fees. In fact, mild deterioration was already experienced in Q2 when credit card revenue declined by 10% year-over-year to $46.1 million.

Credit Card Delinquency Rate (St.Louis Fed)

Lastly, we dislike NerdWallet’s restructuring plan, as we think it will void an opportunity to ascertain additional market share. One of the pillars we based our previous analysis on was NerdWallet’s market share growth, and, therefore, we see a cost-cutting spree as a negative, especially if R&D is reduced.

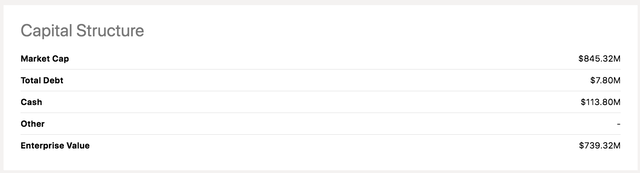

NerdWallet has a cash pile of more than $113 million, a low debt load, and a strong reputation. We think a fight for additional market share during tough market conditions would’ve been a better option.

Capital Structure (Seeking Alpha)

Aside: A strong reputation often allows easier access to the capital markets to fund a firm’s losses.

The Good

Okay, enough negativity for now; let’s look at a few positives.

As communicated in our previous analysis, we think NerdWallet has a great long-term concept whereby it uses the rising demand for financial education to leverage its intermediation. The company has experienced scintillating growth through Fundera and Barrelhead, two entities that operate as loan comparison vehicles.

Seeking Alpha

We see tremendous support through markets such as student loans, credit cards, and even home loan comparison tools. Although we anticipate a cyclical decline, we maintain our long-term view of the company’s growth story.

Earnings Metrics

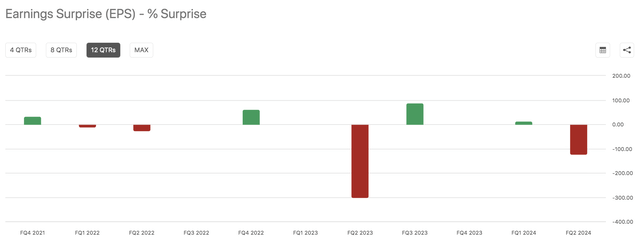

A glance at NerdWallet’s past earnings surprises shows that it regularly misses out on its earnings-per-share target. The stock has been listed for less than three years, meaning analysts have likely yet to establish a baseline earnings trajectory for NerdWallet. As such, I would cut it some slack for now. However, earnings momentum and stock momentum are often positively correlated. Therefore, recurring EPS misses might dent NerdWallet stock’s momentum.

Earnings Surprises (Seeking Alpha)

NRDS Stock Price Action

Valuation Metrics

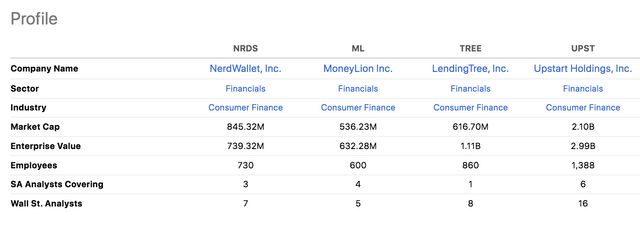

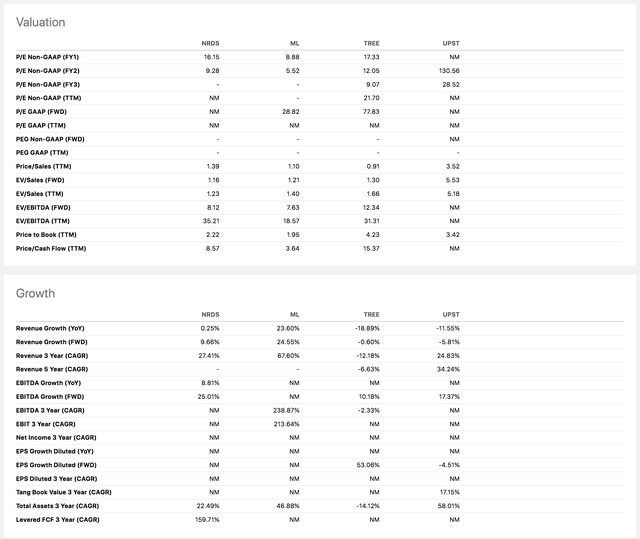

We decided to utilize a peer analysis to judge NerdWallet’s valuation. Among the selected constituents are MoneyLion (ML), LendingTree (TREE), and Upstart (UPST). The selected peers have idiosyncratic differences; however, we consider their end markets and company dynamics to be similar.

Peers (Seeking Alpha)

The following shows NerdWallet’s peer-based multiples; a discussion follows.

Click on Image To Enlarge (Seeking Alpha)

We don’t mind the look of NerdWallet’s valuation multiples. For example, it has a price-to-sales (P/S) ratio of 1.39x, which, in isolation, we consider low, especially considering the firm’s three-year compound annual growth rate (CAGR) of 27.41%. Moreover, NerdWallet’s P/S ratio is relatively in line with those of its peers, suggesting little evidence exists for it being grossly overvalued.

I dialed in on our P/S findings, as a growth firm’s top-line multiples can be telling. However, an additional multiple to look at is NerdWallet’s forward EV/EBITDA ratio of 8.12x, which is basically in line with or lower than those of its peers. Additionally, the firm has a forward EBITDA growth metric of 25.01%, which seems best-in-class.

I already told you why I focused on NerdWallet’s P/S, but why is the EV/EBITDA emphasized? Technology firms often engage in subjective amortization practices, which are factored out by EBITDA, making it a net income proxy. Moreover, the firm is unprofitable, adding additional utility to the multiple.

Other metrics should be considered before drawing a conclusion about NerdWallet’s valuation. Nevertheless, the ones we selected seem well-placed.

NerdWallet Stock Technical Analysis

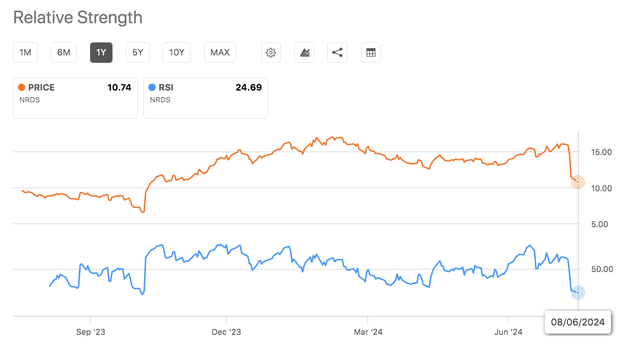

I want to share a few technical indicators to affirm the above.

Unsurprisingly, NerdWallet’s RSI has dipped below 30, suggesting the stock is oversold (30 is a theoretical boundary). Moreover, optimism has risen among options traders, as NerdWallet’s Put/Call Ratio has settled at 0.11.

RSI (Seeking Alpha)

We’ve gathered that some might bet on a bounce after NerdWallet’s abrupt decline. This isn’t surprising, as the stock’s RSI is completely depleted. However, we remain skeptical about a “buy the dip” narrative, as the current nature of the stock market’s influencing variables seems uncertain.

Final Word

Although we strongly dislike selling low and buying high, we have decided to soften our stance on NerdWallet’s stock. Factors such as the firm’s decision to downsize its spending and the exacerbated credit risk have prompted us to downgrade our outlook to neutral from our previous bullish consensus. This is a rare case where I/we would deviate from our contrarian nature, but NerdWallet’s parameters likely don’t justify a bullish rating.

Read the full article here