Introduction – EPRT, who are you?

Essential Properties Realty Trust (NYSE:EPRT) operates within the e-commerce/recession-resilient, service-oriented property sector. The Company is not as popular as some of its peers, like Agree Realty (ADC), Realty Income (O) or NNN REIT (NNN). As of June 2024, EPRT had 2009 properties across 49 states, with 96.4% of its ABR generated through triple-net leases.

For those unacquainted with the ‘triple-net’ lease term, it’s a highly favourable agreement type (from the landlord’s perspective) that involves the tenant covering the substantial costs related to operating and maintaining the property (incl. taxes, insurance, repairs, etc.). It’s especially attractive when combined with contractual rent escalators. For clarity, REITs grow through two main ways:

- externally – through acquisitions

- internally – through rent increases

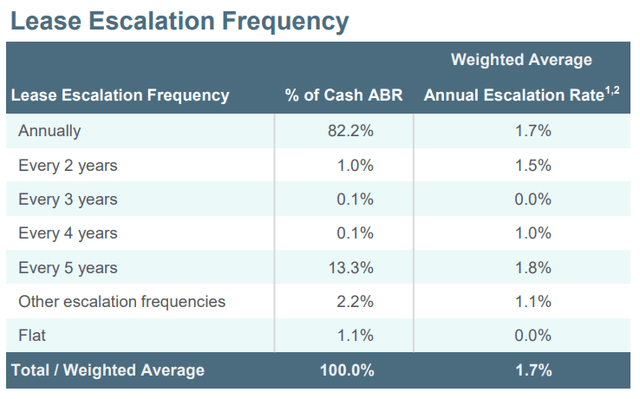

Regardless of the market rent growth, triple-net lease agreements typically include contractual rent escalators, ranging from 1% to 2% annually. Under the triple-net lease structure, such (seemingly low in the eyes of some investors) low single-digit increases tend to add up over time and significantly impact the bottom line. EPRT stands firmly in that area, with its weighted average annual rent escalators sticking to the higher end of the above range – they amounted to 1.7%.

EPRT’s Supplement to Q2 2024 Earnings

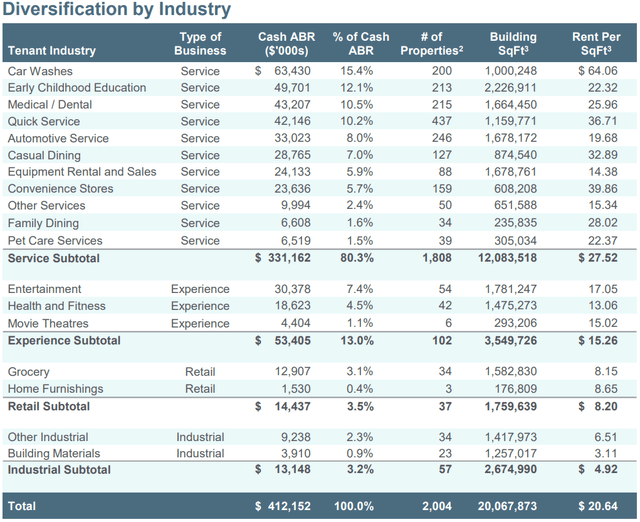

In terms of industry exposition, over 80% of EPRT’s ABR is derived from service-oriented tenants operating, inter alia:

- car washes (15.4% of ABR)

- early childhood education (12.1%)

- medical/dental services (10.5%)

- quick service (10.2%)

- automotive services (8%)

It also has some experiential, retail, or industrial exposition, with the last two responsible for ~6.7% of ABR. Therefore, it’s safe to say that EPRT’s tenants are e-commerce and recession-resilient. After all, people use such services (dental, medical, children-related, car-related, and many others) regardless of the economic environment, and the ‘Amazon Effect’ doesn’t apply to such services.

EPRT’s Supplement to Q2 2024 Earnings

Previous & Updated Thesis

Since the last time I covered EPRT (with a ‘buy’ rating assigned), the stock price has increased by 6.5%, constituting a total return of 7.6%.

Seeking Alpha, Cash Flow Venue

At the time, I recognised the effectiveness of its investment strategy and outstanding business & credit metrics. Upon the Q2 2024 earnings release, I decided that it was worth taking another look at EPRT’s business and evaluating my previous take.

With the key metrics upheld (or even improved) and a significant acceleration of investment activity at outstandingly attractive terms, I can’t say there’s anything essentially wrong with EPRT. The Company has very good things going for it – to name a few:

- high, positive investment spreads with plenty of safety margin

- one of the highest occupancy rates in the sector

- uncanny WALT

- investment-grade rated balance sheet with no upcoming maturities

- effective investment strategy reflected in the Q2 2024 investment volume and investment-related metrics

The only negative is that the entry point is higher, as the stock price has increased since my last publication. Nevertheless, it experienced a slight pull-back recently, so I believe that EPRT is still a reasonable addition to a well-structured portfolio. That is a ‘buy’ for me, but I don’t believe there’s a significant safety margin at the current prices, so it may be worth withholding until a slightly better valuation – depending on your investment approach, horizon, and personal goals. Enjoy the read!

Strong Second Quarter

Key metrics summary

In my view, EPRT’s Q2 2024 performance was marked by great investment activity, but before we dive into that, let’s summarize its key metrics. EPRT concentrates on middle-market tenants, so that can be considered a niche segment when compared to ADC, NNN, and O, as each of the above typically targets similar, larger tenants. Therefore, EPRT has significant negotiating power, which is well-reflected within the terms included in its agreements. Apart from the high contractual rent escalators (mentioned earlier), EPRT secured outstanding (for this property sector) lease terms. Its weighted average lease term (WALT) amounted to 14.1 years, which is noticeably higher than the level some of its peers recorded. For reference, please refer to the table below, summarizing the WALT for selected Q1 and Q2 2024 entities.

Author based on EPRT, NNN, and ADC

Although EPRT’s occupancy rate slightly declined, it still had one of its peers’ highest levels—at 99.8% as of June 2024. Please refer to the table below summarizing the occupancy rate.

Author based on EPRT, NNN, and ADC

Regarding the AFFO per share, EPRT recorded one of the highest growth dynamics across the sector, with a CAGR for the 2020-2023 period equal to 9.7%. The Company expects its AFFO per share to increase by another 5.2% in 2024 (vs 2023), which is a realistic scenario as its AFFO per share for 2024 YTD increased by ~5% compared to the same period of the previous year.

EPRT has a relatively modest dividend yield of ~4.0%, but it delivered solid DPS growth during the 2020-2023 period, recording a CAGR of 6.2%. Also, considering its very conservative AFFO payout ratio of ~66.4%, the dividend situation looks promising, and I expect further increases upholding the historical growth rate.

Author based on EPRT

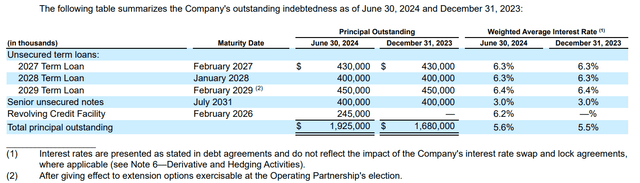

EPRT’s ability to uphold and increase the dividend is supported by its BBB rated balance sheet with no debt maturities upcoming until February 2027. Moreover, the debt maturing in 2027 already has a relatively high interest rate, so the refinancing impact (probably) won’t be negative. The only debt maturing earlier is the revolving credit facility, but it has two extension options, so it will probably be prolonged until, also, February 2027.

EPRT’s Q2 2024 10-Q

Robust Investment Activity

Overview – the gap between sellers’ and buyers’ expectations seems to be narrowing

The gap between buyers’ and sellers’ expectations is relatively wide during the high interest rate environment. This is a limiting factor for REITs as the growth potential resulting from their main external growth driver is tamed as the transactional market is more dormant.

That has been especially evident in the industrial property sector but also took its toll on the retail/service-oriented property sector. However, recent earnings releases of key segment players suggest that the abovementioned gap is narrowing. For example, ADC realised ~50% more investment volume during Q2 2024 than in Q1 2024. It was similar in the case of EPRT, which invested ~34.2% more during Q2 2024 than during Q1 2024. Total investment volume amounted to $333.9m during Q2 2024 – EPRT closed 35 transactions regarding 83 properties. Each transaction was a sale-leaseback deal, with 82% of them sourced through an existing relationship.

Moreover, the deals closed positively impacted EPRT’s metrics:

- WALT regarding these deals amounted to 17.8 (more than an average of 14.1)

- rent escalators amounted to 1.9% (more than an average of 1.7%)

Investment volume is one thing – investment spread is another

I like to prepare an illustrative estimate of investment spreads. In order to do that, we have to estimate the cost of capital of a given entity.

Assuming the cost of equity as an AFFO yield (AFFO per share guidance for 2024 divided by recent stock price) and the cost of debt based on EPRT’s credit rating, we arrive at WACC (weighted average cost of capital) equal to ~5.8%. Given the average cap rate of 8%, we get to an implied investment spread of 2.2%, which is very high and comes with a solid margin of safety. Please refer to the table below for details regarding the WACC and investment spread estimate for EPRT, ADC, and NNN.

Author based on EPRT, NNN, ADC, and Seeking Alpha

Both EPRT and ADC benefit over NNN in terms of their cost of equity, which leads to lower WACC and, as a result – higher spread.

Valuation outlook

As an M&A advisor, I usually rely on a multiple valuation method that is a leading tool in transaction processes, as it allows for accessible and market-driven benchmarking.

That said, the forward-looking P/FFO multiple stood at:

- 15.5x for EPRT

- 17.5x for ADC

- 13.9x for NNN

EPRT’s P/FFO multiple is noticeably higher than NNN’s, but I believe NNN will witness multiple appreciations in the upcoming months. Regarding ADC, I consider it this segment’s player that offers the most total return potential and is set to outperform its peers. To get a better grasp on my views on NNN and ADC, please refer to the links below:

- NNN: Great Pick For Stability-Seeking Investors

- Agree Realty Is Set To Outperform Its Peers: Here’s Why

As mentioned earlier, after the recent pull-back, there’s room for multiple appreciation for EPRT, but I believe that to be limited. I don’t see its multiple exceeding that of ADC. There’s still some upside potential, as EPRT is likely to exceed 16.0x P/FFO; however, it doesn’t come with as wide a safety margin as the last time I covered it. Nevertheless, that’s still a fair price for such a strong player.

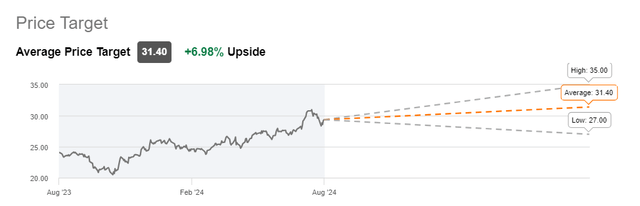

For a reference point, please see the chart below depicting the average expectations of Wall St. Analysts’ Ratings. I believe the average expected price target is attainable, but I would be skeptical about the $35 per share target.

Seeking Alpha

The Bottom Line

EPRT is quite fairly valued. It still has some upside potential resulting from the potential multiple appreciation, but it’s not as broad as it used to be. Its business keeps on striving and has great things going for it. To name a few:

- high, positive investment spreads with plenty of safety margin

- one of the highest occupancy rates in the sector

- uncanny WALT

- investment-grade rated balance sheet with no upcoming maturities

- effective investment strategy reflected in the Q2 2024 investment volume and investment-related metrics

EPRT remains a worth-considering addition to a well-structured portfolio. That’s a ‘buy’ rating from me, but as mentioned, it always depends on your investment approach and personal goals.

As each investment is, EPRT is accompanied by some risk factors:

- potential tenant issues could lead to a worse financial situation and higher stock price volatility. However, this risk remains limited as EPRT has a relatively low tenant concentration. Therefore, any tenant issues would have less impact on its financial stance

- A prolonged high-interest rate environment could hurt the business. Although EPRT is relatively safe on the financing front, that could impact the activity of the transactional market and, thus, EPRT’s growth prospects.

- any other material adverse changes that could lead to a worse financial stance and higher stock price volatility

Nevertheless, with recession resilient business model and top-tier metrics like EPRT’s, the Company is set to withstand many hardships. Thank you!

Read the full article here