NGL First Quarter Earnings Review:

NGL Partners (NYSE:NGL) reported an okay first quarter tonight (August 8th). Operationally, it looked similar to the Q4 report that I highlighted in my last public writeup on the company. Water dominated while crude oil logistics and liquids were marginal contributors. Part of this pattern is seasonal as fiscal Q1 and Q2 are the slowest quarters for liquids.

The company also reaffirmed the guidance for both water and overall adjusted EBITDA, and made good on remaining current on the preferred distributions, which were a big component of my last writeups. While the thesis has migrated from big capital return to income on the preferred (NYSE:NGL.PR.B) and (NGL.PR.C), I still think their low teens yield make for excellent low-risk total return investments. Meanwhile, the common (NGL) units, which have traded off on no news, have room to appreciate quite a bit. The company trades several turns of EBITDA cheap to other smaller MLP’s and every turn of EBITDA here is worth over 100% on the stock.

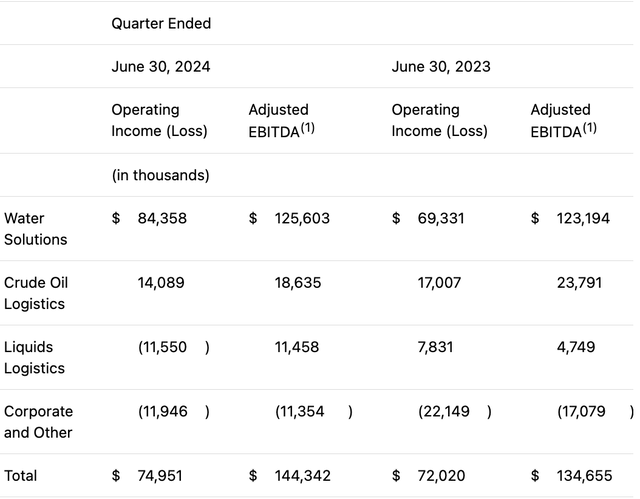

The company generated adjusted EBITDA of $144.3 million, compared to $134.7 million for the same quarter last year.

NGL Segment EBITDA (NGL Quarterly Earnings Letter)

As usual water was the biggest component. Its EBITDA was $125.6 million, up slightly from $123.2 million last year. Processed barrels per day increased 0.3%. Water disposal services fees declined due to lower fees due to the expiration of higher fee per barrel contracts replaced with lower fee per barrel contracts but with an extended term and higher volumes. DJ Basin water volumes declined as certain producers reused their water in their operations. Higher volumes of produced water came from contracted customers in the Eagle Ford Basin and Delaware Basin, plus higher fees from interruptible spot volumes. Some producers also paid for committed volumes not delivered. The company did not specify where these take or pay payments came from.

Water was helped by recovered skim oil, including profits from skim oil hedges, which totaled $30.7 million versus $7.7 million last year. Both higher skim oil recovered from increased produced water processed and higher realized crude oil prices selling the skim oil barrels helped.

Oil storage and liquids are still mediocre at best. I hate these businesses and long for the day that they are sold. The good news is they constituted about 20% of EBITDA combined before considering corporate overhead.

As mentioned above, the company reaffirmed our guidance for Fiscal 2025 with Water Solutions adjusted EBITDA to a range of $550 – $560 million and full-year adjusted EBITDA of $665 million. Clearly, the company doesn’t expect material recovery in either oil of liquids. Water will have to pick up the pace a little to hit that targeted range, but the LEX II water pipeline comes on line in October with initial capacity of 200,000 barrels per day. That capacity will be expandable to 500,000 barrels.

NGL Balance Sheet and Capital Usage:

The balance sheet was largely unchanged except for the accrued preferred distributions being paid. The company is about 4.5x leveraged on $665 million of EBITDA. The D preferred are a little bit less than another turn of EBITDA. EBITDA minus $270 million of cash interest, $60 million of maintenance cap ex and a smattering of taxes should leave about $330 million. Back out about $70 million of preferred distributions and another $150 million of growth cap ex will leave about $100 million to pay down the D’s. This free cash will increase once the LEX II pipeline is in service as that comprises 60% ($90 million) of the growth cap ex budget.

The company reiterated during the conference call that paying down the D’s will be the priority for excess cash flow. Selling liquids and oil logistics for any halfway decent multiple would allow the company to get rid of the D preferred and restart a common distribution.

The company renegotiated its bank line this week to reduce the spread over SOFR from 4.50% to 3.75% on its Term Loan B. There is $700 million outstanding under this facility, so this lower spread will save $5.25 million. In the context of the free cash flow I broke down above, that $5 million means something.

Valuation:

Valuation has come down with the unit price over the past few week. Clearly expectations were low for this quarter. I think the company didn’t really surprise anyone either way.

| Market Cap (@ $4.18/unit) | $554 million |

| Cash | 5 million |

| Preferred | 900 million |

| Minority interest | 20 million |

| Debt | 3.1 billion |

| Enterprise Value | $4.569 billion |

| EV/2025 Fiscal Year EBITDA (using $665 million) | 6.87x |

| Normalized Free Cash Yield (Using $190 million) | 34.2% |

These valuations are very cheap compared to other MLP’s like MPLX (MPLX), CrossAmerica Partners (CAPL), Sunoco (SUN), which all trade over 9x EBITDA. The discount is particularly out of place now that all the debt is refinanced, the accrued preferred distributions are paid, and the company is generating enough cash to pay all capital projects, preferred distributions and pay down the D preferred with internal funds.

Risk:

The risk here is a slowdown of drilling activity, particularly in the Delaware basin. The unit prices are also susceptible to oil price volatility.

Conclusion:

I still like the units and the series B preferred here. The B’s are amazing yield here and their distributions seem pretty safe now. The C series are cheap too but much less liquid than the B’s.

I wouldn’t expect a common distribution or major buyback any time soon, at least until the D’s are paid down, but at close to a 35% fcf yield, purchases of the D’s will accrete to the value of the equity dollar for dollar holding the multiple steady.

Read the full article here