Wolverine World Wide, Inc. (NYSE:WWW) reported the company’s Q2 results on the 7th of August in pre-market hours, beating Wall Street revenue and EPS estimates by a considerable margin. Yet, the stock fell by -7% to the results, seemingly as the brands’ sales declines still don’t have a near-term end in sight.

In my previous article on the stock, “Wolverine World Wide: Sales Improvements Need To Start Showing Soon,” I remained at a Hold rating for Wolverine as the turnaround potential was nearly fairly valued with a significant uptick in product development and branding activity, especially for the Saucony and Wolverine brands. Yet, I highlighted the needed urgency for the improvements for the investment case to seem worthy. Since the article was published on the 25th of June, the stock has now lost -10% of its value, compared to the S&P 500’s (SP500) return of -2%.

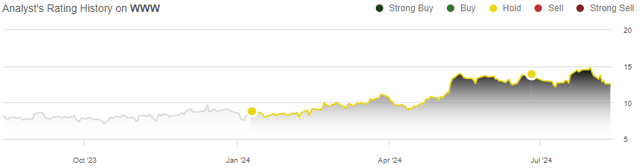

My Rating History on WWW (Seeking Alpha)

Q2 Financials: Continued Sales Weakness, But a Sequential Improvement

Wolverine’s Q2 results showed an -18.4% organic year-on-year revenue decline into $424.8 million, still showing considerable weakness across the line. The adjusted EPS came in at $0.15, $0.04 below the Q2/2023 EPS. The financials still came in above Wall Street’s expectations as revenues beat by a considerable $14.4 million margin, and the adjusted EPS consequently beat Wall Street estimates by $0.04 with less negative operating leverage than expected. A part of the beat, as discussed in the Q2 earnings call, was due to a distribution center transition not pushing $5 million of sales into Q3 as was previously expected.

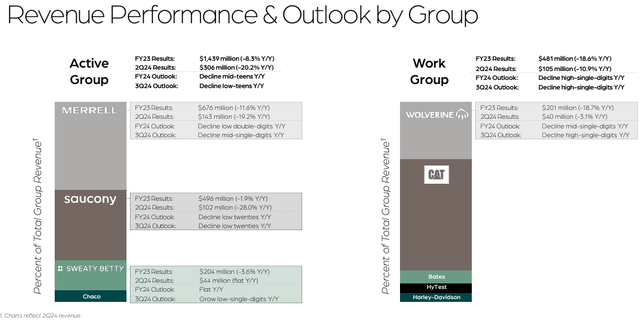

By brand, Merrell’s sales declined -19.2% compared to a guided low-twenties Q2 decline outlook, communicated in the Q1 investor presentation, showing a slight outlook beat. Saucony’s sales declined -28.0% compared to a low-thirties decline outlook, also beating the company’s given outlook. The Wolverine brand reported a small -3.1% decline, showing especially good signs compared to the given high single-digit decline outlook – while not very significant at just 9.4% of Q2 ongoing sales, the brand is showing healthy signs of a return to growth.

Sweaty Betty sales stayed flat compared to a low-single-digit growth outlook, being a small hiccup in the company’s Q2 performance against the given brand-specific outlook, driven by slightly weaker-than-expected retail sales for the brand.

In my opinion, the sales performance was overall fair considering the already guided-for weakness and some turbulence in the industry, especially in wholesale. The quarterly report also already saw a good sequential improvement from a -24.5% organic revenue decline in Q1, albeit with a weaker comparison period in Q2 enabling a lower decline. The company still has ways to go to improve into a healthily performing group of brands, but the Q2 results showed some good signs sequentially.

Underlying Profitability Continued Improving in Q2

Despite an adjusted EPS decline year-on-year, Wolverine’s underlying profitability is clearly improving, for now, countered by the continued sales declines. The adjusted gross margin elevated by a great 400 basis points to 43.1%, and operating expenses deleveraged nearly along with revenues with a -15.2% decline; expecting a revenue recovery in the midterm, the gross margin expansion leaves good room for margin expansion as well.

Wolverine’s Clear Focus on Saucony Was Highlighted in Q2 Call

Wolverine’s primary focus is clearly on Saucony, as I already previously noted with the rapid product launches for the brand. The Q2 earnings call focused very intensively on the brand, as the brand was mentioned a whole 47 times in the call.

In terms of product pipeline innovation, Wolverine communicated in the call that Saucony is the furthest along, clearly already shown by the continued launches including a redesigned Hurricane 24 announced after my previous article. While older product lines seem to really struggle, new product introductions were communicated to have driven a 900 basis point increase in revenue contribution in Q2, with especially good momentum seen in the UK.

Saucony’s launches were communicated to have seen good sell-through overall as well, building a position for improving overall momentum for Saucony. The new product launches and updated branding seem to have worked so far amid Wolverine’s turn into a renewed offering.

Yet, the company continued losing share at the -28.0% Q2 revenue decline to rapidly growing new brands in the space, including Deckers’ (DECK) HOKA brand that had a 29.7% growth in the most recent reported quarter, and On Holding’s (ONON) similar 29.4% constant currency growth. Competitors appear to be innovating more in the running shoes category, and Saucony’s new launches’ success can’t yet be taken at face value, despite good initial sell-through. A good performance is still needed to drive Saucony back to total revenue growth at a good overall scale of revenues.

I believe that some cautious optimism is in place for Saucony, although major shifts in total brand growth are still likely pushed towards 2025 at the soonest, and growing competition in the space acts as a considerable threat.

Slight 2024 Outlook Adjustment Doesn’t Raise Eyebrows

Wolverine adjusted the 2024 outlook slightly, now expecting revenues of $1.71-1.73 billion instead of $1.68-1.73 billion. While the adjusted gross margin again stands at 44.5%, the operating margin outlook has risen to 6.0% from 5.7% previously due to the higher sales mid-point. The adjusted EPS guidance’s lower bound was raised by 10 cents into the current $0.75-0.85 adjusted EPS range.

WWW Q2 Investor Presentation

Yet, the brands’ guided 2024 sales performances stay the same. With the Q2 revenue beat, the updated outlook expects a very similar performance as previously for H2. In my opinion, the guidance change was very non-significant, and even missed Wall Street analysts’ expected 2024 figures despite a narrowing to the upside.

Updated Valuation: WWW Comes at a Fair Margin of Safety

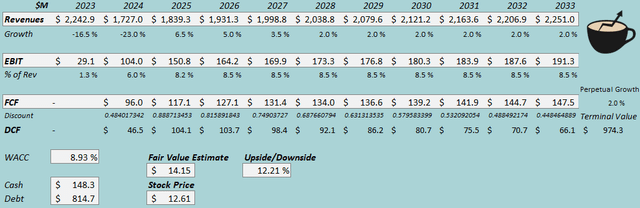

I updated my discounted cash flow [DCF] model slightly, now estimating a -23% revenue decline in 2024 instead of -24% previously due to the updated outlook. Afterward, I estimate similar growth with a midterm sales recovery, only pushing the 2025 growth outlook down by 0.5 percentage points due to the recovery being pushed slightly more into 2024.

I again estimate similar margins at an 8.5% EBIT margin level eventually, with slightly improved short-term estimates.

For more thorough explanations of the estimates, I refer to my previous, and initial articles on Wolverine.

DCF Model (Author’s Calculation)

The estimates put Wolverine’s fair value at $15.15, 12% above the stock price at the time of writing. While the estimate shows some upside, I believe that a good margin of safety for the estimated recovery is justifiably priced in amid still weakly performing brands.

The fair value estimate is up from $12.85 previously.

CAPM

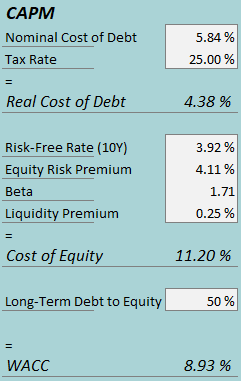

A weighted average cost of capital of 8.93% is used in the DCF model, down from 9.32% previously. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2, Wolverine had $11.9 million in interest expenses, making the company’s interest rate 5.84% with the current amount of interest-bearing debt. I now estimate a 50% long-term debt-to-equity ratio instead of 60% previously as Wolverine has paid down debt quite well despite outstanding weakness.

To estimate the cost of equity, I use the 10-year bond yield of 3.92% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. I have kept the beta estimate at 1.71. With a liquidity premium of 0.25%, the cost of equity stands at 11.20% and the WACC at 8.93%.

Takeaway

Wolverine World Wide, Inc.’s Q2 results showed a slightly less bad performance than Wall Street and the company itself anticipated, already improving growth well sequentially in part due to a weaker comparison level. The 2024 guidance’s revenue and EPS mid-points were also slightly raised, although not at a meaningful level or one that Wall Street seemed to anticipate. Wall Street analysts are still turning positive on the stock, driven by likely nearing inflection in the renewed brands amid Saucony’s extensive reinvention. The stock remains valued near fairly with a small margin of safety, and as such, I remain with a Hold rating for Wolverine World Wide.

Read the full article here