Introduction

Buckle up! It’s time to discuss natural gas.

Although I promised I would focus more on non-energy investments, I want to take a detour to update my thesis on what may be one of the most volatile stocks on my radar: Antero Resources (NYSE:AR).

My most recent article on this company was written on June 9, when I went with the title “Why Antero Resources Is One Of My Highest Conviction Ideas.”

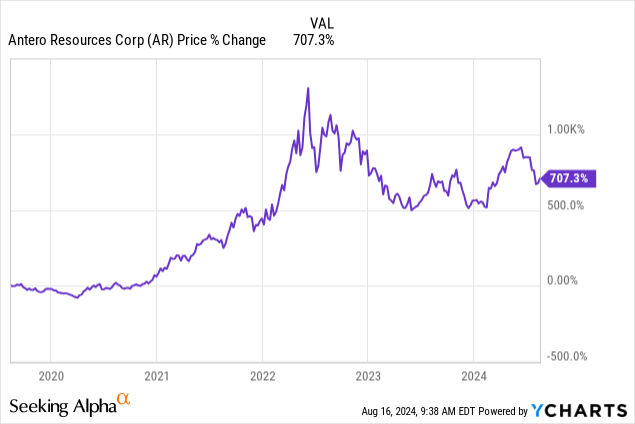

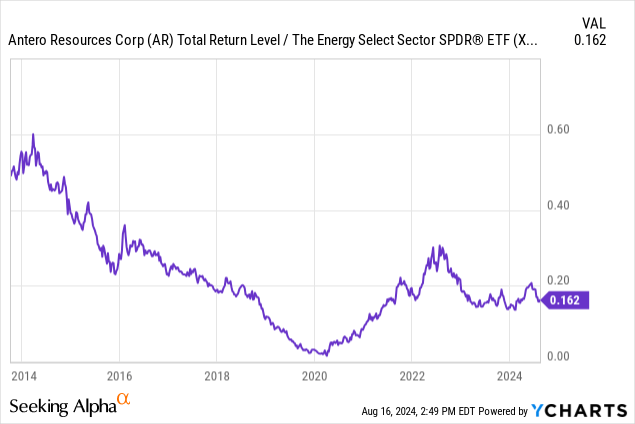

Since then, shares have fallen 19%, putting a dent in my thesis.

However, since my February article, shares are still up 16%. Over the past five years, the AR stock price has risen by more than 700%, partially due to the fact that it bottomed after a devastating long-term downtrend.

Although the share price has struggled since my June article, I believe this is nothing but another bump in the road. In this case, caused by weakening natural gas prices.

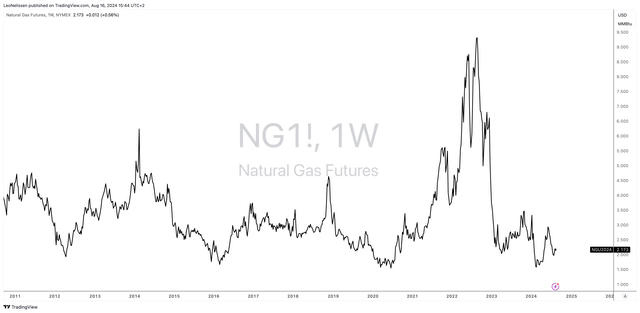

As we can see below, NYMEX Henry Hub prices are in the low $2 range again, slightly below the long-term average.

TradingView (NYMEX Henry Hub)

Despite significant tailwinds from data center power demand, the war in Ukraine, and higher LNG exports, this clean-burning fossil fuel cannot catch a break.

Moreover, as I have four major investments in the energy space (two Permian Basin royalty/land plays, one Canadian oil/gas producer, and one midstream company in the gas sector), being on top of these developments is key.

Hence, in this article, we’ll do two things.

- Assess the natural gas bull case.

- Discuss what makes Antero Resources such a fantastic natural gas stock.

It also helps that AR recently reported its 2Q24 earnings, which adds a lot more data and commentary to work with.

So, let’s dive into the details!

The Natural Gas Bull Case Remains Strong

Although I’m bullish on natural gas, I’ve always made the case that people should not trade the commodity or invest in producers unless they are fully aware of the risks.

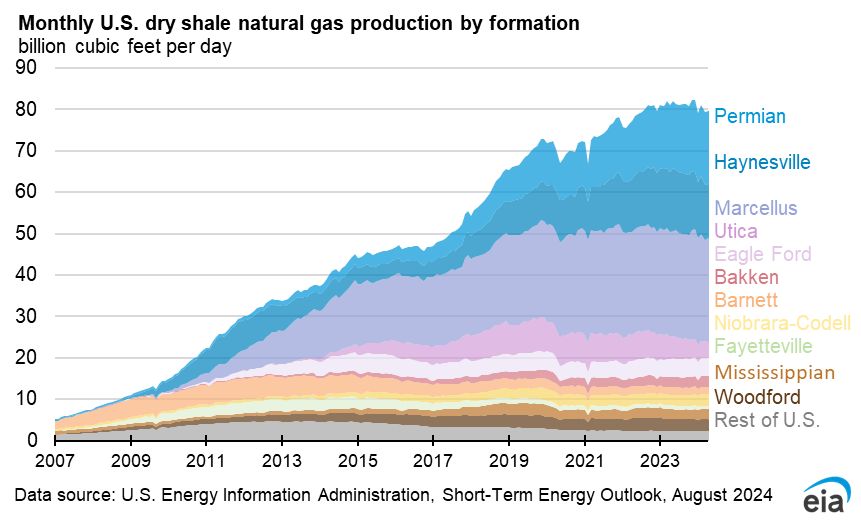

As the chart above shows, natural gas is one of the most volatile commodities in the world. While demand is strong, supply has been a major issue. The problem is the abundance of natural gas. Unlike oil, which is seeing lower global output growth, natural gas production has remained very strong after the pandemic.

Since 2020, dry shale natural gas production in the United States has risen from roughly 70 billion cubic feet per day to 80 million cubic feet per day.

Energy Information Administration

Now, it looks like natural gas production has peaked – at least for the time being.

One driver of this is lower prices, making it less attractive for many players to maintain the same production rates.

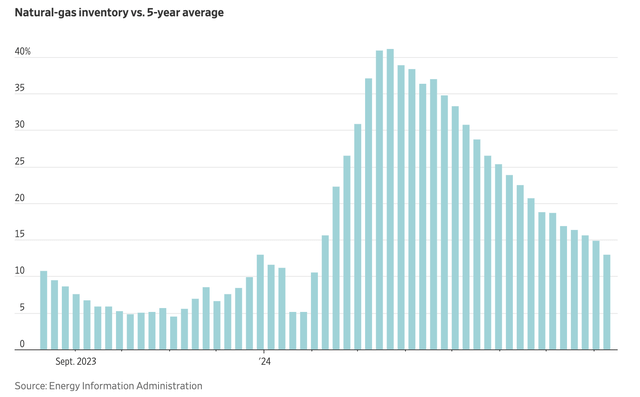

This has finally lowered natural gas stockpiles in the United States.

The U.S. drew down natural gas stockpiles last week for the first time during the summer since 2016, according to the Energy Information Administration, taking a big bite out of the surplus that has weighed on prices for the power-generation fuel.

An abundance of gas left over from winter has withstood some of the hottest weather on record and weighed on prices, prompting big drillers like Chesapeake Energy and Coterra Energy to curtail output.

The production cuts have begun to eat into the glut and lifted gas-futures prices by more than 15% since the start of last week. – The Wall Street Journal

The Wall Street Journal

On the demand side, artificial intelligence is turning into the biggest driver of growth.

AI data centers alone are expected to add about 323 terawatt hours of electricity demand in the U.S. by 2030, according to Wells Fargo. The forecast power demand from AI alone is seven times greater than New York City’s current annual electricity consumption of 48 terawatt hours. Goldman Sachs projects that data centers will represent 8% of total U.S. electricity consumption by the end of the decade. – CNBC (emphasis added)

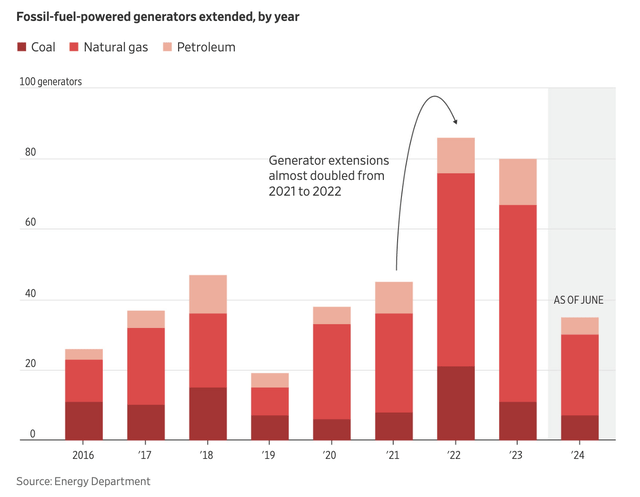

As a result, fossil-fueled power plants are seeing life extensions.

The Wall Street Journal

In light of everything we have discussed so far, Goehring & Rozencwajg make the case for the perfect bull thesis, supported by both demand and supply tailwinds. I added emphasis to the quote below:

In our view, US natural gas demand is set to grow at the fastest rate in history between now and 2030. At the same time, dry gas production appears to have peaked. While analysts are hopeful that a rebound is forthcoming, we are not as optimistic. The shale gas revolution resulted in a dramatic increase in supply, but as we have argued, immense is not the same as infinite. More than half of reserve estimates have now been produced in every major shale basin, an event that has corresponded historically with falling production. If our models are correct, and we believe they are, the most significant gas demand increase in history will occur just as production begins to falter. -Goehring & Rozencwajg

Although I expect that efficiency gains and potentially higher natural gas prices in the future could cause production to rise further, there is no denying that the long-term bull case keeps getting better.

Hence, I’m increasingly focused on low-cost producers with fantastic business models. One of them is Antero Resources.

What Makes Antero Resources So Special

When it comes to investing in the volatile natural gas space, I care about a few characteristics.

- I want producers with extremely low breakeven prices.

- I want producers with deep reserves.

- I want producers with healthy balance sheets.

- I want these producers to reward shareholders through dividends and/or buybacks.

Antero has all of this.

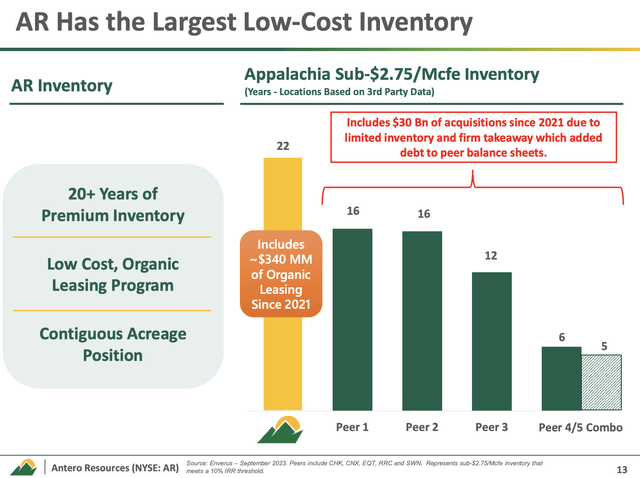

The company has 22 years’ worth of premium inventory in the Appalachia region, the most important natural gas basin in the United States.

This does not mean the company will run out of natural gas to produce after 20 years. What this means is that the company has 22 years of inventory that is breakeven below $2.75/Mcfe. This also excludes any new discoveries.

Antero Resources

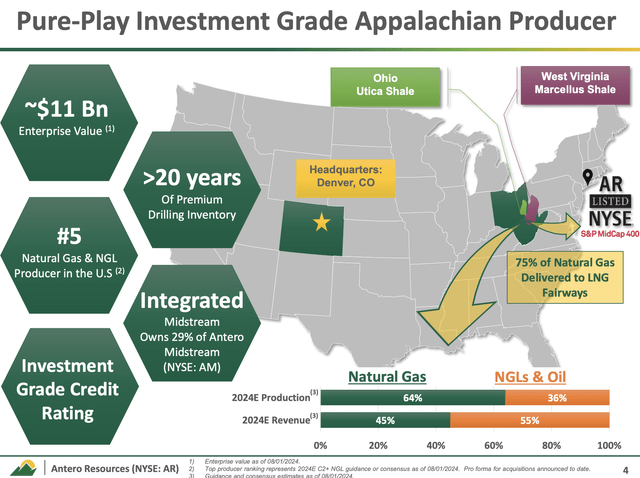

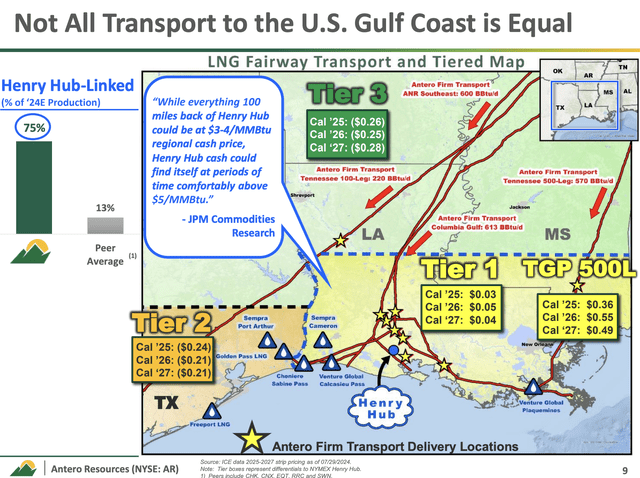

Even better, as we will discuss in this article, roughly 75% of its production is sold out of its basin to attractive markets like the LNG Fairway. The peer average is 13%.

On top of that, more than a third of its production consists of high-margin natural gas liquids (“NGL”), which account for more than half of the expected 2024 revenue.

Antero Resources

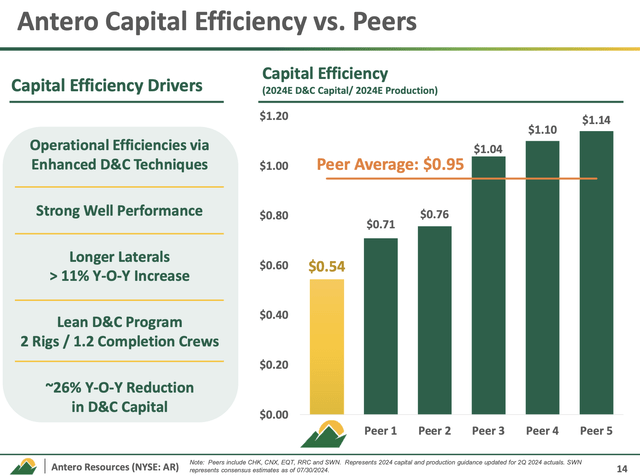

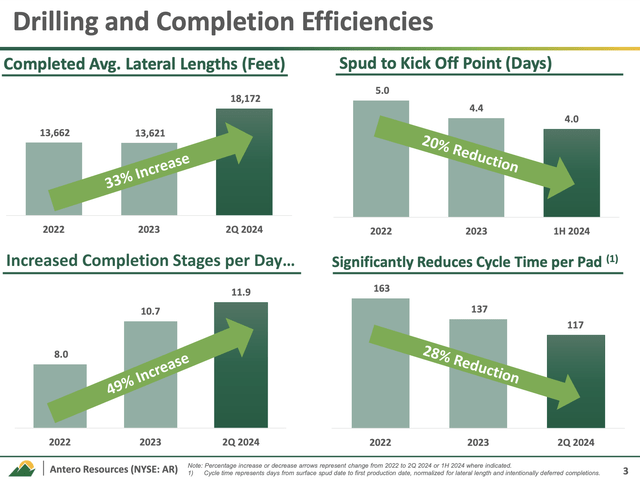

Moreover, when it comes to capital spending, the company has the lowest drilling and completion costs among its peers in the United States – by a significant margin.

Antero Resources

In the second quarter, the company continued to streamline its operations by reducing the average drilling time from spud to kickoff point to four days, down from 4.4 days in 2023.

On the completion side, Antero set another quarterly record by averaging 11.9 stages per day, which is a significant improvement from the 10.7 stages per day it saw in the previous year.

In general, it’s a fantastic example of increasing efficiencies in the oil and gas industry.

Antero Resources

Moreover, because the company has elevated NGL exposure, it benefits from higher-margin output. That’s very beneficial in an environment of subdued natural gas prices.

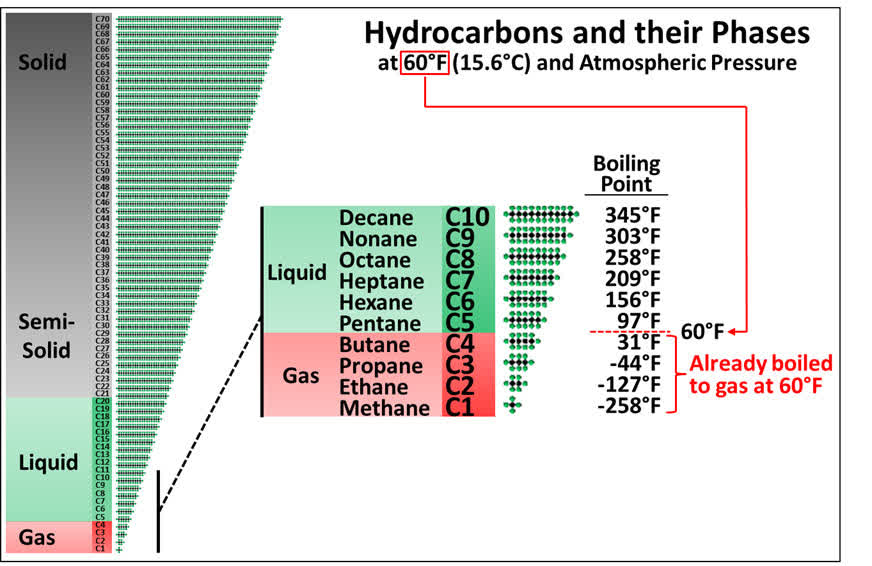

During its 2Q24 earnings call, the company noted it has benefited from strong propane exports, which have been a major tailwind for its C3+ price realizations this year. Please note that C3 means propane. It’s an indication of hydrocarbons based on the number of carbon molecules. C6, for example, is hexane.

Energy Training Resources

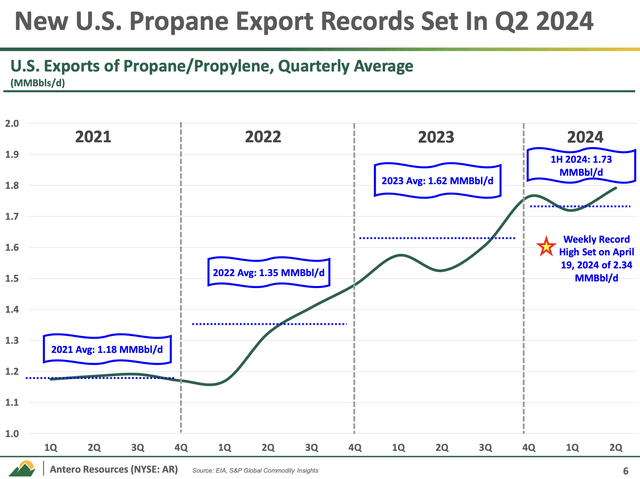

With more than 50% of its C3+ production (mainly propane) being exported via the Marcus Hook terminal in Pennsylvania, Antero is shielded from capacity constraints that currently impact the Gulf Coast. That’s another major benefit that is often overlooked.

Antero Resources

Because of these benefits, the company enjoys premium pricing, which allowed it to keep its negative free cash flow to a loss of $59 million in the first half of this year. That’s a poor number but better than all major peers (see below).

Antero Resources

Despite weak natural gas prices in the first half, the company managed to achieve a significant uplift of $1.10 per Mcf due to strong C3+ NGL prices.

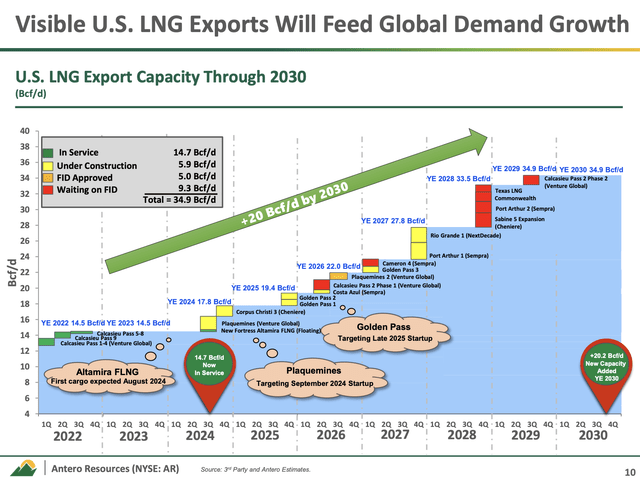

Moreover, as I already briefly mentioned, Antero Resources is a major winner of the LNG trend.

During its earnings call, the company noted it holds 570,000 MMBtu per day of firm delivery to the TGP 500L pool, which represents 63% of the supply feeding the Kinder Morgan TGP Evangeline Pass Phase 1 project at the Plaquemine LNG facility.

Through 2030, the United States is expected to add another 20 billion cubic feet per day in LNG export capacity, roughly twice its current capacity.

Antero Resources

In general, Antero Resources is in a great spot to benefit from the widening price spread between sales points near Henry Hub and those outside this premium market.

According to the company, this spread has already seen premiums of more than $0.50 per MMBtu for the 2025-2027 forward curve. That is a significant increase from the under $0.10 per MMBtu premium the company saw a year ago.

Antero Resources

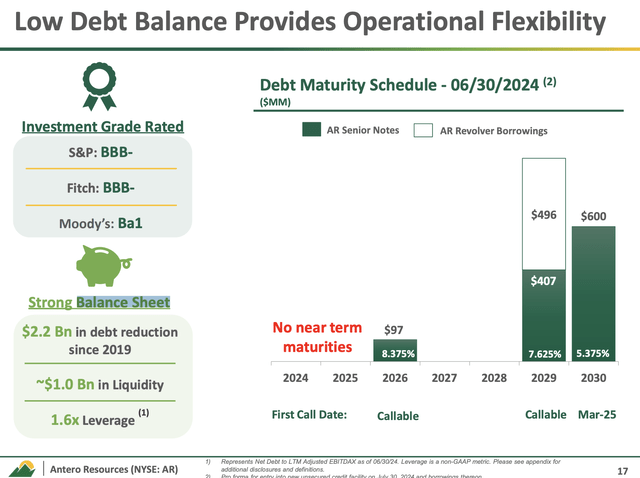

Moreover, the company has received an investment-grade credit rating of BBB-. In June, the fifth credit rating hike since 2020 made it an investment-grade company.

This is a truly impressive trend supported by a debt reduction of more than $2 billion since 2019.

This balance sheet comes with roughly $1.0 billion in liquidity, a leverage ratio of just 1.6x EBITDAX, and no significant debt maturities until 2029!

Antero Resources

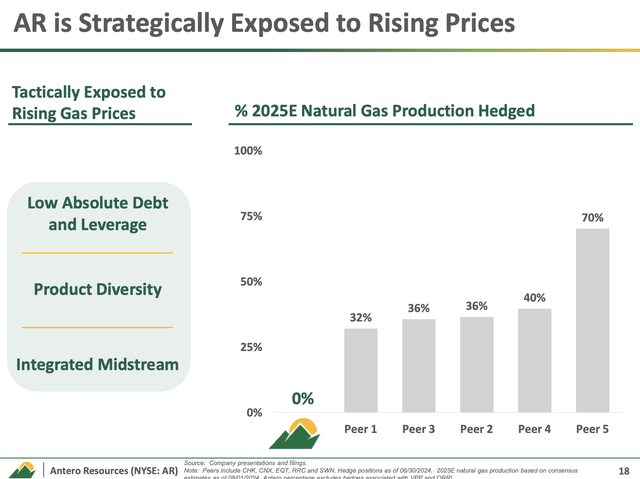

On top of that, the company has no hedges. Of its 2025 production nothing has been hedged. Its closest peer has hedged 32% of its production.

Although this is a huge disadvantage when prices are declining, I believe it’s a huge pro for people who have a bullish thesis on natural gas. The absence of hedges provides much more upside potential.

Antero Resources

As Antero Resources has industry-leading breakeven prices and a very healthy balance sheet, it can take the risk of not hedging its production.

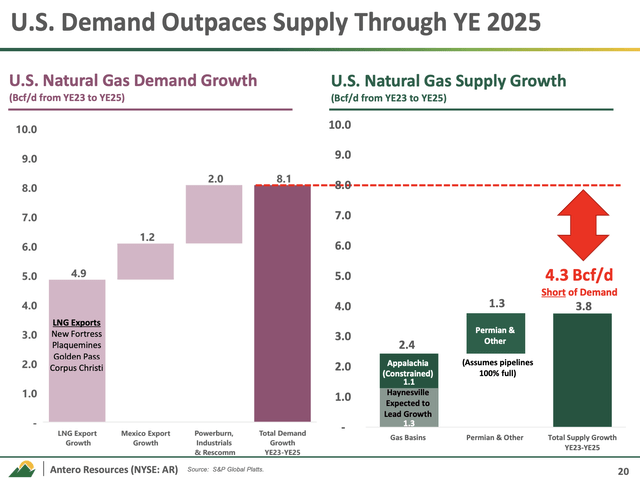

It is also very bullish on natural gas, expecting a supply/demand gap of more than 4 billion cubic feet per day until 2025. This aligns with the thesis I discussed in the first part of this article.

Antero Resources

So, what about its valuation?

Valuation

Putting a valuation on a company that is highly dependent on commodity prices is tricky. After all, the bull case mainly depends on the price of natural gas and natural gas liquids.

As I’m bullish on these prices, I’m bullish on AR as well.

However, to add some numbers, even in this environment, analysts expect AR to boost free cash flow to $1.1 billion next year. That would be 12.6% of its current market cap.

As I wrote in my prior article, this gives the company room to aggressively buy back stock – especially if natural gas prices normalize. The company aims to spend roughly half of its free cash flow on buybacks while continuing to reduce debt.

If my bull case is correct and natural gas prices rise to more than $5-$6 Henry Hub in the years ahead, I believe AR has the potential to generate a free cash flow yield of more than 20%.

Moreover, while AR is currently unable to outperform the energy ETF (XLE), that’s mainly due to poor natural gas prices and the absence of any hedges. On a long-term basis, I expect AR to outperform its peers by a wide margin.

The only problem is its volatility. AR is not the right stock for conservative investors. Conservative investors are better off buying oil and gas giants with less volatility.

I sold AR when I switched brokers earlier this year and invested most of my money in oil and gas royalty stocks. However, I am planning to buy back in, as I absolutely love the value this driller brings to the table.

I also own Antero Midstream (AM), the company that owns Antero Resources’ midstream assets.

Takeaway

Despite recent setbacks, my confidence in Antero Resources remains strong – very strong.

The natural gas market may be volatile, but Antero’s low breakeven costs, deep reserves, and healthy balance sheet make it a standout player in its industry.

While the stock isn’t for the faint-hearted, it offers significant upside potential, especially as natural gas demand continues to rise and production levels stabilize.

I’m planning to reinvest in AR, as I believe its long-term opportunities far outweigh the current challenges.

If you’re bullish on natural gas, Antero Resources deserves a spot on your radar.

Pros & Cons

Pros:

- Low Breakeven Costs: Antero Resources has industry-leading production costs, making it resilient in a volatile natural gas market.

- Deep Reserves: With over 20 years of premium inventory, AR is well-protected against declining reserve levels in the industry.

- Strong Balance Sheet: Investment-grade credit rating, low leverage, and substantial liquidity provide AR with financial stability.

- High Upside Potential: No hedges mean greater exposure to rising natural gas prices, which could lead to significant gains.

Cons:

- High Volatility: AR is extremely sensitive to natural gas price fluctuations, making it unsuitable for conservative investors.

- Short-Term Weakness: Recent price declines have hurt its performance, and the stock may struggle if gas prices remain low.

- No Hedging: While it offers an upside, the lack of hedges can lead to a significant downside if gas prices drop further. However, because producers are already cutting output due to low prices, I doubt prices have much more room to fall.

Read the full article here