Snowball Effect Just Getting Started

When I wrote my bullish Delcath (NASDAQ:DCTH) article in November 2023 there was a lot of investor angst heading into the HEPZATO KIT launch in Q1 2024. It had received FDA approval in August 2023, but until sales start coming in, medical device stocks can move rapidly in either direction. Medical device stock volatility is the highest prior to approvals. Following approvals, it declines but is still elevated. The next step for volatility to fall is initial sales. The final hurdle is getting to profitability.

I believe some funds sold the stock following the positive catalyst to cash out in what was a very bad medical device trading environment in the late summer/early fall of 2023. Regardless of what caused the stock to fall, investor stress was high due to the extensive training process required to administer HEPZATO KIT. I will refer to HEPZATO KIT as PHP (Percutaneous Hepatic Perfusion) in rest of this article. This isn’t a drug that gets high sales almost immediately upon approval. It’s a device drug combination therapy that requires a team of doctors including an interventional radiologist, perfusionist, and anesthesiologist to watch a procedure (preceptorship) and do one under the watchful eye of experienced users of the technology (proctorship). Then the hospital formulary and value analysis committees need to review PHP before it be used.

At the start of the US launch, experienced PHP users needed to fly in from Europe to train doctors. It was going to take two to three quarters to really get going where the snowball effect would make it easier to train doctors (more doctors available to give training) and streamline the reimbursement process.

That reimbursement process was given a nice boost when CMS (Center for Medicare and Medicaid Services) gave PHP a permanent J-Code which went into effect on April 1. This pass-through payment status simplified the process for insurers and hospitals. Hospitals get paid 6% plus the $182,500 cost of PHP (the $182,500 flows to Delcath). Private insurers copy this payment structure because metastatic uveal melanoma (mUM) is an ultra-orphan indication.

HEPZATO KIT REMS website

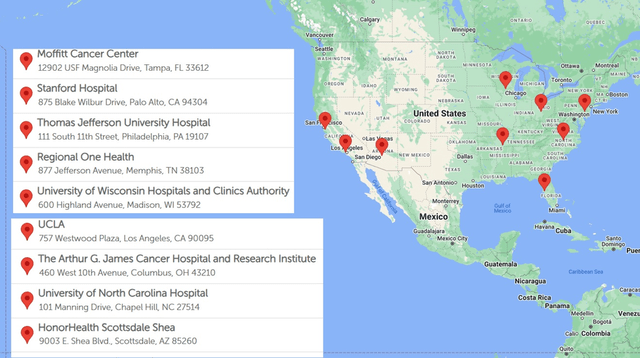

Delcath is now through the hard part of the launch. As you can see on the map above, the firm now has nine treatment centers currently doing this procedure. It should have 10 treatment centers by the end of August. This makes it much easier to schedule the required preceptorships and proctorships to open new centers. The subsequent launches will have a streamlined formulary process. New launches will go smoother since doctors will have more colleagues to lean on when discussing how the first few procedures went. Therefore, the snowball effect I described in my November article is just getting started in Q3 2024.

Stock Volatility Too High: A Look At Treatment Center Rollout

There was stock volatility to the upside and downside following the Q1 & Q2 reports, but not much about the launch has changed in the past two reports. As you can see from the chart below, next year analyst sales estimates haven’t moved much in reaction to either report. Specifically, Q1 was deemed a good report because Gerard Michel, Delcath’s CEO, raised guidance from 15 treatment centers doing procedures at year end, to 20. Furthermore, the firm expected 10 centers by Q2 and 15 by Q3.

Since then, we’ve seen launches go slower than expected due to modest delays in hospital formulary committees’ acceptance of the device (which has caused the stock to correct). Formulary committees at hospitals evaluate which medications will be used. They decide which drugs will be on hospital formularies (list of drugs used at the hospital), create a drug use program, and set rules for the usage of expensive medications.

The nice part for investors is the Risk Evaluation and Mitigation Strategy (“REMS”) website tells us exactly how many hospitals are doing procedures. We knew headed into the Q2 report launches had been going slightly slower than expected. It was great to hear there wasn’t a major reason for the slowness. It’s just formulary committees taking a few weeks longer than expected. This has no impact on the long-term thesis. Furthermore, in addition to the 10 treatment centers by the end of August, there are four more centers in the process of scheduling proctorships which means they will be active centers in the next few months (management says by September).

Management stated there are eight more hospitals on the preceptorship step. However, they also said over 20 centers total have done a preceptorship which implies seven out of these eight hospitals have already done a preceptorship. That’s because over 20 means at least 21; if you add up the 10 doing procedures as of the end of August with the four about to start in the next few months and the eight I just mentioned, you get 22.

HEPZATO KIT website

Regardless of which exact step this set of eight centers is on, this implies there will be about 22 centers doing procedures at the end of Q1. The map on the HEPZATO KIT website which shows the centers accepting patients has 17 hospitals listed. There are more hospitals on this map than the REMS one because hospitals start accepting patients a few weeks before the procedures start due to the time it takes to get the patient set up. An analogy would be leaving for the store 30 minutes before it opens because you know there will be a 30–45-minute commute.

Prior to the Q2 report, management suggested there would be 25 to 35 treatment centers in America at maturation. On the Q2 call, management raised that guidance to 35-40 hospitals. This means there will still be significant work to do after Q1 2025 when only slightly over half of that will be active. This doesn’t mean there are suddenly more patients with mUM. It means there is a lot of doctor/hospital interest in PHP. Having more centers will decrease patient travel time. By the end of 2025, the vast majority of these locations will be active.

Q2 Weak Point Analyzed: Treatments Per Center

Even though the average number of procedures in Q2 was ahead of estimates, I’d argue this topic was one of the more negative aspects of the report although it’s not a long-term problem either. On the Q1 call, management projected a linear increase in procedures per hospital per month. They projected 1.5 treatments per month by mid-year and two per month by year end. In Q2, the average was almost two per month which was way above guidance for 1 to 1.5. That occurred because the high-volume early launch sites were a larger percentage of overall sites since fewer were launched than expected. The firm projected 10 sites by the end of Q2, but only had seven.

The three FOCUS trial sites that helped get PHP approved didn’t need training to get going and were experienced with the procedure. This means they were already operating near maturity which is ~four treatments per month. The two biggest volume sites are Thomas Jefferson University and Moffitt Cancer Center. They can do four to six treatments per month. On the Q1 call, management said Moffitt can do over 40 procedures per year. The newer hospitals might do one per month. In a May tweet, Dr. Jonathan Zager at Moffitt said the center is doing 4-6 procedures per month. Besides the biggest two centers, a third center is becoming a high-volume site. One hospital recently did three procedures in one day. It was likely one of these three high volume sites.

The average number of treatments per month for each center is expected to fall to 1.5-2 by year end as the new centers which are taking time to get to maturity are added to the calculation. This average is lower than the two projected in Q1 because hospitals are doing an initial group of procedures and then pausing 1-2 months to see how patients react and evaluate the explanation of benefits from payers. This is a new negative which wasn’t known prior to the report. However, it’s normal to do this with a new procedure. I don’t think the next batch of new hospitals are going to have pauses like the first batch because they will lean on the experience of the first group. Even if this pause continues, it won’t be a factor once the vast majority of hospitals are launched by year end 2025.

Next year, there will be a big shift from focusing on training new centers to increasing volumes per hospital. There is great uncertainty what the final average of treatments per month will be at maturation, but I’m going with a base case of four treatments per month for 40 hospitals. Delcath is working on building out the referral network necessary to get new hospitals to increase their output from one per month towards three in 2025. There will be a continuum of treatments per month, with Moffitt and Thomas Jefferson remaining the highest volume sites. When management guided for 25-35 centers, they said they didn’t want low volume sites doing one treatment per month unless the site was used for trials. By extending the footprint to 40, it shows Delcath sees enough demand at these incremental sites to do at least two per month.

Europe Growing Adoption, But Only Breaking Even For Now

Delcath beat sales estimates in Q1 mostly due to its growth from CHEMOSAT in Europe which almost all came from Germany. Remember, CHEMOSAT is PHP with the melphalan sold separately. Europe had $1.1 million in sales which was up from $600k in Q1 2023. Sales were mostly from Germany because that’s the only EU country where PHP has consistent reimbursement and where Delcath’s only European sales rep was located. While Germany is reimbursing PHP, it’s only at about $20,000 per procedure which is leading Delcath to manage Europe on a near breakeven basis in the short to medium term with most of the focus being on generating data from case studies/trials. This means sales from countries that offer reimbursement will pay for the cost of these case studies and small trials (free procedures).

As of Q1, management said Germany had about 15% penetration. In Q2, PHP had $1.2 million of sales in Europe, so penetration is likely in the mid to high teens. Delcath has recently hired a sales rep to go after the UK market. The first goal is to get reimbursement (currently patients can only get the procedure in the UK through private payors or self-pay). Management expects to get reimbursement next year, but it doesn’t expect a significantly higher rate than it’s getting in Germany. Germany’s population is about 22% larger than the UK and has similar incidence levels per capita.

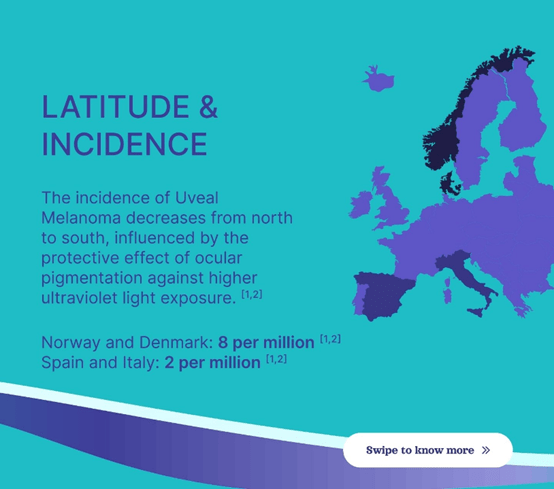

As you can see from the map below, northern Europe has the highest incidence rate of uveal melanoma and southern Europe has the lowest rate. People with lighter eyes and skin pigmentation are more likely to get this disease which metastasizes about 50% of the time (over 90% liver dominant). Norway and Denmark will be critical areas to go after since they have eight cases per million. Italy and Spain only have two cases per million, but obviously they have large populations, so they are still useful to go after. Delcath is early in its commercialization process in France, Italy, and Spain. It wants to have multiple centers in all the countries I’ve mentioned. PHP is currently being done in over 22 centers in Europe. The two most prominent areas are Germany and the UK. There are some centers in Italy, Netherlands, Turkey, and Sweden.

Delcath EMEA LinkedIn

I never expected Europe to reimburse PHP at the same rate as the US, but I expect a higher rate (than ~$20,000) eventually once data comes out from the CHOPIN combination study which I will discuss in the next section. If the data shows evidence of a very large progression free survival improvement, I expect better reimbursement rates. PHP is so well received in America, HEPZATO KIT was awarded the New Technology Add-on Payment (“NTAP”) designation. This will only help hospital costs in the rare instance where the procedure is done inpatient. However, there is a high bar to achieve this designation which shows how much CMS values this procedure. Europe should also highly value it in time. However, I won’t project any payment improvement in 2024 or 2025. Early CHOPIN data will be presented in 2H 2025. CHOPIN is an Investigator Initiated Trial (“IIT”) in the Netherlands. Delcath management estimates 40% of the country’s patient population is in this study, meaning they are already getting treatment (for free).

2021 Delcath Investor Presentation

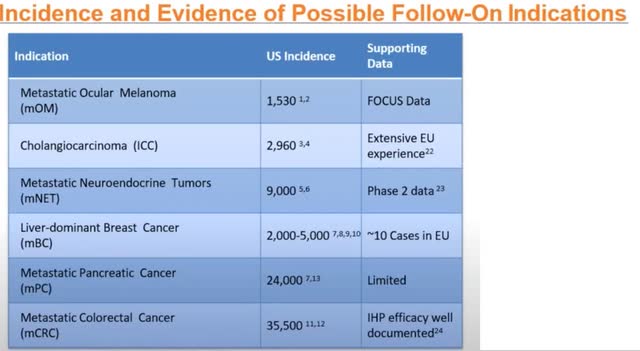

Europe is especially important to expanding PHP into treating other solid tumor types since patients have already been treated there with indications outside of mUM. This data, shown in the table above, is a key factor in my thesis that PHP is a platform technology. Europe has extensive experience treating Intrahepatic Cholangiocarcinoma (“ICC”) with PHP in combination with immune checkpoint inhibitors (“ICIs”). There is positive phase 2 data on Metastatic neuroendocrine tumors (mNET) being treated with PHP. In the phase 2 study of 24 mNET patients, 10 had a partial response, six had stable disease, and three had progressive disease (five not available). The chart below shows those two indications are much larger than mUM, which is the smallest one.

Delcath Investor Presentation Deck

CHOPIN Update Coming 2H 2025

The CHOPIN study is a phase 2 randomized trial collecting data on the use of a combination therapy that includes PHP as a first line treatment for mUM. It had enrolled 70 patients as of the August call. The goal is to get to 76 enrollees which will likely occur by year end. The CHOPIN study looks at combination therapy with PHP and Ipilimumab + Nivolumab (OPDIVO + YERVOY) which is a Bristol-Myers Squibb (BMY) combination drug. It is an immunotherapy administered intravenously. This combination drug is an immune checkpoint inhibitor. ICIs work by blocking proteins that stop the immune system from working properly and attacking the cancer cells. PHP working well with Ipi/Nivo makes PHP more valuable to Bristol-Myers Squibb. Furthermore, it makes PHP more likely to be used as a first line treatment for mUM.

At the time of the most recent cutoff date, all seven patients in the phase 1b portion of the study were still alive. Three of four patients who experienced progressive disease continued treatment with repeated PHP cycles. The CHOPIN study includes four uses of PHP. Since PHP is administered up to six times, it makes sense patients are getting more PHP treatments after the study. The primary objective of the study is to measure progression free survival after one year.

The fact the primary endpoint is going to be mid-2025 when we had expected a presentation of the findings in the spring might be good news because delays can be caused by patients living longer. The initial findings of this study will be presented in 2H 2025. The goal of the phase 2 study is to increase progression free survival at one year from 20% in the PHP only arm to 50% in the combination arm. Considering that the CHOPIN data can make PHP a first line therapy for mUM and can increase reimbursement rates in Europe, this presentation is a major catalyst for Delcath stock in 2H 2025.

Delcath announced on the Q2 call that it is doing another IIT sponsored study with the same combination approach. Enrollment in Sweden started in Q3. Delcath wouldn’t be doing another study if the CHOPIN study was going poorly. PHP will be the control arm. Management has heard multiple anecdotal reports of doctors using Ipi/Nivo combined with PHP prior to the results of the CHOPIN study being published. Doctors wouldn’t be doing this if they heard the CHOPIN study wasn’t going well. This all lines up for Delcath stock to have a major catalyst likely next fall when the initial data is made public.

New Indications: ICC & mCRC

As I mentioned in my last article, Delcath is looking for PHP to be used to treat ICC via an addition to National Comprehensive Cancer Network (“NCCN”) guidelines in which PHP will be used off its FDA label. Delcath won’t be able to market this usage. The company might get on NCCN guidelines with existing publications or a small trial. It aims to get reimbursement via the peer reviewed publications, case studies, and single arm basket trials it gathers from European sites. I expect the plan for the ICC indication will be presented on an earnings call once more centers launch in Europe. We should get clarity in 1H 2025.

On the Q2 call, Gerard stated,

“The goal will be ranging from giving adequate data, so physicians can make an informed judgment for certain patients whether or not they want to treat and try to get reimbursed for the patients, to informing potential guidelines [emphasis added] down the road, all the way to trying to expand the label.”

It’s not unrealistic to expect the ICC indication to start generating sales as early as 2026. Let’s see what plans management lays out in the next few quarters. This is an important catalyst to unlocking the valuation given to platform cancer therapies. Platforms get a higher multiple because they have greater sales potential and diversified revenue streams.

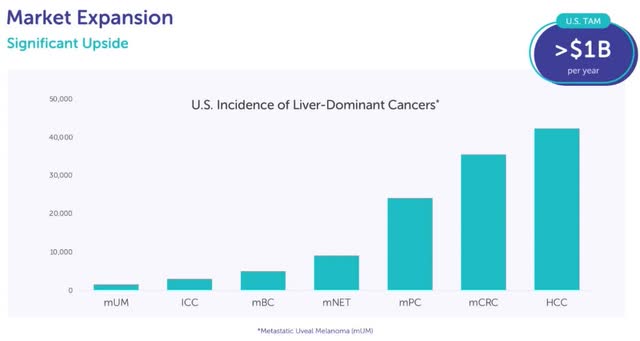

Delcath plans to start a phase 3 trial on an additional indication next year. This choice will likely be announced on the Q3 call. It will probably start enrollment in the spring following Delcath receiving the $25 million it gets 21 days after achieving $10 million in US sales in a quarter. This will be a small trial with somewhere around 200 patients (making it cheaper than most trials) because it is for an orphan indication. The chart earlier in the article shows metastatic colorectal cancer (mCRC) is the second-most prominent indication, but the 40,000 incidences in America is still well below the threshold of being an orphan indication (below 200,000).

Phase 3 trials usually take up to four years, meaning we should see sales in 2027 or 2028 if it goes well. Trial enrollment will easier than mUM since mCRC has a much higher incidence rate. Plus, PHP is FDA approved and working in the real world for mUM patients.

As you can tell, I think mCRC is the most likely indication Delcath will go after. On the call, management said it conducted two scientific advisory boards focused on colorectal and breast cancer. I think the choice should be mCRC because it is a much larger indication and there’s more evidence PHP is an effective treatment. Just like with mUM, mCRC has been successfully treated with Intrahepatic Perfusion (“IHP”). IHP is the invasive version of PHP which had a high correlation of efficacy in the mUM indication. PHP is basically a less risky version of IHP that can be repeated.

There have been multiple clinical studies done with IHP on mCRC in combination with immune checkpoint inhibitors. The Van Iersel data includes 154 patients with an objective response rate (ORR) of 50%, median progression free survival of 7.4 months, and median overall survival (mOS) of 24.8 months. The data from Alexander which includes 120 patients showed a 61% ORR, mOS of 17.4 months, and a two-year survival rate of 34%. The patients in these studies were heavily pre-treated meaning they were very far along with the disease. This lowers the response rate making these results even more impressive.

There have been ~10 documented cases on PHP being used in the treatment of liver dominant metastatic breast cancer (mBC) with good results. Breast cancer is a large cancer type with a small percentage of patients with liver dominant metastatic cancer. Specifically, 726,259 women are diagnosed with breast cancer annually in the US, EU, and UK combined. 18% of women with breast cancer have distant metastatic disease and 5% of this subset have liver only metastasis.

Delcath’s investor presentation has a slide dedicated to mCRC, but doesn’t have one for mBC. Furthermore, in a 2021 investor presentation Gerard said mCRC was the indication they are likely to go after next. Regardless of which solid tumor type is picked, this should be a major catalyst for Delcath stock in the medium term. It’s human nature to focus on what’s immediately ahead of us since Delcath is just getting started with the rollout for mUM, but it’s not a good idea for investors to wait until Delcath gets to peak sales in this indication before looking for the next growth driver. We must think ahead of the market which is already somewhat forward looking. I think when Delcath hits profitability and starts the mCRC trial in the spring, investors will start to price the stock as a platform company which could lead to a higher multiple on long-term projected sales.

Competitive Landscape: KIMMTRAK

Many patients will get treated with KIMMTRAK and PHP since neither are a cure for mUM. However, there is some competition to see which will be the first line of treatment for HLA positive patients (PHP treats both HLA positive & HLA negative patients). Besides looking at the competitive landscape, KIMMTRAK is useful to analyze because its sales help us project PHP’s sales in the next couple years since KIMMTRAK has had a two-year head start. In Q2 2024, KIMMTRAK had $75.3 million in sales which mostly came from the US. This was up 32% from the prior year.

Breaking sales down by region, KIMMTRAK did $55.6 million in sales in the US (35.4% growth), $15.4 million in Europe (1.1% growth), and $4.3 million internationally (553.2% growth). Immunocore (IMCR) believes it has 65% market share in the US which means its annualized addressable market is $342 million. This makes PHP’s addressable market about $760 million since 45% of mUM patients are HLA positive and all can be treated by PHP.

Immunocore expects continued growth for KIMMTRAK throughout the year implying it can get to at least 70% market share in the US. KIMMTRAK was approved in January 2022, so we are currently 2.5 years post approval. KIMMTRAK is easier to administer which gave it a quicker start than PHP. If Delcath’s 40 US centers do an average of four treatments per month, that’s $350 million in sales which is about 46% market share. That’s a fine goal for 2.5 years post approval (mid-2026) because PHP is off to a slower start since hospitals need to schedule training. Peak mUM sales might be as high as 70% market share which is $532 million.

PHP hitting 70% peak market share requires it to have significant first line usage. When thinking about the first line competitive landscape of mUM, I refer to Dr. Zagar at Moffitt Cancer Center. He said,

“We should convince the community to use this treatment in first line, as there is data to support treating patients with low burden of disease and as first line will give them best chances at a response… if we don’t use PHP early in the treatment there could be a chance the patient becomes ineligible for PHP due to progression in the liver or progression to numerous sites outside the liver that cannot be treated between PHPs.”

Once over 50% of the liver has cancer, PHP can’t be used, so it should be used before KIMMTRAK. The CHOPIN data will encourage doctors to use it as a first line treatment if the 1-year progression free survival rate hits the 50% target.

KIMMTRAK management stated on the Q2 call the current reimbursement environment in Europe is terrible (tough time for CHEMOSAT to go after reimbursement following FOCUS trial). Specifically, the firm’s head of commercial said this is one of the toughest reimbursement environments he’s seen (over 20 years of experience). That’s evidenced by Europe’s anemic 1.1% growth rate in Q2. Even still, it’s not horrible to see Europe at $61.6 million annualized sales since Delcath is currently only at $4.8 million. There’s room for growth even without CHOPIN data driving a higher reimbursement rate.

Immunocore is seeking a label expansion for KIMMTRAK in late-line cutaneous melanoma and adjuvant uveal melanoma. Adjuvant is additional treatment after the primary treatment to lower the chance of cancer reoccurring. Remember, KIMMTRAK is currently approved for metastatic uveal melanoma which is different from uveal melanoma.

Competitive Landscape: Darovasertib + Crizotinib

IDEAYA Biosciences (IDYA) is in clinical testing of the combination drug Darovasertib + Crizotinib which is a more serious threat to Delcath than KIMMTRAK. IDEAYA Biosciences is undergoing three clinical trials for their combination therapy. There was a recent update in June from their uveal melanoma treatment which showed nine of 12 patients had their eye preserved; eight of them showed over 30% tumor shrinkage in the eye after six months (median 47% shrinkage). This study doesn’t impact Delcath because uveal melanoma can metastasize to the liver even after treatment.

There is also a phase 1/2 study which looks at patients with solid tumors with GNAQ or GNA11 mutations including mUM and cutaneous melanoma. This study has a primary completion date of October 2024, so I will be looking out for the results. Obviously, it being in phase 2 signals we are still pretty far away from anything major being approved. The early readouts only showed results for successful tumor shrinkage of cutaneous melanoma patients (not mUM).

The most important clinical trial is the one for Darovasertib + Crizotinib being used as a first line treatment for mUM. The phase 2/3 primary completion date is January 15, 2027. By then, PHP should be showing strong results in combination with immune checkpoint inhibitors. Plus, it’s possible by the late 2020s, mUM isn’t an important percentage of Delcath’s revenues given it’s the smallest indication for PHP. It’s also notable that more data might be needed for Darovasertib + Crizotinib to get approved because this is only a ‘potentially’ registrational trial. The phase 2/3 trial is only enrolling HLA negative patients probably because KIMMTRAK treats HLA positive patients. However, the company is looking to expand the clinical application to HLA positive patients in the future.

The Darovasertib + Crizotinib combination therapy has shown strong early results. The phase 2 data that came out in October 2023 included 68 mUM patients. The ORR in HLA positive patients was 60% and 42% in HLA negative patients. Both of these were first line treatments. The median progression free survival rate was 7.1 months in first line mUM treatments. It was 11 months in hepatic only mUM patients which is the subset Delcath is going after. The median progression free survival rate in the PHP FOCUS trial was nine months. In the FOCUS trial, PHP was used as a second line or later therapy. I believe PHP will show better results when it is used earlier in the real world than it was in the FOCUS trial as I highlighted in my last article.

Intermediate Term Sales Projection

In Q2, Delcath reported $1.2 million in CHEMOSAT sales and $6.6 million in HEPZATO KIT sales. CHEMOSAT sales should grow gradually as Germany gains penetration. There will be a step up in growth when the UK grants it reimbursement. In this section, I’ll assume no significantly larger reimbursement rate is given in Europe. Based on similar growth in Germany, CHEMOSAT can do $1.3 million and $1.4 million in sales in Q3 and Q4. If the UK starts generating sales in Q2 2025, we could see the following sales from Europe each quarter next year: $1.5 million $2 million, $2.2 million, $2.4 million. That’s a total of $8.1 million. This will pay for the free treatments in Netherlands and Sweden that are a part of studies.

Let’s now look at HEPZATO KIT. In July, there were eight centers doing about 1.9 procedures per month. In August there will be 10 centers doing about 1.75 treatments per month. In September, there could be 14 centers doing 1.5 treatments per month. That gets me to $9.8 million in Q3 sales. Based on this, I’ll say there’s probably a 30% shot Delcath gets to the $10 million mark in US sales. Even if Delcath is one procedure away from hitting the milestone, they can’t move a procedure from October into September since each procedure is being done as fast as possible already. The $10 million mark will give the company $25 million in cash from the warrants. The stock would spike on achieving this milestone a quarter earlier than guidance. I project Delcath will have $11.1 million in total sales in Q3 which would beat estimates for $9.6 million.

I forecast Delcath will end the year with 18 centers and average 16 centers in Q4; it will end Q1 with 22 centers and average 20. I believe centers will do 1.4 treatments per month in Q4 (new hospitals diluting results) and 1.65 treatments per month in Q1. That gets me to $12.3 million US sales in Q4 and $13.7 million total. That’s above estimates for $12.3 million. I don’t think the consensus is that far off in 2024, but it gets further off the more we push into the future. My Q1 calculation is $18 million in US sales and $19.5 million globally.

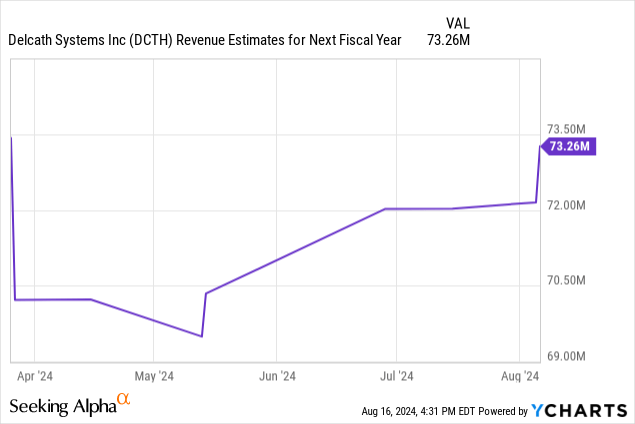

Now let’s quickly run through the next three quarters. I expect the average number of centers in the next three quarters to increase to 24, 28, and 32. The average treatments per month will increase to 2, 2.5, and 3. That gives us US sales of $26.3 million, $38.3 million, and $52.6 million. That brings us to total global full year 2025 sales of $143.3 million which is almost double the consensus for $73.3 million.

Medium Term Stock Price Target $73

Delcath is doubly undervalued because mUM indication sales estimates are too low and the market is ignoring the potential for PHP to be a platform device which treats multiple solid tumor types. If Delcath gets to $350 million in annualized run rate US sales by mid-2026, I think the market cap should be at least $3.5 billion to price in the potential from ICC and mCRC along with further growth from mUM (getting to 70% market share). There are currently 44.4 million fully diluted shares outstanding. With 48 million shares outstanding by mid-2026, a $3.5 billion market cap gives us a ~$73 share price.

I believe that’s conservative because $350 million in sales is only 46% market share of mUM, ICC should be very close to generating sales by mid-2026, the mCRC phase 3 trial could show early positive readings in 2026, and that’s not counting a higher reimbursement rate in Europe. I’m not including sales from Europe at all in this valuation. If it’s still being run at breakeven, it doesn’t deserve a sales multiple above 1. Since I’m only speculating it will get a higher reimbursement rate after the CHOPIN data is published, I’ll position this as potential upside not included in my base case. In my last article, I mentioned Europe has a 45% larger patient population than America. Assuming Europe’s reimbursement rate would get to 70% of America’s might have been too bullish with Germany initially paying only slightly more than 10% of America’s rate.

The current stock price is $7.5. The stock catalysts in the next two years are the following: 2025 sales results/guidance causing estimates to increase, the CHOPIN data being published in Q3 2025, European reimbursement rates increasing following the CHOPIN data coming out, ICC being added to NCCN guidelines/sales being generated from off label usage, management announcing the indication it is going after with phase 3 trial, and initial data points from the phase 3 trial.

Cash Position Analysis: Breakeven Projection & Clinical Trial Cost

Delcath raised $7 million by issuing shares in Q1 to help pay off its debt and lower the risk it wouldn’t get to cashflow breakeven. The small offering was entirely supported by management and existing investors. There were insider buys at $3.72 in March 2024 from the GM of Interventional Oncology, General Counsel, Chief Medical Officer, CEO, SVP of Finance, and 2 Directors. As I will illustrate, the raise wasn’t needed. It’s only 1.8 million shares which isn’t going to make or break the investment. Clearly, insiders wanted a chance to buy the stock at the launch of HEPZATO KIT. It’s better than just giving them free shares.

Delcath ended Q2 with $19.9 million in cash. They finished paying off their loan on August 1. They had two $1 million monthly payments in Q3. I project the company will burn about $2 million from operations in Q3 which is down from $4.5 million in Q2 due to higher sales from HEPZATO KIT which will have +80% gross margins. Therefore, the firm will end Q3 with about $15.9 million in cash. I expect the firm to reach free cash flow breakeven in Q4 since it will have $13.7 million in sales and management said the breakeven threshold is $13 million (guidance is to reach breakeven in Q1).

The firm will get $25 million in cash from the warrants early in the spring when the business is already free cash flow positive. This money will be used to fund the mCRC phase 3 trial. I am projecting this trial will have 200 patients and cost $42k per patient (median for a phase 3 trial). If that projection works out, the $25 million from the warrants is more than enough to cover this $8.4 million expense. If the trial costs more per patient, the firm can use profits from the mUM indication to fund it. The trial isn’t entirely an upfront expense. Therefore, profits in 2025 will be more than enough to pay for it even if it costs over $25 million.

Short & Long Term Risks

Delcath’s PHP technology only launched commercially in America this January. Even though over 30 hospitals have shown interest in adopting PHP, there is still risk the rollout doesn’t go smoothly. Value analysis committees and formulary bodies which control reimbursement can delay adoption.

Furthermore, the procedure involves three doctors who each need training. If this complex procedure isn’t done correctly and the REMS isn’t followed properly, there could be harm to the patient. Any news of harm to patients could slow or halt adoption. Delcath is at a very critical portion of its lifecycle in which it is about to turn profitable and reach $10 million in US sales which will get it access to $25 million. Therefore, any major adoption issues would be particularly harmful in the next three to six months. Taking longer to reach profitability and $10 million in US sales could cause the company to issue shares at low valuations like it has done in the past.

Delcath faces reimbursement risk which is the most obvious in Europe because of the low rate given in Germany and the tough environment. There also is risk in America; CMS could lower the rate in the next few years due to budget constraints. The aging of the American population is catalyzing increased spending on healthcare. However, decisions need to be made to avoid exploding budget deficits. PHP is a very new technology, but in the future politicians might go after its high cost like they are going after current expensive drug pricing.

The average number of monthly treatments per center in the intermediate term and at maturity is highly uncertain. If the average only rises to three per month and increases at a slower pace than I expect, the stock won’t rise as much as I projected. Specifically, three treatments per month at 40 centers would bring in $263 million in US sales rather than the $350 million I projected. Lower treatments per center would occur if PHP isn’t used as a first line treatment. Dr. Jonathan Zagar is one of the biggest proponents of PHP. His assessment that PHP should be used as a first line treatment might not become the consensus if real world success isn’t as high as it has been at the three FOCUS trial hospitals.

I expect the CHOPIN trial will show improved one-year progression free survival. However, I can’t be sure the results will meet expectations. If results are better than the control arm, but disappoint some doctors, it might limit PHP’s expansion into becoming a first line therapy and receiving better reimbursement rates in Europe.

Delcath faces future competition from IDEAYA Biosciences. It’s possible that using KIMMTRAK and HEPZATO KIT leads to improved results for patients. However, we have no evidence of how Darovasertib + Crizotinib will impact the treatment landscape. Maybe the phase 2/3 trial will show such good results that it gets approved in early 2027 and causes PHP to be phased out as a treatment for mUM.

The evidence for the use of PHP in patients with ICC is strong. However, it’s not as robust in other indications. That’s why Delcath is trying to do a phase 3 trial for either mCRC or mBC. The phase 3 trial might take longer to show results than I expect. Furthermore, it might not be as successful as investors hope.

Delcath won’t get a high multiple on maturing mUM sales if it can’t expand the NCCN guidelines to include ICC and generate reimbursement for that indication. The success of the phase 3 trial on a future larger indication also will impact the multiple. If it’s unsuccessful, the sales multiple will stay suppressed or decline if optimism is high prior to results being publicized.

Finally, Delcath could get acquired by Boston Scientific (BSX) which makes Y90 (competing product with much worse results than PHP) or (BMY). While that sounds like a positive, an acquisition in the near term would limit shareholders from profiting off the full potential upside Delcath could bring if PHP ends up being widely used to treat all potential indications in the long term.

Read the full article here