Note:

I have covered Borr Drilling Limited (NYSE:BORR) previously, so investors should view this as an update to my earlier articles on the company.

Last week, leading offshore driller Borr Drilling reported Q2/2024 results. Adjusted for a number of one-time items, revenues and profitability came in largely in line with expectations.

Company Press Releases / Regulatory Filings

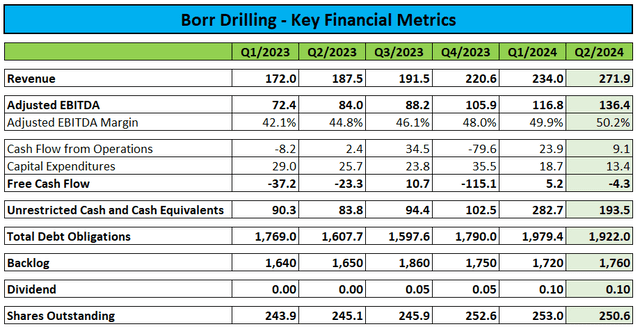

While Adjusted EBITDA of $136.4 million and Adjusted EBITDA margin of 50.2% reached new all-time highs, cash generation was impacted by $91.9 million in semi-annually interest payments.

The company finished the quarter with $193.5 million in unrestricted cash and cash equivalents and $1.92 billion in debt. Total liquidity amounted to $343.5 million.

Subsequent to quarter end, Borr Drilling issued an additional $150 million of 2028 10% senior secured notes:

The proceeds from the offering are intended to be used for the acquisition and activation costs for the newbuild rig “Vali”, instead of the previously secured yard financing that was intended for the newbuild, as the terms and pricing for the Additional Notes are more advantageous, and for general corporate purposes including debt service.

The company took delivery of the “Vali” last week, with the rig likely being assigned to a previously announced contract offshore Africa.

Please note that the company expects to take delivery of its last remaining newbuild rig “Var” in Q4/2024. While there’s committed shipyard financing in place, Borr Drilling might very well consider issuing additional senior notes in order to avoid potentially restrictive covenants.

Backlog of $1.76 billion was up slightly, both on a sequential basis and year-over-year.

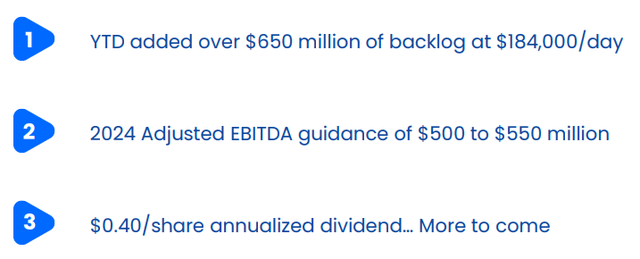

So far this year, the company has secured $651 million in gross backlog additions at an average dayrate of $184,000 with $250 million alone contributed by a surprise four-year contract for the rig Arabia 1 with Petrobras (PBR) in Brazil. Should Petrobras exercise its option for an additional four years, the rig would remain employed in Brazil until 2033.

Please note that the dayrate for this new contract will be substantially above the rate received from Saudi Aramco until the rig’s suspension earlier this year.

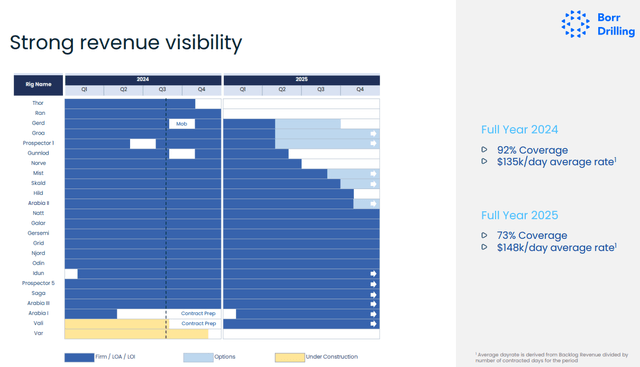

Contract coverage for 2024 and 2025 has increased to 92% and 73% respectively, with the average dayrate for 2025 currently up by 10% over 2024:

Company Presentation

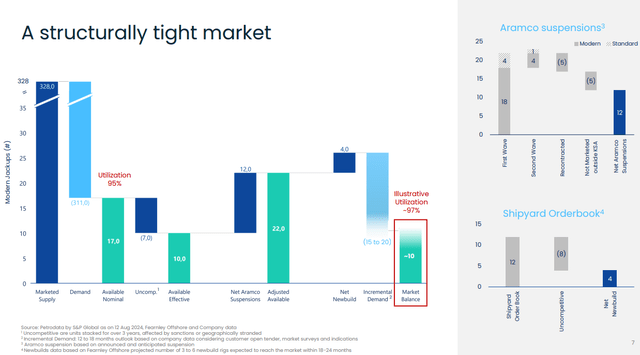

On the conference call, management remained optimistic on the prospects of the jackup market as recent contract suspensions by Saudi Aramco (ARMCO) are expected to be offset by incremental demand in other regions:

Company Presentation

Borr Drilling also declared a quarterly dividend of $0.10, unchanged from Q1/2024 which is expected to be paid on September 6. On the call, management hinted to further increases next year:

Looking at 2025 with reduced CapEx outlay and incremental day rates for the already committed contracts, then there is plenty of potential to significantly increase returns to shareholders going forward.

During the questions-and-answers session, management outlined expectations for cash generation to increase by over $200 million next year.

Lastly, Borr Drilling reiterated full-year guidance for Adjusted EBITDA of $500 million to $550 million:

Company Presentation

With the company apparently executing well on the contracting front and the only rig suspended by Saudi Aramco scheduled to commence a new multi-year contract at a much higher rate in early 2025, I no longer expect the situation in Saudi Arabia to materially impact the company’s financial results.

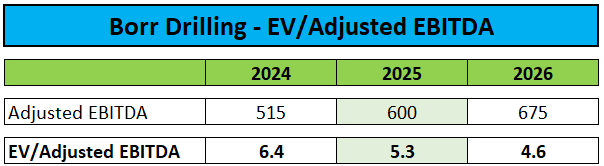

Consequently, I have increased my Adjusted EBITDA estimates for both 2025 and 2026:

Author’s Estimates

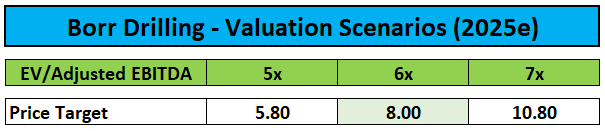

As a result, my price target for the shares moves up from $7 to $8 based on an assigned valuation of 6x estimated 2025 Adjusted EBITDA:

Author’s Estimates

At prevailing prices, the company’s shares are offering a 6.4% dividend yield. With Borr Drilling remaining committed to increased shareholder capital returns, I wouldn’t be surprised to see the quarterly dividend being lifted to $0.15 in early 2025.

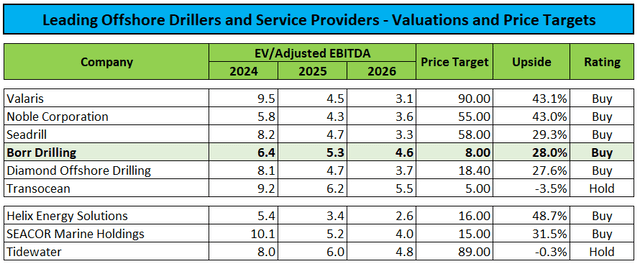

Considering almost 30% upside from current share price levels, I am upgrading the company’s shares from “Hold” to “Buy“.

Author’s Estimates

Bottom Line

Adjusted for a number of one-time items, Borr Drilling reported Q2/2024 largely in line with expectations and reiterated full-year guidance.

The company continues to do well on the contracting front, with a new $250 million multi-year contract offshore Brazil being the highlight for the quarter.

With strong visibility for the remainder of the year and decent contract coverage for 2025, I have raised my Adjusted EBITDA estimates for 2025 and 2026 and increased my price target from $7 to $8.

Considering almost 30% upside from current levels, a juicy 6.4% dividend yield and the company’s strong commitment to increasing shareholder capital returns, I am upgrading Borr Drilling’s stock from “Hold” to “Buy“.

Read the full article here