Evolv (NASDAQ:EVLV) is the AI security provider that has ‘reinvented’ the metal detector with the help of AI, producing a host of advantages:

- Unlike metal detectors, Evolv portals also scans non-metallic weapons.

- It provides visual alerts that indicate the location of the item, allowing security personnel to conduct targeted searches more efficiently and non-invasively.

- It minimizes false alarms, which are rife with metal detectors.

- Roughly 10x the throughput of metal detectors, producing a better user experience as they can simply walk through the gates at normal speed, no need to stop, empty pockets, etc.

- Fewer security people are needed, so it saves costs for customers.

- Easy setup, it can be deployed in less than five minutes by a single person

There was some hiccup in Q1 as negative publicity from shorters lengthened sales cycles somewhat, but the company is back on track, and we’re really not worried about the shorters as there is overwhelming evidence that the technology works, and it is also improving.

The company supplies to multiple verticals, most notably education, hospitals, large venues and stadiums, and a new promising one, industrial warehouses. It sells 70% through channel partners, Motorola is a prominent one (which produced a 196% increase for the company in Q2), others are Johnson Controls, Securitas Technology, and Alliance Technology Group.

Growth drivers

- Market: security concerns are high with ubiquitous gun violence in the US, now there is a system with high throughput and AI-driven detection that can reduce the risks for public buildings like schools, hospitals, warehouses, large venues, and the like, and

- New customers

- New verticals: Industrial warehouses

- Channel partners, 70%, Motorola, ASM Global

- Upgrades and new products

Customers

- The company has many premier customers:

EVLV IR presentation

The company added 84 new customers in Q2 and now serves 800+ customers across 10 verticals (the IR presentation above is a little dated). Some of the new customers:

- Evolv gained 441 new multiyear subscriptions to Evolv Express

- They have 40 sports stadiums across five major leagues, 400+ hospital buildings, 22 of the largest school districts and 1000+ school buildings as customers.

- New Q2 major additions were Soldier Field (Chicago Bears) and the Target Center (Minnesota Timberwolves). Two wins in the NHL Ice Hockey League, the Honda Center, the Canadian Life Center, the T-Mobile Arena and the MGM Grand Garden Arena, and after the close of Q2 they added the Moda Center, and Charlotte Football Club. There are many more customer wins, they PR only the big ones.

- Evolv has a deal with ASM Global, which operates 350 of the world’s biggest arenas, and has chosen Evolv as its preferred screening technology provider. They doubled the ASM sites to 16 in Q2.

- The company added 28 new education customers and a 60% sequential increase in Evolv Express, which 60% of the customers choosing the distribution model. In education, there is considerable competition due to simpler products (basically metal detectors) that offer lower prices.

- There were 12 new healthcare customers in Q2, taking the total to 400. Competition is less here than in education, they have a 100% close rate in healthcare.

- The company is also moving overseas, for instance providing security to European venues like the Olympics.

New products

There was a major software update in Evolv Express for existing customers, “The update introduces new capabilities to the myEvolv portal and launches our new mobile app… Key new features include market-specific default dashboards, an intuitive threat map report, automated screening reports, real-time data updates, and extended alert image data access.” (Q2CC).

The company has introduced its Visual Gun Detect product last year, able to identify open carry approaching a venue, this can be an up-sell as well as a separate sell.

The company will introduce two new, unspecified subscription-based products by yearend, one digital and one physical.

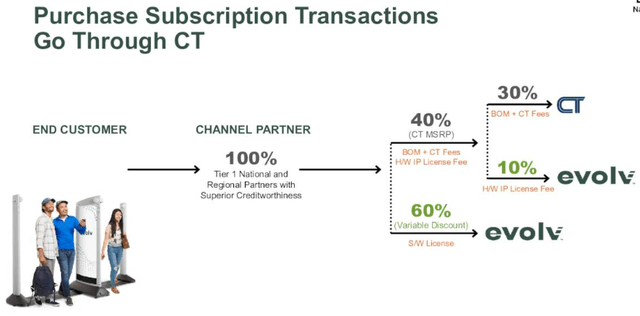

Change in business model

The company is shifting towards what they call the distribution model, which produces recurring revenue and boosts gross margins.

Customers preferring the CapEx model (upfront equipment purchases) can now place hardware orders directly with contract manufacturer CT (Columbia Tech).

EVLV IR presentation

Columbia Tech became its distributor as well, enabling the company to move to a distribution model, which has the following elements:

Customers purchase the hardware component directly from the contract manufacturer while entering a long-term software subscription contract with Evolv.

For Evolv, this shifts revenue away from hardware towards subscription, which will be 80% of revs ultimately. It creates a very high margin license revenue (for equipment sales) from CT that gets recognized immediately and will ultimately produce 20% of revenue.

It tends to reduce ARR (as hardware sales are no longer part of ARR) but that’s more than compensated by the shift itself. It reduces capital outlays as the company buys the hardware for the customers that rent it.

It also slows revenue growth (+4% in Q4) as hardware sales now go through CT, so we see ARR growing much faster than revenue. Increases gross margin (from 5% in FY22 to 45% in FY23 to 58% in Q2 and management guided 60% for FY24) with further upside beyond.

The distribution model was 25% of all units booked in Q4/23, but management sees it improving every quarter, and it reached 40% in Q2 and 50% by yearend.

Critics are wrong

10% of the float is short, management has already refuted the short thesis some time ago (and again here), but there are two investigations (from the FTC and the SEC).

We can think of a host of reasons why these critics are wrong. We think that while management might have made aggressive claims a couple of years ago about the technology, there is overwhelming evidence that it works:

- The company has 800+ customers, most of these went through extensive vetting with trials, and the company is winning new customers every quarter.

- The technology keeps on improving through more data and machine learning.

- Renewals, of the 12 expiring contracts in Q1 3 didn’t renew of which 1 went bankrupt. 45% of booked ARR in Q2 was from existing customers, compared to 37% in Q2/23.

- The company has a 100% close rate in healthcare.

- our competition has weaponized the regulatory issues, and we’re taking those on early in the sales cycle instead of being surprised at the end. And because of that, we were able to keep a high close rate

- Evolv Express to tag, on average, more than 500 firearms every single day.

- New York is seriously considering implementing Evolv in its subway, even when Evolv’s CEO has argued that subways are a difficult terrain for the technology.

- Evolv Express won awards (here and here for the most recent ones).

- Evolv was awarded another patent for Evolv Express in the US and several other countries for a total of 30

Financials

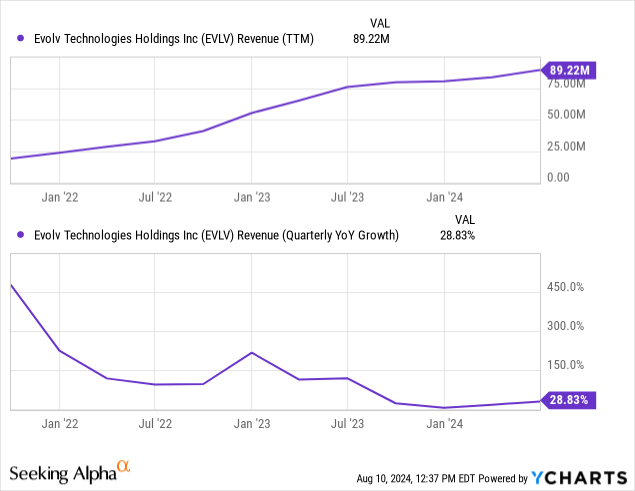

The hypergrowth is really over and the growth figures are affected by the change in the business model:

- Revenue up 29% y/y and a promising 18% q/q to $25.5M

- ARR +64% y/y to $89M

- 83% of revenue is recurring, versus 59% a year ago

- RPO (remaining performance obligations) +33% to $263M

- Adj gross margins at 58% versus 38% Q2/23

- Adj OpEx $26.5M versus $23.7M. They have some 150 people in sales

- Adj net loss $11.1M versus $14.3M in Q2/23

- Adj EBITDA loss $7.9M versus $13.8M in Q2/23

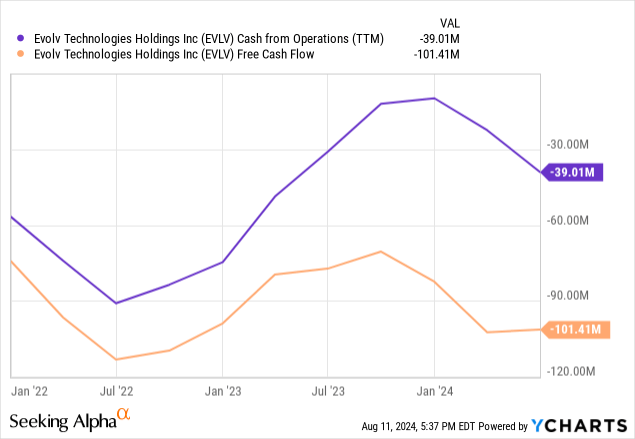

- Cash $57M vs $81M end of Q1

Reaffirming Outlook

- $100M revenue (+25%), ARR $100M (+33%) Adj gross margin at 60%, and a 40% improvement in adj. EBITDA.

- The (in our view, likely) NY subway win and possible subsequent subway wins are not in the outlook, they are not even in the TAM at this point.

The cash flow graph looks ugly as the big improvement last year seems to have reversed, but this is on the back of increasing inventories for the transition to a new generation system.

According to management, cash will bottom in Q3 but recover to $60M in Q4 (Q2CC):

as this distribution model is popping up is moving some of our equipment, which was originally in fixed assets back to the inventory line in anticipation of distribution model growth.

Management expects to reach positive EBITDA in Q2/25 with the same level of cash, that is, roughly $60M, which means they do not need additional financing (and will only do this when required for M&A).

Valuation

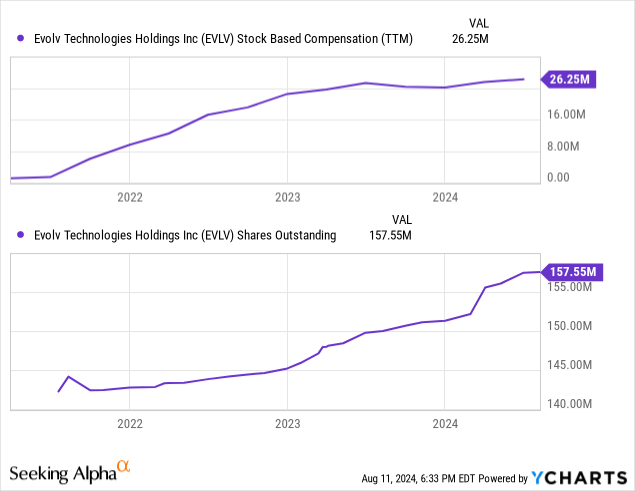

No red or even yellow flags from SBC nor dilution, but there are another 15M dilutive securities (warrants, options, RSUs) in the diluted share count of 172.5M and a potentially dilutive (that is, non-vested) 47M shares.

At $3 per share the company has a market cap of $603.7 and an EV of $543.8, the shares are selling at 5.4x EV/S. Insiders seem to think this offers good value as one director buys 50K shares at $3 and another one 8.3K at $3, we agree.

Conclusion

We see many attractive features:

- While we wouldn’t go as far as to argue that Evolv has cornered the market, the premier customer lineup clearly shows them to be the market leader.

- We’re still in the very early innings of its expansion. There are plenty of markets to go after, new segments even present themselves without much company effort, like subways in major cities, and the company hasn’t done much, if any, internationally (apart from its deal with ASM Global).

- The company has made a very attractive business model, consigning hardware sales to its contract manufacturer whilst garnering an upfront 10% royalty on hardware sales and recurring SaaS subscription on the software, even if not all of the customers will ultimately be on that model, boosting ARR and gross margins.

- The main risk is that no technology is 100% foolproof, although its solutions have gone through rigorous testing by multiple big customers and are used daily by 800 customers, a single high-profile security breach can’t be excluded.

The upshot: We think the shares are a strong buy at $3.5.

Read the full article here