Investment thesis

My previous bullish thesis about MercadoLibre’s stock (NASDAQ:MELI) aged extremely well as the stock delivered a 20.5% price increase since early May. The U.S. stock market returned around 8% to investors over the same period.

The company recently delivered a staggering Q2 earnings report, with all the most vital metrics demonstrating immense growth momentum. MELI operates across emerging markets and thriving industries, which are apparent powerful tailwinds that power growth. Moreover, my valuation analysis suggests that the stock is still extremely attractively valued. All in all, I reiterate a “Strong Buy” rating for MELI.

Recent developments

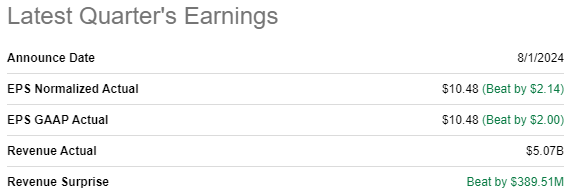

MELI released its latest quarterly earnings on August 1, confidently surpassing consensus revenue and EPS estimates. Revenue growth accelerated once again with increasing YoY by staggering 49%. The adjusted EPS more than doubled, from $5.16 to $10.48.

Seeking Alpha

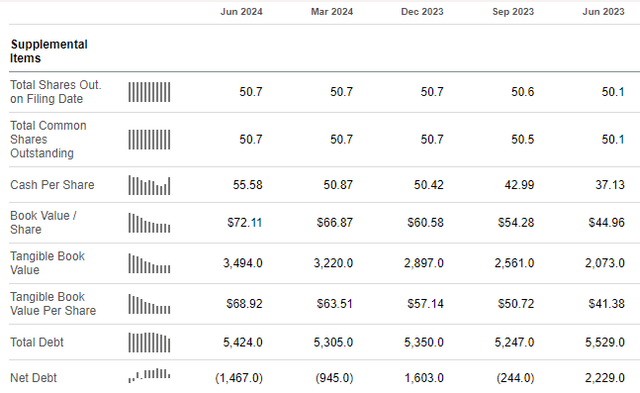

Robust growth momentum in revenue and EPS positively affected the company’s cash flows. Cash from operations delivered strong YoY growth in Q2, from $1,412 million to $1,882 million. MercadoLibre generated around $850 million levered free cash flow [FCF] in Q2. This was around twice as high compared to the same quarter last year. As a result, MELI’s balance sheet continued fortifying rapidly during the quarter. The company currently boasts a $6.9 billion cash pile, and its net cash position improved sequentially from $945 million to $1,467 million.

Furthermore, over the last four quarters, MELI significantly improved its financial position from $2.2 billion in net debt to almost a $1.5 billion in net cash. Improving balance sheet is always a big green sign for me, as it is evidence of the management’s well-disciplined approach to capital allocation and prioritization of improving financial flexibility.

Seeking Alpha

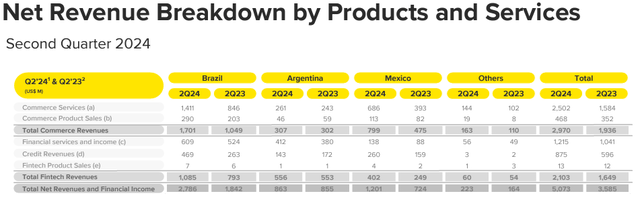

Now, let me deep dive into MELI’s fresh earnings report. Massive YoY growth across all of the crucial metrics is strong evidence the company is well-equipped to sustain stellar revenue growth momentum for longer. The most important to me is that MELI demonstrated growth across all products and services: both Commerce and Fintech.

MELI’s latest earnings presentation

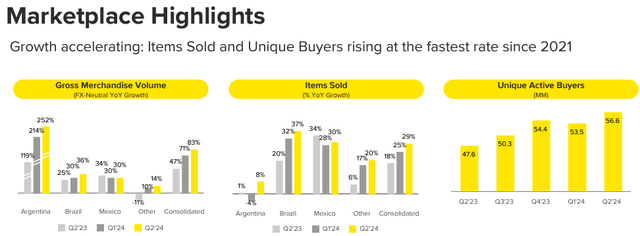

MELI’s growth in Commerce appears to be of a high-quality because it was driven across all key business metrics. Brazil and Mexico demonstrated an above 30% FX [foreign exchange] neutral gross merchandise value [GMV] YoY growth. The number of items sold grew by 29% YoY and unique buyers grew by 19% YoY. As we see, the segment’s growth was fueled by the double-digit strength in all three vital variables, which means that the momentum is likely to sustain for longer here.

MELI’s latest earnings presentation

The Fintech business observed even more impressive growth across most vital metrics. Monthly active users’ [MAU] growth accelerated to 37% YoY and there are currently 52 million users of Mercado Pago. Strength in MAU dynamic also supported staggering growth in assets under management [AUM], which grew by 86% YoY. Fintech’s credit portfolio’s growth was impressive as well, with a 51% YoY increase. It is also crucial to emphasize that the credit card portfolio recorded an unbelievable 146% YoY growth.

MELI’s latest earnings presentation

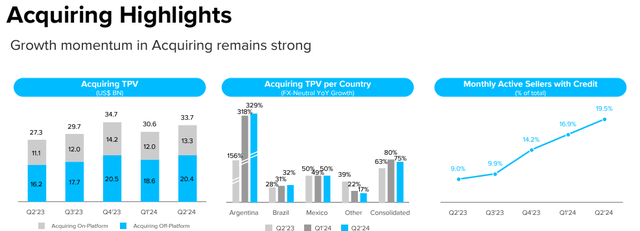

Since MELI is an ecosystem, it also leverages synergies by being both a Commerce and a Fintech business. Acquiring looks like a good metric to assess the magnitude of synergies generated by being an ecosystem. The acquiring total payment volume [TPV] grew by 24% YoY and the growth has been solid both on- and off-platform. Let us also not forget about merchants, another crucial part of MELI’s ecosystem. The proportion of monthly active sellers with credit grew from 9.0% to 19.5% YoY, which is another positive sign. The more flexibility of payment terms merchants offer to users, the higher is the probability of a further growth in GMV.

It is also crucial that MELI’s business has a solid footprint across the largest of Latin America’s economies, mitigating geographic concentration risks. For instance, in Q2 Argentina demonstrated almost invisible growth, but it was by far offset by impressive performance in Brazil and Mexico. According to the International Trade Administration, Brazil’s e-commerce market is expected to compound with a 14.3% CAGR by 2026. Mexico’s e-commerce market is projected to growth with a 12.4% CAGR over the next decade. That said, even if Argentina continues delivering low growth, MELI has two big markets which are expected to continue demonstrating solid e-commerce over the long term. From the Fintech business perspective, the future also looks bright, as Boston Consulting Group forecasts that the Latin American fintech industry will be led by Brazil and Mexico and is poised to compound with a 29% CAGR by 2030.

Last but not least, the company is extremely efficient in converting key operating metrics success and top-line strength into the bottom-line profitability expansion. MELI demonstrated a solid improvement in the net income margin on a YoY basis and sequentially. Apart from revenue growth, profitability expansion was driven by the significantly improved Commerce take rate, from 18.4% to 23.5% YoY.

Valuation update

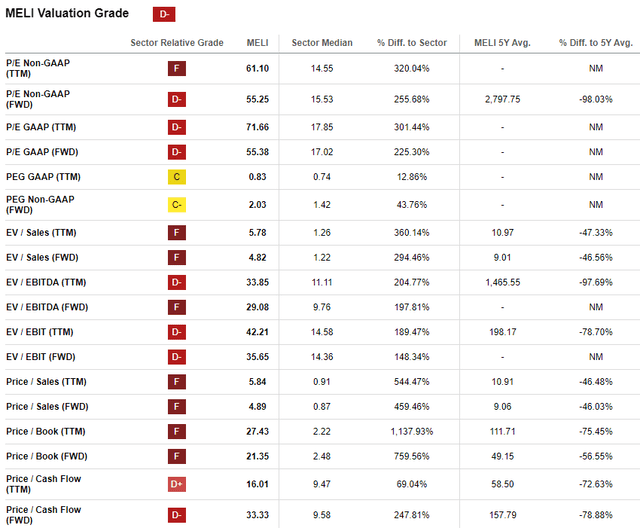

MELI rallied by 59% over the last twelve months, substantially outperforming the broader U.S. stock market. The YTD performance has been more modest so far, with around 26% rally. MELI’s current valuation ratios look extremely attractive compared to the company’s historical averages. That said, I believe that MELI appears to be very attractively valued from the perspective of ratios.

Seeking Alpha

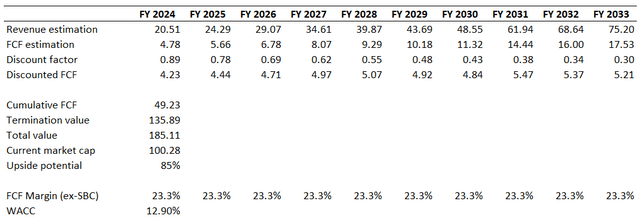

Analyzing only valuation ratios is unlikely to be sufficient for a growth stock like MELI. Therefore, a discounted cash flow [DCF] model must be simulated using a 12.9% WACC. I rely on consensus revenue estimates for my DCF, which projects a 16% CAGR for the next decade. This might appear too optimistic for some, but I would like to remind that e-commerce penetration is still low in Latin America and expected to reach 16% only in 2025. The same source adds context that in China and South Korea, penetration of e-commerce is substantially higher at 30%. That said, there is still a vast potential for MELI’s Commerce business to deliver double-digit growth. Latin America’s fintech market is projected to grow with a 26.2% CAGR, which is also a robust tailwind for MELI. Therefore, I believe that a 16% revenue CAGR is fairly conservative. To be conservative, I expect a flat 23.3% FCF margin, which is MELI’s TTM level ex-stock-based compensation.

Author’s calculations

According to my DCF simulation, the fair value of the business is $185 billion. This is 85% higher than MELI’s current market cap, meaning that the stock is massively undervalued.

Risks update

When I look at MELI’s share price chart over the last five years, I see that a $1,900-$2,000 is a strong resistance range and while the stock is currently within this range investors might see a new pullback in the share price. Investors should be aware that MELI is certainly a long-term play, and I recommend the dollar average to mitigate the substantial volatility risk.

Seeking Alpha

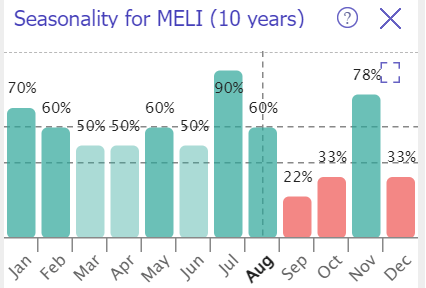

According to the stock’s historical seasonality patterns, MELI usually performs much weaker in the last four months of a year compared to the period from January to August. September is especially weak, and together with trading in a strong resistance zone, means that there is a notable probability of a temporary pullback before the growth continues.

TrendSpider

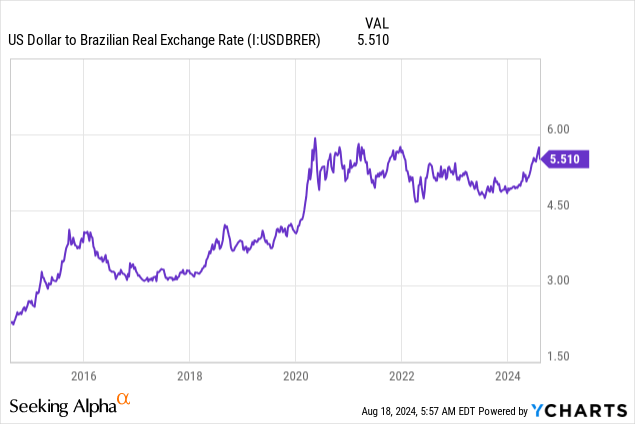

MercadoLibre operates across emerging markets, which are inherently riskier because political and legal institutions are still evolving and are less stable compared to developed economies. This instability might lead to sudden changes in governmental policies, regulations, and taxation. Currencies of emerging economies are also inherently more volatile compared to USD or EUR. For example, Argentina’s peso might demonstrate up to 50% plunge within relatively short timeframes. The Brazilian Real is a more stable currency, but it still notably weakened against the U.S. Dollar over the last decade. Before investing in MELI, investors should be aware of political and substantial foreign exchange risks.

Bottom line

To conclude, MELI is still a “Strong Buy”. Its operational and financial performance is exceptional, with business demonstrating double-digit growth across almost all crucial metrics. The stock is extremely undervalued and MELI’s balance sheet is improving rapidly.

Read the full article here