Earnings season has come and gone. It was not nearly as strong as those of the past four quarters. Earnings and sales surprises were both down dramatically, which has led to downward earnings revisions for the S&P 500 and the Nasdaq 100. This could be a problem for the market-cap weight large-cap indexes because solid fundamentals have not driven the moves but have been driven by expanding price-to-earnings [PE] multiples.

So far, 82 of the 100 companies in the Nasdaq 100 have reported an aggregated earnings surprise of -0.91% and an aggregated sales surprise of 0.61% – the weakest performance since late 2022.

Bloomberg

Similarly, 464 of the 500 companies in the S&P 500 have reported showing an aggregated earnings surprise of 4.1%, with an aggregated sales surprise of 0.77%, again the weakest performance since the fourth quarter of 2022.

Bloomberg

Downward Earnings Revisions

As a result, 2024 earnings estimates for the S&P 500 have been revised downward to $240.64 per share from roughly $243 at the end of June, despite sales estimates remaining flat. The primary reason is shrinking profit margins, which have fallen to about 12.9% from roughly 13%.

Bloomberg

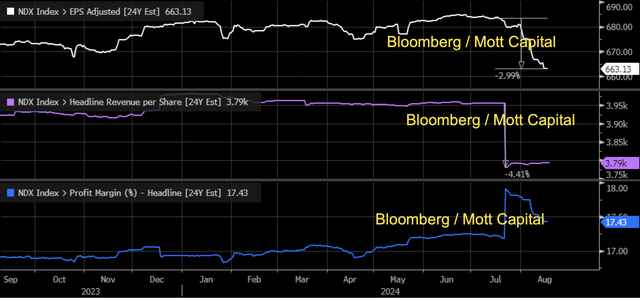

The Nasdaq 100 has seen even more significant revisions, with earnings estimates dropping by approximately 3% to $663.13, despite margins slightly improving to 17.4%.

Bloomberg

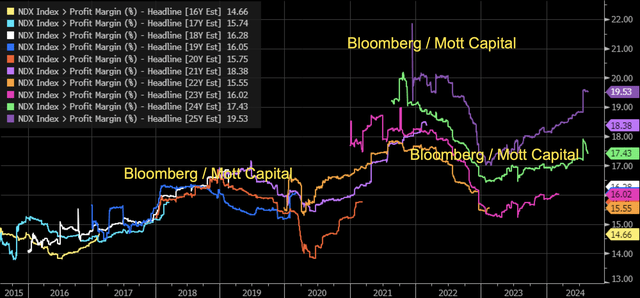

2025 Estimate At Risk

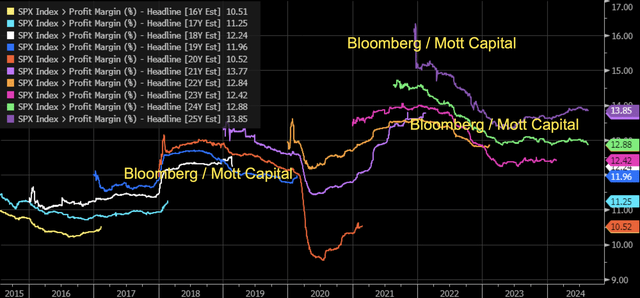

In 2025, margin estimates for the S&P 500 and the Nasdaq seem overly optimistic. Margin estimates for the S&P 500 are forecast to expand to 13.85%, which would be higher than previous highs seen in 2021. It seems odd to think that at this point in the cycle, with inflation coming down sharply, margins are not only going to expand in 2025 from 2024 levels but also climb to a record high in 2025.

Bloomberg

For the Nasdaq 100, margins are expected to expand to 19.5% in 2025, rising beyond the levels seen in 2021, when they reached roughly 18.5%. More interestingly, they’re expected to expand by almost 200 bps.

Bloomberg

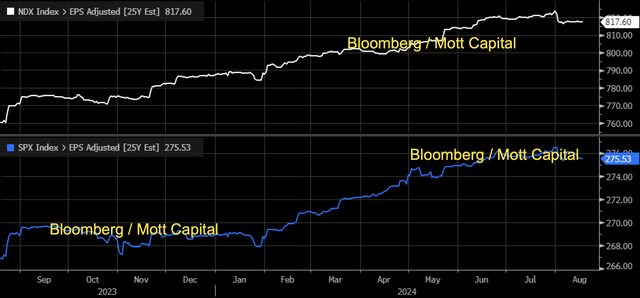

This implies that if margin estimates in 2025 are too high and are likely to come down, earnings estimates for both the Nasdaq and the S&P 500 are going to have to head lower, too, and those estimates are too high at $817.60 per share and $275.53 per share, respectively.

Bloomberg

PE Expansion

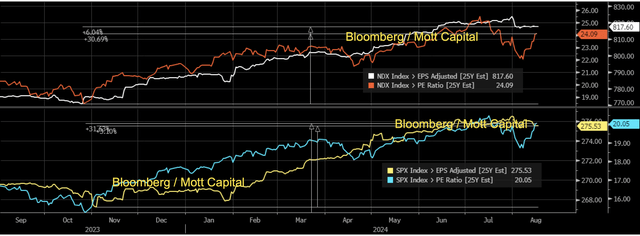

Overall, falling earnings estimates and rising stock prices tell us that the source of the higher move in equities isn’t due to improving fundamentals but expanding PE multiples, and that has been the driver of nearly the entire rally since October. In fact, since October 2023, earnings estimates for 2025 have only increased by 3.1% for the S&P 500 versus almost 32% for the PE ratio. Meanwhile, earnings estimates for the Nasdaq have climbed by 6%, while the PE ratio has increased by 30.7%.

Bloomberg

If earnings estimates for 2025 do roll over, either the market will have to adjust for the slower-than-expected growth in 2025 and lower estimates, or the market risks growing more expensive relative to those earnings estimates. From a fundamental standpoint, this does not paint a favorable risk-reward profile for the large-cap market-weighted indexes moving forward.

Join Reading The Markets

Reading the Markets helps readers cut through all the noise, delivering daily video and written market commentaries to prepare you for upcoming events.

We use a repeated and detailed process of watching the fundamental trends, technical charts, and options trading data. The process helps isolate and determine where a stock, sector, or market may be heading over various time frames.

Read the full article here