Summary

I am neutral on Expeditors International of Washington (NYSE:EXPD), as there is very little visibility into the earnings growth outlook over the medium term. While I acknowledge the near-term strength stemming from the Red Sea conflict situation, I don’t think the market appreciates what happens when the conflict gets resolved. EXPD is currently trading at 23x (the high end of its historical trading range), which means there is plenty of room to fall if the risk I highlighted below plays out.

Company overview

EXPD is an international forwarder of air and ocean freight that has a global presence. The United States is EXPD’s largest revenue contribution region (36%), followed by North Asia (23%), Europe (19%), and the rest from South Asia, MEA, India, etc. By segment split, air freight [AF] accounts for ~28% of net revenue, ocean freight [OF] is 22%, and customs brokerage [CB] is 50%.

In EXPD’s most recent quarter (2Q24), total revenue came in at ~$2.44 billion, which translates to $800 million in net revenue (a 32.8% margin). Driving the ~9% total growth was AF seeing 14.5% y/y growth, OF seeing 9.7% y/y growth, and CB seeing 3.6% y/y growth. However, profitability was a miss, with EXPD reporting 2Q24 operating EPS of $1.24, $0.03 below consensus estimates. This was largely driven by a greater cost of transportation as net margins were compressed across all segments: both AF and OF net margins were compressed by 510 bps y/y, and CB net margins were compressed by 110 bps y/y.

Near-term performance likely positive

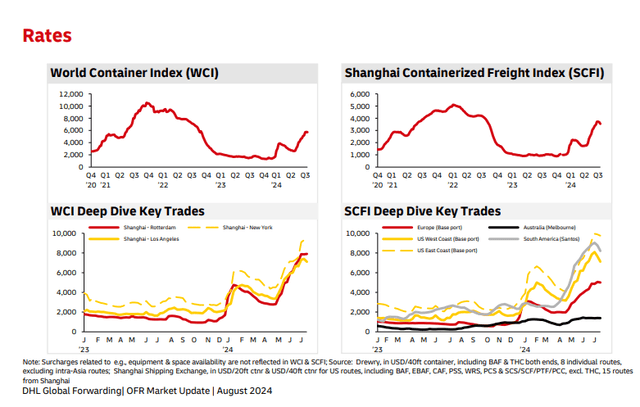

DHL

EXPD’s near-term performance is probably going to stay positive given the current macrodynamics. The current red sea situation continues to be a massive tailwind for EXPD (and the industry, basically) as clients continue to pull forward their freight demand in anticipation of peak demand season. The idea is to ensure they have enough inventories and also to lock in freight prices that are rising across the board. Suppose the pull-forward effect steps up as the red sea conflict situation worsens; this could drive rates even higher, enabling EXPD to pass costs onto shippers to expand its net margin.

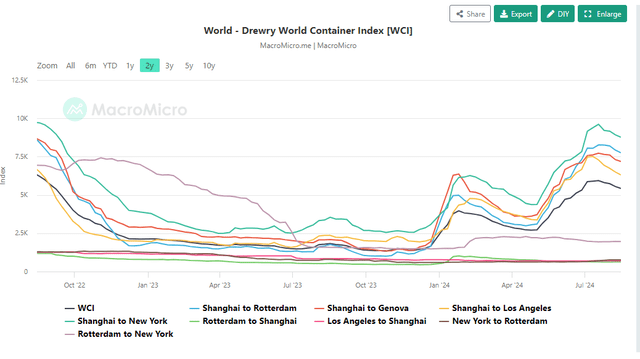

MacroMicro

Based on EXPD historical OF net revenue growth per unit (OF net revenue growth minus OF volume growth to get this) vs. the WCI index y/y change, OF net revenue growth generally lags by 1 quarter. With WCI spiking in recent months, it suggests a potential sequential growth acceleration for EXPD’s OF net revenue per unit in 3Q24.

Moving onto the AF segment, the strong volume growth (15%), mainly driven by e-commerce demand out of North Asia, was a pleasant surprise. Notably, volume growth accelerated throughout the months, with volumes in April up 13%, May up 15%, and June up 19%. The momentum doesn’t seem to be slowing down based on Temu’s (PDD) operating metrics (for disclosure, TEMU grew US GMV by ~6x vs. last year). Absence any major changes to the industry dynamics (i.e., the tariff risk I note in the below section), EXPD should continue to see strong demand here in the near-term.

However, medium term outlook is uncertain

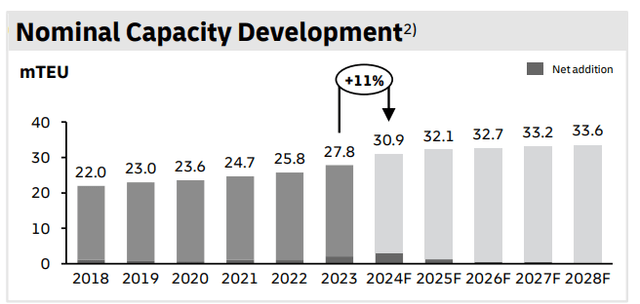

Refer to link above (DHL)

That said, I think there is very little visibility into how EXPD will perform over the medium term. Firstly, regarding the e-commerce strength seen in the AF segment, it could be heavily disrupted by the potential increase in tariffs, depending on who wins the upcoming US election.

Secondly, given the attractive rate environment, I expect more capacity to continue coming online (per DHL estimates, nominal capacity will increase by 11% in FY24 to 30.9 mTEU, followed by another 4% in FY25). This should put a limit on how much rates can continue increasing unless demand for goods sees a much stronger improvement from here. This could happen, but I am wary of the fact that the consumer spending environment has not fully recovered yet. Although Walmart came out the other day saying that consumer spending has not weakened, note that many other companies have spoken otherwise, and consumer sentiment still remains poor. Suppose demand fails to catch up with the new supply; it could result in pricing pressure for EXPD.

Thirdly, nobody knows when the Red Sea situation will be resolved. Based on where rates are today, the market seems to be expecting the situation to last for the near term. But what if the situation gets resolved earlier than expected? Suddenly, businesses and retailers realize they do not need to pull forward their demand anymore, and this results in a massive demand plunge. Coupled with the growing freight supply, it could result in both volume and pricing plummeting for EXPD.

Valuation

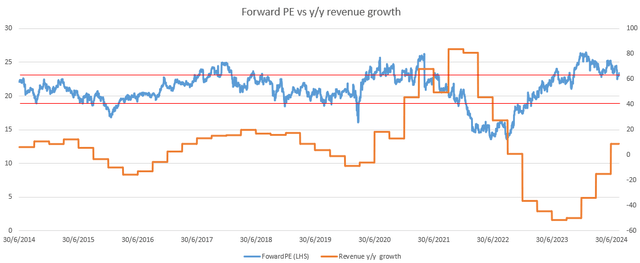

Source: Author’s calculation

Finally, the last piece of the puzzle that forced me to stay on the sidelines is the high valuation that EXPD is trading today. Relative to EXPD’s trading history, where it tends to trade within the range of 18.5x to 23x forward PE, the stock is currently trading at the high end of the range (at 23x). The market appears to be only focusing on the near term and not appreciating the risk that I have laid out above over the medium term. By comparing y/y revenue growth to the forward PE movement, we know there is a strong relationship between the two, and if I am right about the risk above, the valuation multiple could see a sharp downward revision. Depending on the magnitude of the decline, the valuation multiple could drop all the way back to 14x, like it did in 2022.

Conclusion

My neutral view on EXPD is because of the lack of visibility over the medium term earnings growth. While EXPD is currently benefiting from a favorable industry backdrop, driven by geopolitical tensions and robust e-commerce growth, the uncertainty surrounding the duration of these tailwinds, coupled with potential headwinds from increased capacity, makes it challenging to forecast growth over the medium term. In addition, EXPD is not trading at a cheap level (relative to history). Hence, I maintain a neutral stance on the stock.

Read the full article here