Introduction & Investment Thesis

I last covered Pinterest (NYSE:PINS) on June 13, where I reiterated my “buy” rating as it continued to demonstrate progress against its strategic initiatives to deepen user engagement, especially among Gen Z’s, by leveraging AI to drive higher relevance and personalization while building lower funnel solutions for advertisers to drive higher monetization and ROI in ad spend.

Although the stock had initially climbed 31% from my first “buy” rating to a price of $45, it has since declined over 10% since my first coverage and 29% since my last coverage, underperforming the S&P 500.

Pinterest reported its Q2 FY24 earnings, where it saw revenue and Adjusted EBITDA grow 21% and 68%YoY, respectively, with MAU’s (Monthly Active Users) reaching a new high of 522M while ARPU (Average Revenue per User) grew 8% YoY to $1.64, with the US & Canada region doing most of the heavy lifting.

Although the company continued to drive with operational excellence and strong product innovation, I believe that the recent pullback is driven by the management’s Q3 revenue and earnings guidance, where it expects revenue growth to slow to 16–18% YoY as it faces tougher comps, along with flat margins on a year-over-year basis. Given the macroeconomic uncertainty as well as low ad pricing in international markets, it is likely that investors have gotten weary as to whether the company will be able to meet its 3-5 year financial projections of 30% Adjusted EBITDA margins.

While the concerns are valid, I believe that even if the company sees a slowdown in revenue growth to the low teens over the next 2 years, along with a lesser than expected margin growth of 27%, the stock is still undervalued at current levels. As an investor, I have used the opportunity to buy more shares at current levels, and I believe that the stock remains a “buy” with an upside of at least 32% over the longer term.

The good: Strong user engagement and monetization, with MAUs and ARPU growing 12% and 8% YoY, respectively

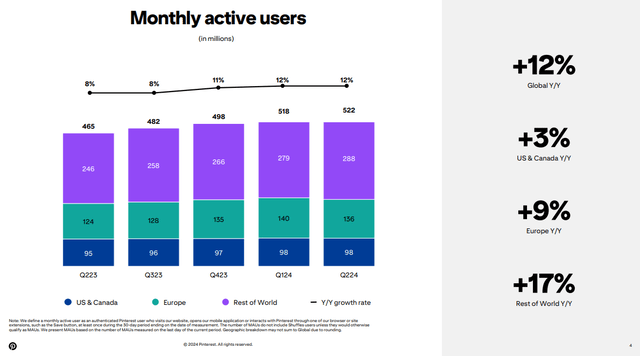

Pinterest reported its Q2 FY24 earnings, where revenue grew 21% YoY to $854M as the management continues to execute on its strategic initiatives of driving user engagement and monetization by rolling out AI-powered products and experiences, leading them to gain share of advertising budgets with large brands. During the quarter, the company saw its MAUs grow 12% YoY to 522M (at the same pace as the previous quarter), with the US & Canada accounting for 55% of all MAU’s growing 3% YoY, while Europe and RoW (Rest of the World) contributed the remaining 45% of all MAU’s growing 9% and 17% YoY, respectively.

In my previous post, I had analyzed the management’s progress across their three strategic priorities, which include: 1) growing their user base and deepening engagement; 2) improving monetization; and 3) accelerating their audience reach through third-party partnerships and resellers. In this post, I will take a similar approach and break down key updates across each of the aforementioned initiatives and tie them together into Pinterest’s investment thesis.

Starting with growing its user base and deepening engagement, Pinterest continues to utilize AI to drive higher relevance and personalization where they upgraded their search ranking algorithm and bolstered content discovery with gen AI-based guided search, resulting in a significant increase in their global search fulfillment rate. Meanwhile, they are also doubling down on curation through boards and collages by launching board sharing and interactive pins to help users navigate along their journey, resulting in a higher number of saves, especially among their fast-growing GenZ cohort, while increasing actionability with better shopping capabilities and features such as video shopping ads that have doubled the number of outbound clicks they send to advertisers on a year-over-year basis for the third quarter in a row.

Q2 FY24 Earnings Slides: MAUs continue to reach new highs

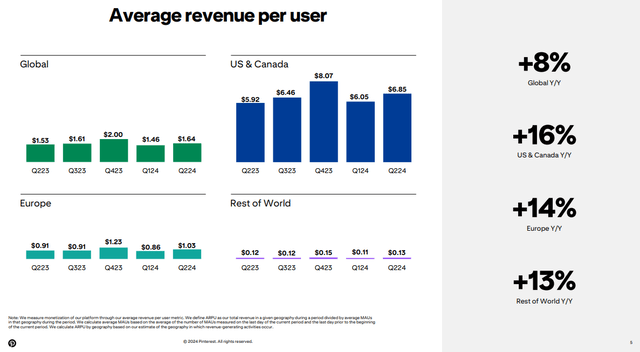

Moving on to the second strategic priority, which is improving monetization on the platform, Pinterest saw its ARPU grow 8% YoY to $1.64, with the US & Canada growing at the fastest rate among all other geographic segments. In my previous post, I discussed how the company is investing to build lower funnel offerings that are creating significant value for advertisers as they make the purchase journey for users more seamless with products like mobile deep linking and direct links. During the earnings call, the management discussed that large advertisers are increasingly voting their dollars and driving more budget to Pinterest, especially as they roll out their new automation suite Performance+ to increase efficiency of campaign setup as the next iteration of their lower funnel suite, which should result in improved cost per acquisition and higher ROI on advertising spend, in my opinion.

Q2 FY24 Earnings Slides: Trend of ARPU over the last 1 year

Finally, Pinterest continues to accelerate their audience reach and monetization through third-party ads to gain market share, especially in unmonetized international markets, as well as fill gaps in the auction. It already has partnerships with Amazon Ads and Google Ads Manager, which have been ramping steadily, while Pinterest is focused on easing the onboarding process for advertisers and helping them understand how privacy-centric measurement solutions such as Conversions API and Clean Rooms can strengthen their conversion visibility.

The bad: Profit margins expanded, but low eCPM in unmonetized markets can sabotage Pinterest’s 3-5 year target, revenue growth is expected to slow down in Q3

Meanwhile, Pinterest generated $180M in Adjusted EBITDA, which grew over 68% YoY, with a margin improvement of 600 basis points as it streamlined its operating expenses, especially in Sales & Marketing which amounted to 27% of Total Revenue, compared to 31% in the previous year, while unlocking operating leverage from driving higher ARPU. However, I would like to point out that Pinterest saw a greater mix shift to ad impressions with lower average pricing or eCPM during the quarter, as they started serving ads in previously unmonetized markets, particularly in RoW, which have lower eCPMs compared to existing monetized markets, along with growth in third-party ad impressions that filled in gaps in their auction in places that were previously under monetized or not monetized at all. While the management believes that ad pricing or eCPM will grow over time, this can also lead to margin pressure in the event it fails to gain traction, thus putting its 3-5 year plan of reaching 30% Adjusted EBITDA margin in danger.

Simultaneously, the company also guided revenue growth to slow down to approximately 16.9% YoY growth rate to $892.5M as they face tougher comps from last year, along with the management outlining that they don’t expect a material improvement in trend for the food and beverage category or any meaningful revenue contribution from the launch of Performance+, as it is rolled out to a small set of advertisers. While the management did not provide full-year revenue guidance, it continued to emphasize that the underlying health of the business is strong as they make progress against their strategic initiatives.

Revisiting my valuation: Pinterest is a “buy”

Looking forward, the company expects to see a slowdown in its revenue growth in the 17% YoY range to $892.5M in Q4, while expecting to spend approximately $492.5M in non-GAAP operating expenses. Assuming that the Cost of Revenue remains anchored in the 21% range, it should generate an Adjusted EBITDA of approximately $212M with a margin of 23%, which would be flat on a year-over-year basis.

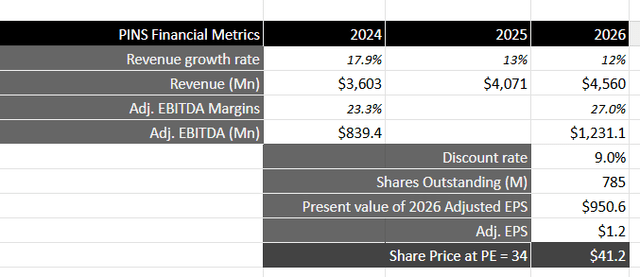

Assuming that the company continues to grow in the low teens over the next 2 years as it executes its strategic initiatives to deepen user engagement along their shopping journey from inspiration to actionability with AI-driven product innovation, while building robust lower funnel offerings for advertisers and third-party partners to help them better measure and drive higher ROI in ad spend, it should continue to see an increase in ad load with greater demand for its ad products, leading to higher eCPM. This will translate to a total revenue of at least $4.68B by FY26. Note that I have taken a growth rate that is lower than consensus estimates to factor in uncertainty with international monetization prospects as well as macroeconomic risks where consumer spending weakens from its current levels.

From a profitability standpoint, I will also take a cautious approach, and therefore I will go with the assumption that Pinterest may not be able to meet its 3-5 year target of achieving a 30% Adjusted EBITDA margin as international markets weigh down on the overall profitability. In that case, I will take an Adjusted EBITDA margin of 27%, which will translate to Adjusted EBITDA of $1.23B by FY26, or a present value of $950M, when discounted at 9%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% with a price-to-earnings ratio of 15–18, I believe that Pinterest should trade at least twice the multiple, given the growth rate of its earnings during this period of time. This will translate to a PE ratio of 34, or a price target of $42, which represents an upside of 32% from its current levels.

Author’s Valuation Model

My final verdict and conclusions

Even though the company continues to execute robustly against its strategic priorities, I believe that the current drawdown is a result of the latest revenue and earnings guidance for Q3, where it is expected to grow at a slower rate as it faces tougher comps, while margins are likely to remain flat on a year-over-year basis in Q3. This has likely made investors wary about whether Pinterest can indeed reach its 3-5-year target of 30% Adjusted EBITDA margins. Meanwhile, the macroeconomic environment in the US & Canada region remains uncertain with contradictory reports on the state of consumer health, while low ad pricing in under monetized geographies can put pressure on both the top and bottom lines of Pinterest.

However, the current state of investor pessimism has created an amazing opportunity to scoop up shares of this company that, I believe, is well positioned to win long-term given its strategic initiatives to engage and inspire their users along their shopping journey and translate their intent into actionability, resulting in strong monetization and ROI for advertisers as it builds innovative AI-led products while maintaining financial discipline. With the latest pullback, I have already added to my position and believe that the stock is attractively priced from a risk-reward perspective to drive significant long-term upside, making it a “buy.”

Read the full article here