Note: All amounts discussed are in Canadian Dollars. All prices referenced are for those on TSX.

On our last coverage of Emera Incorporated (TSX:EMA:CA), we gave it a passing grade as the stock was not egregiously expensive as when we had given it a “Sell” rating in June 2023. But we suggested investors follow us into ATCO Ltd. (ACO.X:CA) and avoid the pains of a dividend cut here.

The threat of a dividend cut is fairly high. We would continue to avoid Emera Incorporated stock until we get it at a sub 14X multiple. A dividend cut would also help realign the cash flow and the payout. This is hardly Draconian, considering we are getting superior quality companies at 10X multiples with far lower debt levels. We rate Emera Incorporated stock as a neutral/hold for now.

Source: Payout Ratio Likely To Go Past 100% For The 6% Yielder.

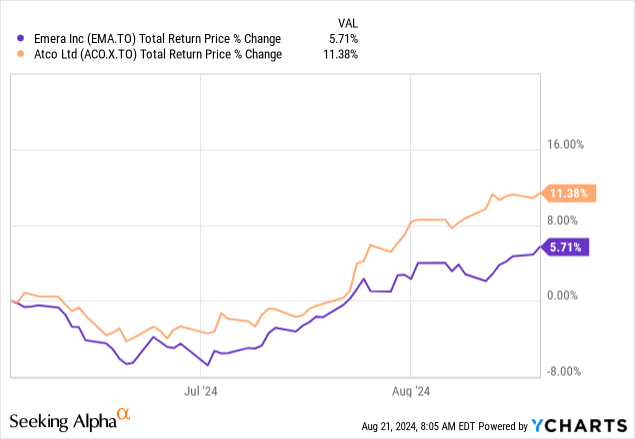

So far, that call has worked. Even though Emera is up, Atco is taking it down, 2:1.

We examine the Q2-2024 results and tell you why the dividend cut may be on our doorstep the moment we get the next credit spread jump.

Q2-2024 & The Dividend Coverage

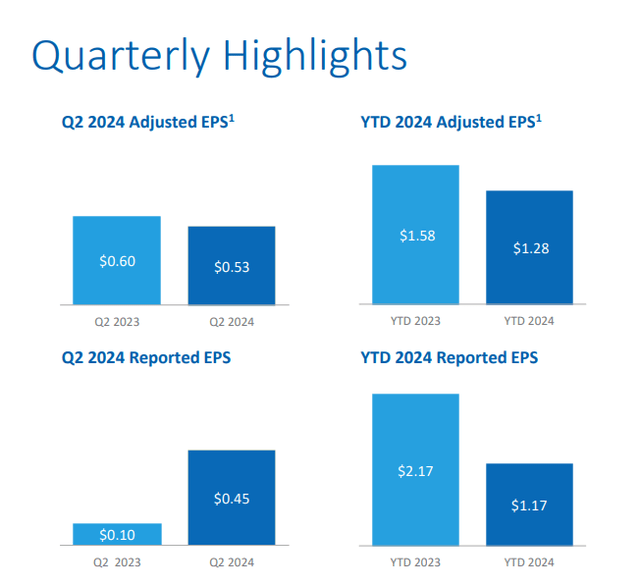

Emera continued its string of misses with a terrible set of second quarter results. Q2-2024 adjusted earnings per share were about 10% below consensus estimates. That is a pretty massive deal in utility land, where predictably is the name of the game. This was also the third quarter where Emera missed and analysts had to take down 2024 estimates once more. The biggest pressure was from the ramp in expenses relative to the regulatory lag in getting these through. Adjusted earnings per share were at 53 cents in the quarter, and a reminder here that the dividend is at 71.75 cents a quarter.

EMA Q2-2024

Utilities ideally like to have this ratio under 70% and tend to get jumpy once you go past the 80% level. Emera was at 135% in this quarter. If you think that 80% number is not critical, then consider what Emera said and did recently.

As part of a broader strategic initiative to reallocate capital towards investing in these high-growth opportunities, beginning today, Emera is adjusting its dividend growth rate to 1 to 2 per cent per year. This will have the effect of reducing Emera’s dividend payout ratio of adjusted net income(2) (payout ratio) to approximately 80 per cent by the end of 2027 with continued improvement in the following years.

Source: EMA Investor Day Conference Call Transcript (source: TIKR).

As recently as one quarter back, Emera was still singing that 4-5% dividend growth, while we kept forecasting a cut.

But I also say that we continue to believe that our dividend — current dividend growth profile is sustainable. That over time our EPS growth will outpace that 4% to 5% dividend growth profile, and therefore, our payout ratio will come down over time. And it obviously that will take some time, but we continue to be confident that our payer ratio will come down over time.

Source: EMA Q1-2024 Conference Call Transcript.

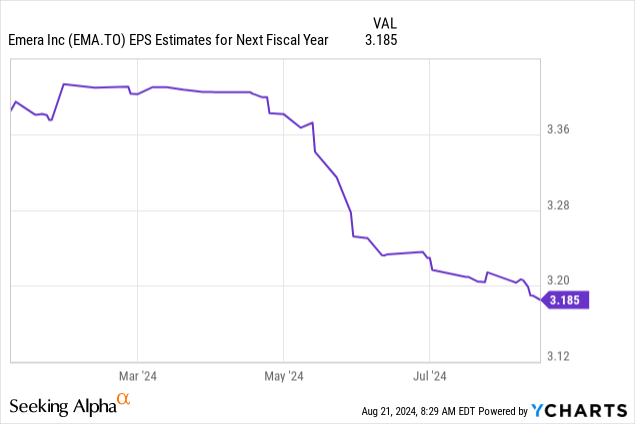

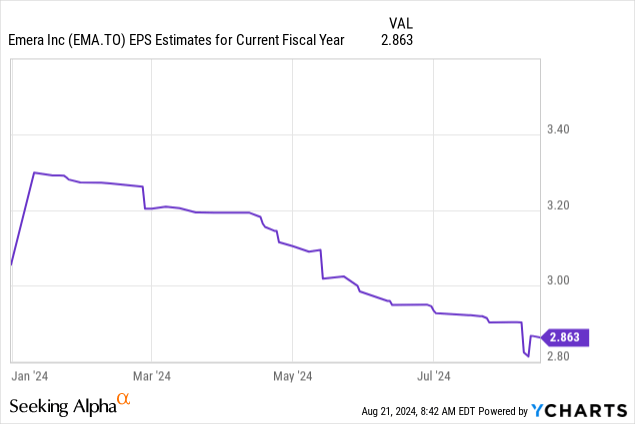

So, in our view, this is the central path that most companies take. First the growth comes down, or they move to a freeze, and then they cut. You never see a 180-degree turn right away. Current expectations are that the dividend payout ratio will be over 100% for all of 2024. For 2025, assuming Emera freezes the dividend, the payout ratio will be around 90%. You can see the deterioration in this number (2025 EPS) as well as it has moved from $3.40 to $3.18.

Outlook

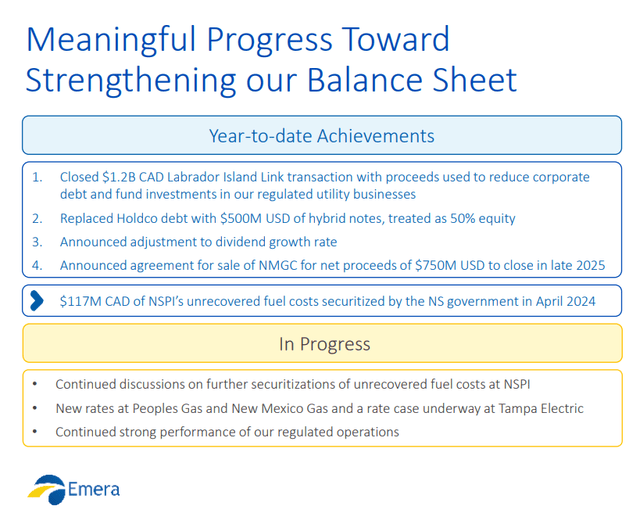

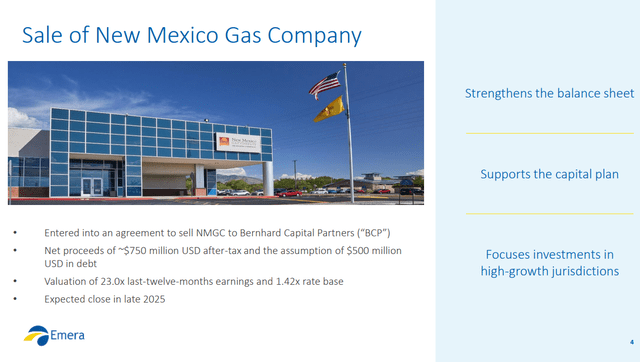

Let’s give Emera some credit for righting their balance sheet. This looked perilously bad at the beginning of 2024, and they have got two asset sales done (regulatory approval still pending though).

EMA Q2-2024

We are not regulatory experts, but there are several analysts concerned about the NMGC sale and believe there may be challenges to that deal. The multiple of that deal was fairly good, but actually lower than what estimates we saw out there (1.5X base rate).

EMA Q2-2024

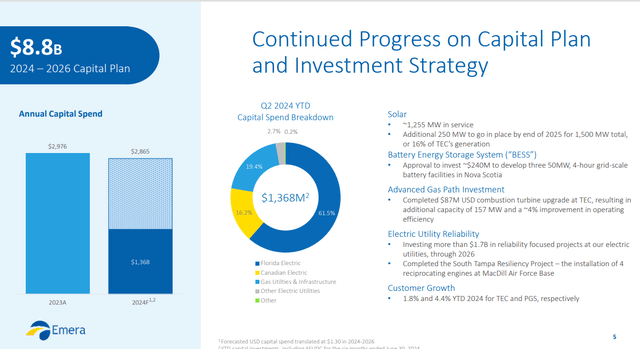

Considering both deals will take time to close (late 2025 for NMGC), Emera’s capital pans will remain unaltered for now.

EMA Q2-2024

Here lies the problem, as Emera will have to tread very carefully until the deal goes through. In the interim, if they have a misstep and if the odds of the deal falling apart increase, the credit rating agencies might take that axe with a “swing first, ask questions later” approach.

Emera is not exactly cheap, either. The stock is holding a 6X debt to EBITDA and trading at 19X earnings. Atco, the one we recommended as an alternative, trades at 11X earnings and carries a debt to EBITDA almost two multiples lower. Their dividend payout rate is about 50% for Atco vs. over 100% for Emera. So even if you suggest there is zero risk to the dividend, you really have to ask whether Emera remotely makes sense as an investment here.

Verdict

Analysts on Wall Street and Bay Street are an optimistic bunch. They expected $3.30 in EPS at the beginning of this year. Just look at how the estimates have evolved this year.

So, if you want to ride on that pony into 2025, be our guest. For our part, we see this as a gift chance to sell at such a high valuation. The best case is to collect a flat dividend for two years and Emera grows slowly into this valuation with zero price gains. The worst case is a 40% dividend cut, and Emera trades at a 12X multiple down the line. In case you find 12X too low, just go back and read about a growing utility with no risk to the dividend trading under that. We are moving Emera back to a Sell at this point.

Emera Incorporated Cumulative Preferred Shares Series A (TSX:EMA.PR.A:CA)

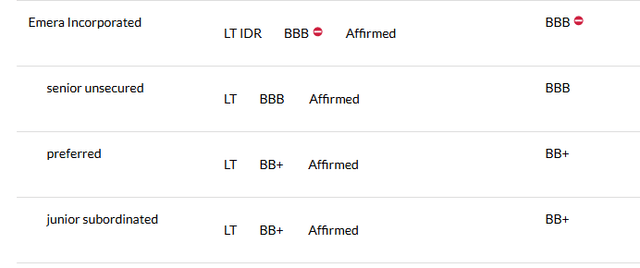

We always look at all layers of the capital stack to find investment opportunities. In the past, we have been cold on the Emera preferred shares, as the preferreds themselves are rated junk.

Fitch May 30, 2024 Outlook

Furthermore, on most occasions, the yield has not been too favorable relative to other choices. EMA.PR.A is still an interesting setup today. At present, it yields just a paltry 3.63% at its $15.00 price. But there is a reset coming in August 2025 at Government of Canada 5 year bond yield (GOC-5) plus 1.84%. Since the spread is one of the narrowest among the resetting preferreds shares of any Canadian company, this one will be highly linked to the GOC-5 itself. This might make sense for those who believe that the rate cut cycle may bottom earlier and at a higher level than what the market believes. Even at the current GOC-5 yields of about 3%, the preferreds would reset at 4.84% on par. That works out to about 8.06% on the $15.00 price. This is a lower risk play and one on our watch list.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here