It’s almost cliché to talk about buying quality stocks on pullbacks as a long-term winning investment strategy, but that has historically been a good strategy with stocks like Rockwell Automation, Inc. (NYSE:ROK). With the shares down close to 10% since my last update, and underperforming many peers including ABB Ltd (OTCPK:ABBNY), Emerson Electric Co. (EMR), Schneider Electric S.E. (OTCPK:SBGSF), and Siemens Aktiengesellschaft (OTCPK:SIEGY), while outperforming companies like Fanuc Corporation (OTCPK:FANUY) and YASKAWA Electric Corporation (OTCPK:YASKY), there is certainly an opportunity to consider this name as a “buy the dip” candidate.

And yet, I find myself reluctant to go fully positive on the name. I still see risks to the company’s growth outlook in FY’25, and I’d note that margin progress over the last decade-plus has actually been pretty minimal. At the same time, rivals like ABB, Emerson, and Siemens have been stepping up their game, and I’d note that the 2023 rally (after a significant decline from late 2021 to mid-2022) failed to top the prior peak. With valuation not suggesting an obvious bargain to me, I remain cautious even while aware that I may well someday have to write a piece talking about how I missed a rare chance to buy into the name.

End-Market Conditions Are Challenging…

Rockwell management has been lowering guidance throughout fiscal 2024 as the process of destocking at distributors and machine builders has taken longer than expected and, as I believe at least, end-market conditions have continued to deteriorate in many markets.

Management is now looking for mid-teens declines in its discrete and hybrid segments and flat revenue in its process markets for FY’24, and the updated guidance that management provided with fiscal Q3 earnings points to Q4 organic revenue down around 20%.

Many of the near-term drivers of weakness aren’t so surprising. Sales to auto customers were down at a high-teens rate in the last quarter, as not only have auto OEMs pulled back on EV-related capex (about half of Rockwell’s mix), but they’ve pulled back on overall capex in the face of softening demand. Likewise, a high-teens decline in the semiconductor market isn’t so surprising in the context of delays and push outs in new major fab projects.

Continuing on, food/beverage declines in the mid-teens look high relative to many companies in the space, but it’s important to remember that companies categorize their markets differently and a significant part of Rockwell’s food/beverage (around half, I believe) business is actually packaging. High-teens declines in life sciences seem reasonable given the weakness in life science research budgets and softer biopharma capex (something seen at companies like Agilent Technologies, Inc. (A), Danaher Corporation (DHR), and Thermo Fisher Scientific Inc. (TMO), and softening conditions in oil/gas, mining, and chemicals is broadly consistent with what companies like ABB, Emerson, and Honeywell International Inc. (HON) have seen (though Rockwell seems to be underperforming some in chemicals).

…And The Recovery May Well Be More “U-Shaped” Than Expected

What concerns me more, though, is that while expectations for a FY’25 recovery aren’t particularly sharp at present (consensus estimates work out to around 4% year-over-year growth), Rockwell could yet disappoint. Orders have been turning positive, but management has removed its guidance on the timing of clearing out channel inventory and many of the company’s peers have shifted their outlook for a recovery in discrete automation markets to mid-2025.

Looking at key markets, I’m concerned about the food/bev segment for Rockwell. This business contributes around 20% of revenue, and after a surge of capex spending tied to the pandemic, most packaging companies appear to be in a “digestion” phase, as companies like Greif, Inc. (GEF) have pointed to substantial declines in capex. Given that surge of past spending, I think Rockwell could be looking at end-market growth in the low single-digits for a few years here.

I’m also cautious about auto-spending. Notwithstanding Yaskawa’s commentary that they believe EV-related orders (from EU OEMs in particular) are sustainably improving, I think the auto sector could well see more moderate capex spending for at least the next 12 months. Chemicals (around 5% of revenue), are also likely to see relatively modest capex spending in FY’25 given recent capacity additions and softer commodity prices, and I’m not particularly bullish on tires or pulp/paper.

Where’s the good news? Biopharma/life sciences should start recovering next year, and I likewise expect better results in machinery and oil/gas. That’s around 20%-25% of the business mix, and I also expect a stronger recovery for semiconductors (another 5%). I also think e-commerce/warehouse will recover as 2025 rolls on, and I’m still fairly bullish on water and mining spending (as mining companies look to automate as a labor- and machinery-sparing alternative).

All in all, back-of-the-envelope math leads me to worry that growth in FY’25 could be more on the order of 2%-2.5% than 4%, and I do worry about operating leverage in an environment where revenue growth may disappoint management expectations.

An Impressive Technology Stack, But Where Are The Margins?

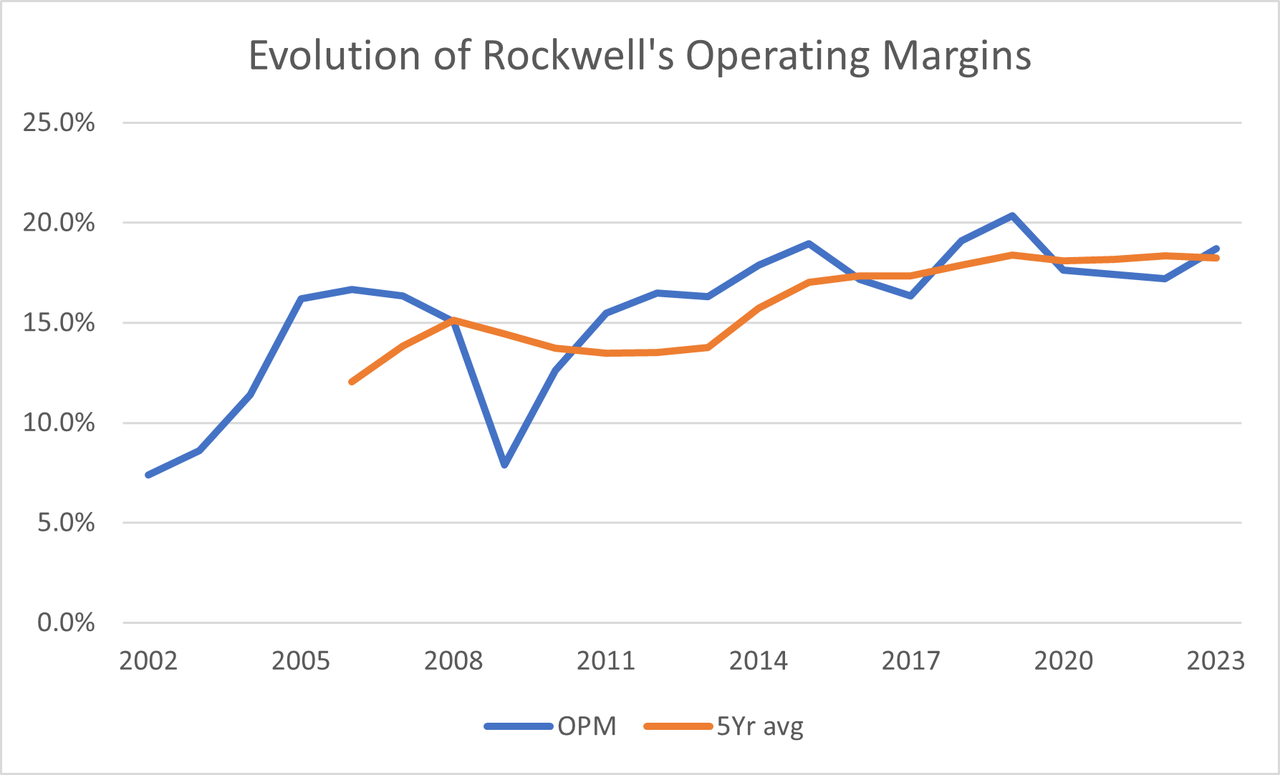

Speaking of operating leverage, one of my growing concerns about Rockwell is how operating margins have evolved over time. Assuming that FY’24 ends up somewhere around 17.6%, this will be the 14th straight year in the mid-to-high teens, with one year above 20%. That’s not terrible, and there has been an upward trend since 2005 (before which there was a sharp ramp), but given the pivot toward higher-margin software and controls, I’d have thought there’d be more margin leverage.

Stephen Simpson, w/ data from 10Ks

Bulls could argue that management has been managing margins to a target, and I think that’s fair. Rockwell has long enjoyed a premium multiple, and perhaps that has been allowing the company to spend more on R&D and business development than it otherwise would or could if it was focused solely on margin maximization. In any case, I do think this is something to watch, as margins do have a lot of influence on industrial stock valuation.

If Rockwell has, in fact, been trading margin for R&D, that spending hasn’t gone unrewarded. The company has an impressive presence in a lot of critical automation categories, including PLCs, drives, and controls, and has likewise built a strong software portfolio. More recently the company has been increasing its investments into robotics, one of the few areas in discrete automation where the company has historically not had much of a presence and where long-term growth potential is still quite attractive.

That said, Rockwell cannot afford to rest on its laurels, and I do wonder what that may suggest for future margin leverage. Emerson, Schneider, and Siemens have been stepping up their investments in areas like software and controls, and a restructured and improved ABB has likewise been improving itself. I’m not forecasting any “doom and gloom” here, but just pointing out that automation is an intensely competitive space where Rockwell’s legacy strengths may come under more pressure as the market evolves.

The Outlook

Despite Rockwell’s leadership in discrete automation, that hasn’t translated into blockbuster growth – the company has grown revenue at around 3% over the last 20 years and 3.5% over the last decade. I’m quite bullish on the long-term prospects for automation, but I can’t really argue for a long-term revenue growth much beyond 4% to 5% (in line with what I expect from most other automation players).

I discussed my margin concerns above, and a key question that I have is whether the company can break through the 20% operating margin (and low-20%’s EBITDA margin) to a new sustainably higher level. Free cash flow margins have improved from the high single digits (2008-2012) to the mid-teens (2013-2023), but haven’t taken that next leg up. With that, it’s harder for me to argue for long-term FCF margins much above the high teens, though improvement toward 17%+ over time can support over 7% annualized FCF growth.

Even with a lower discount rate that rewards Rockwell’s “best of breed” traits, I can’t get to a target that suggests more than mid-single-digit long-term annualized returns (versus a trailing 10-year average of about 10%). Looking at my margin/return-driven EV/EBITDA, even if I maintain the same 5pt premium that Rockwell has long enjoyed, that gets me to around an 18x multiple, or a $263.50 fair value on my 12-month EBITDA estimate.

The Bottom Line

If Rockwell looked substantially undervalued (I’d say 10%-plus is “substantial” for this company), I really wouldn’t worry about the near-term risks to growth expectations or the arguably sluggish progress of margin leverage. At more or less fair value, though, I’m concerned about the risk of further cuts to expectations, even as orders are starting to recover. I do like Rockwell as an enterprise, and I may well regret getting too finicky with valuation and entry price, but I’m still cautious right now, even though this is definitely high up my watch list.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here