Thesis

We last covered the PIMCO Enhanced Short Maturity Active Exchange-Traded Fund ETF (NYSEARCA:MINT) last year, when we assigned the name a ‘Buy’ rating and asserted the fund will deliver in an uncertain macro environment. The ETF most certainly has, with a total return in excess of 4.8% since our article. Some might call MINT boring, but we are of a different opinion. The fund delivers on what it tries to achieve, and does that in a linear fashion.

MINT falls in the short maturity bond funds category, and represents a robust cash parking vehicle. In this article, we are going to re-visit the name and articulate why we believe the fund is still a ‘Buy’ in today’s macro environment.

Boring delivers

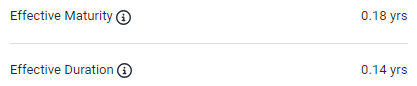

When investors look at cash parking vehicles, they should look for ‘boring’ names. Cash parking funds are aimed at squeezing out yield from the short end of the curve, and are meant to be steady yielders, not exciting moneymakers. MINT falls in that category, with a duration of only 0.14 years:

Duration (Fund Website)

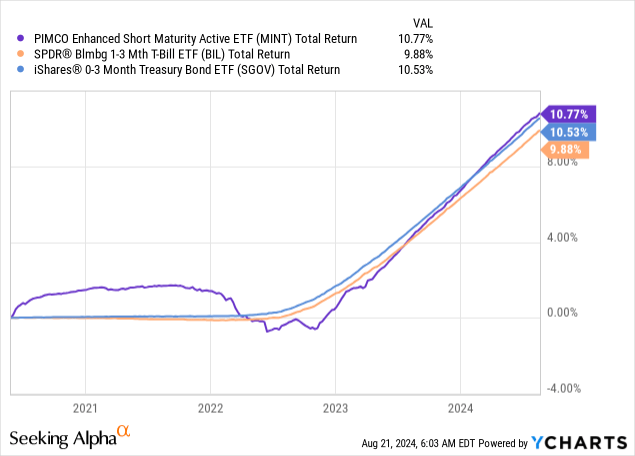

The fund contains mostly investment grade corporate credits and securitized debt, and has managed attractive total returns:

From the above chart, we can see how MINT has managed to outperform the SPDR Bloomberg 1-3 Months T-Bill ETF (BIL) and the iShares 0-3 Month Treasury Bond ETF (SGOV) in the past three years. While the fund does not take any notable duration risk, the name does not stick to risk-free treasuries, and contains mostly investment grade corporate bonds and securitized debt. In the next section of our article, we are going to see why this choice explains the outperformance posted by the fund.

Holdings – a mix of corporate bonds and securitized products

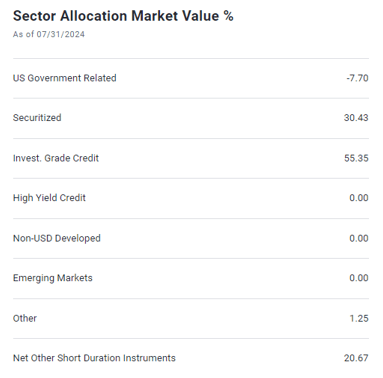

The fund invests in corporate bonds and securitized products rather than treasury bills or treasury notes:

Allocations (Fund Website)

Securitized debt represents 30% of the fund, while IG credit makes up 55% of the holdings. Although it does not focus on treasuries, the name does not take much credit risk as seen from its ratings parsing:

- AAA names: 15%

- AA names: 4%

- A names: 23%

- BBB names: 32%

- Not rated: 14%

- Short-term ratings: 12%

The high-quality holdings combined with a short maturity profile ensure the name does not suffer any credit related losses unless a three sigma event occurs (think the Lehman bankruptcy, with the bank rated A prior to its default). Even in a recession, the fund assets should mature before any real questions are asked regarding the probability of default for the held names:

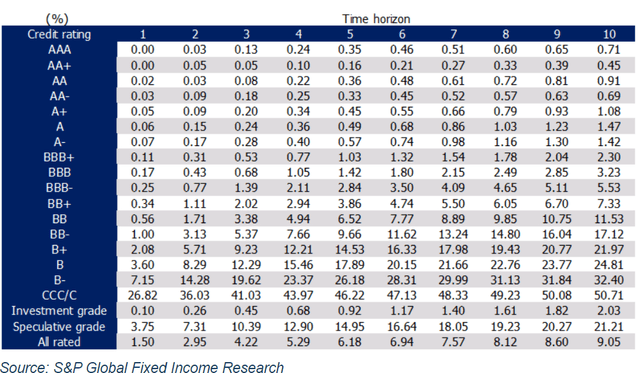

Probability of Default (S&P)

As we can observe from the above table courtesy of S&P, the shorter the time horizon and the higher the rating, the lower the probability of default. Keeping the MINT holdings above BB+ and with a very short maturity span of below 1 year ensures the probability of default associated with the respective assets is very small. Furthermore, ABS securities have embedded subordination triggers that switch on to de-risk the structure when defaults pick-up.

Although the nomenclature sounds complicated, ‘securitized products’ are purely ABS bonds, such as credit card receivables or auto loan securitizations. When banks want to lighten up their balance sheets, they can securitize certain assets and package them into SPVs that issue bonds. Funds such as MINT purchase these bonds at spreads above treasuries, but with minimal risks. ABS bonds are backed by asset pools, and the tranches bought by funds such as MINT are the most senior ones. Securitized products carry a spread to treasuries because they are not meant for individual investors, and they do carry a slightly higher risk via their complexity and structure.

What is going to happen after the Fed lowers rates

The market is now pricing a September 2024 Fed cut as a certainty; thus, Fed Funds are likely set to move lower. If and when the Fed cuts will have an impact on MINT. The fund achieves its low duration via a mix of floating rate securitized products and very short-dated bonds. While the fixed rate short-dated bonds will not be impacted initially, the overall yield in the space will. Upon maturity, the new bonds purchased by the fund will reflect the lower overall yields in the market.

Conversely, the SOFR debt held by the fund (securitized products reset based on SOFR) will feel the impact of lower Fed Funds immediately. One should expect to see a one-for-one impact from lower Fed Funds with a one-month lag (the re-set period for SOFR on most securitized debt).

While MINT will be affected by lower rates, do expect the name to outperform simple treasuries on the back of its holdings. Non-treasury holdings need to offer an excess spread to investors in order to be purchased. That excess spread is what the fund uses to outperform, and this space is the perfect example of correctly utilizing an asset manager’s capabilities in order to obtain a higher return.

Conclusion

MINT is a fixed income exchange-traded fund. The vehicle falls in the short term cash-parking vehicles category with a sub 1-year duration and investment grade composition. The ETF holds securitized products and corporate bonds that have a very low probability of default and a short duration. The fund has delivered very robust results in the past three years, given the excess spread versus treasuries captured by the name. With the Fed set to cut rates in September, expect a lagged effect and impact on MINT. However, the name will still benefit from the additional spread provided by its holdings versus simple treasury holdings. While some market participants might perceive the name as boring, we find MINT to be an ideal instrument for what it tries to achieve and are still at a ‘Buy’ for the name in the current macro context.

Read the full article here