In recent years, you won’t find many names that have done worse than cell programming and biosecurity company Ginkgo Bioworks (NYSE:DNA). The company has continued to miss lofty revenue growth targets, leading to its shares losing almost all of their value. Now that management is trying to turn things around and two major negative catalysts are behind us, it’s time to see if this company can finally get on track.

Previous coverage of the name

I’ve been bearish on this company for some time, as revenue troubles have built and large losses and cash burn have accumulated in recent years. In my latest article on the name, I detailed how Cathie Wood and her ETF firm Ark Invest were starting to sell their large holding of Ginkgo, a position that was nearly 11% of the company’s Class A shares outstanding. Since then, the flagship ARK Innovation ETF (ARKK) has completely sold out of its position, while the ARK Genomic Revolution ETF (ARKG) has almost done the same.

For a while now, I’ve also been talking about Ginkgo needing a reverse split to satisfy exchange listing requirements with shares under a dollar. That process has also been completed recently, with a 1 for 40 reverse split going through. Since my previous article, Ginkgo shares have lost another 40%, while the S&P 500 is up very slightly. In total, the stock is down more than 98% from the peak a few years ago after going public via a SPAC.

The recent Q2 report

A couple of weeks ago, the company announced its second quarter results. Total revenues came in at $56 million, which were well above street estimates, but still down about 30% year over year due to the decline in Covid testing. The main problem though was that Cell Engineering revenue came in at $36 million, down 20% year over year, driven by a decline in revenue from early stage customers partially offset by growth from large/enterprise customers. As I’ve continued to detail, this segment is supposed to be the company’s growth engine, and it’s just not happening right now.

The biggest issue for Ginkgo over the years has been its cost structure. Even before large restructuring charges were taken in Q2, operations lost over $158 million, more than twice the amount of revenue generated. The company announced a 35% reduction in its workforce during the period, with annualized savings expected to be at least $85 million by mid-2025. Unfortunately, there’s still a lot of red ink here, and some of those savings won’t help when it comes to cash flows. That’s because certain costs like stock based compensation were an add-back on the cash flow statement.

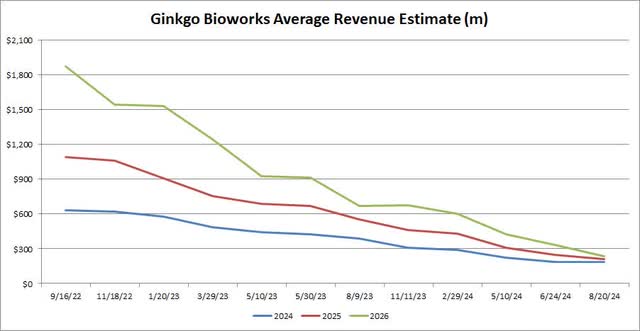

Management did reiterate its yearly forecast for revenues in a range of $170 million to $190 million. That’s a positive because it wasn’t a guidance cut this time around, but let’s not forget that the original forecast for this year was over $600 million (when the company was going public). As seen in the chart below, analyst estimates for this year and the next two continue to come down over time, with limited growth as compared to previous expectations.

Ginkgo Bioworks Revenue Estimates (Seeking Alpha)

Just in the past year, plus about two weeks, the average revenue estimate for the three-year period shown above has been more than halved to around $1.23 billion. Take a look at 2026, for example, where in a little less than two years the average estimate has gone from $1.87 billion to just $232 million. Even then, the company would still need to produce more than 25% growth over a two-year period.

Balance sheet continues to weaken

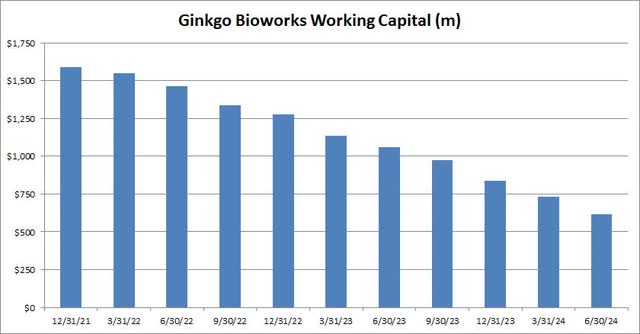

The one positive thing that this company has had in recent years has been its balance sheet. Unlike a lot of newer tech names, there isn’t a major debt pile here and Ginkgo has been sitting on a boatload of cash. Unfortunately, its large losses over the past few years have led to a lot of those funds being burned. At the end of Q2, total cash was down to about $730 million, with over $200 million burned in the first half of this year. That’s put a bit of pressure on working capital (current assets minus current liabilities) as seen in the chart below.

Ginkgo Bioworks Working Capital (Company Filings)

There’s still a lot of financial flexibility here, with working capital being about $617 million at the end of June. However, that number was down over $443 million in the last 12 months, and it’s not like cash burn is going to disappear anytime soon. While the company doesn’t need to go out and raise new funds right now, the balance sheet is getting weaker by the quarter, and that can limit what management does moving forward. Interest income also is coming down over time, which hurts the quest to reduce losses.

Valuation still doesn’t impress me

Even after its latest drop, Ginkgo shares still go for about 2.31 times their expected sales for this year. That’s a bit less than what the overall S&P 500 is trading at in the high 2s, but normally a biotech like this would go for a much higher multiple in the mid to high single digits. The problem is that there have been so many revenue estimate cuts, that you don’t know if you can really trust the current figures.

I am getting closer to upgrading to a hold based on valuation, but I need to see how all these layoffs play out over the next couple of quarters. We don’t yet know how much growth there will be in 2025, as the company focuses more on getting its expense structure in check. As I detailed in my previous article, the two biggest risks to the upside here are that management does get its sales trajectory back on track rather quickly, or that the low valuation results in a larger player in the space acquiring Ginkgo. I don’t think those are imminent catalysts at this point, however, so there could be more pain in store first.

Final thoughts and recommendation

The good news for Ginkgo Bioworks shareholders is that two major negative catalysts are now pretty much behind us. Cathie Wood and Ark Invest have sold almost all of their position, while the reverse split has been completed. The bad news here is that revenue estimates continue to come down, which is fueling negative sentiment in the stock. Moving forward, management is extremely focused on reducing its net losses and cash burn, but it remains to be seen if that will result in further cuts to revenue growth hopes.

For the moment, I am keeping my sell rating on the stock. While the valuation here has definitely improved, I need to see revenue estimates for the next couple of years level off before I can start to think about an upgrade. This company is a long way from where it thought its revenues would be by this point, and more losses and cash burn will increase pressure on the balance sheet in the near term. Perhaps at the next earnings report, if management can lay out some better projections for 2025, I can look at my rating again.

Read the full article here