At the Lab, we have a long history of Aegon (NYSE:AEG), but we should remind our new readers that this company provides life insurance, asset management activities, and pension solutions. Aegon was funded in 1880 in The Hague (Netherlands) and served more than ten countries, with critical operations in the UK and the United States. Indeed, our investment equity story was backed by 1) the Transamerica division’s upside, 2) a supportive Shareholders’ Remuneration, and 3) a sound management team with clear de-risking strategies ongoing. In detail, Aegon has undergone a restructuring under its current management team with the sale of Aegon Netherlands. This has rapidly improved the company’s ROE and its profitability in the US life business.

After a tumultuous start in August, markets have entered a quiet period. In the meantime, government bond yields have moved sharply in a short space of time. The critical near-term event is Jackson Hole, with expectations around the US Federal Reserve cutting cycle beginning in September. With a stock price performance of minus 8% since August started and the company’s H1 numbers released, this is an excellent time to review Aegon’s financials and expectations.

H1 Results

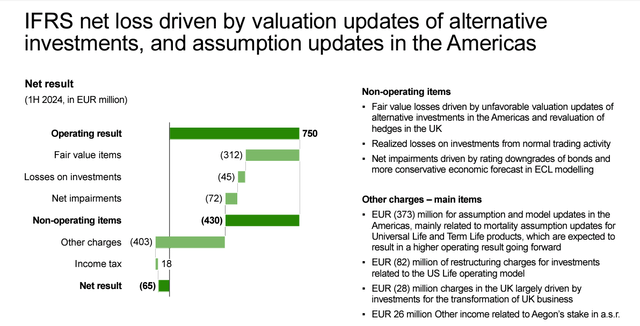

In the semester, the company reported an IFRS operating earnings of €750 million (Fig 1) and a net loss of €65 million. However, the net results were significantly impacted by minus €312 million of negative fair value items and minus €403 million charges due to changes in mortality assumption. Excluding these unfavorable one-time items, the result was almost aligned with Wall Street consensus estimates. That said, Aegon’s operating results were 8% lower vs. H1 2023. Consequently, the company shareholders’ equity decreased to minus 6%. This performance was supported by a positive evolution of the CSM release.

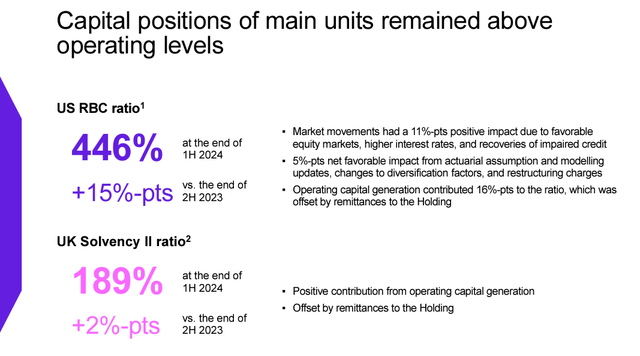

On the solvency ratio, the US RBC ratio was 9 basis points better than the consensus at 446% (Fig 2). This was supported by a positive credit experience due to higher-for-longer rates and favorable equity markets. On the group level, the solvency ratio reached an increase of almost 189% thanks to the company’s capital generation.

Aegon results

Source: Aegon Q2 results presentation – Fig 1

Aegon Solvency Ratio Evolution

Fig 2

UK Strategic Plan and our Optimistic Takes

(Looking ahead, we project a juicy capital return). Last time, we reported a positive evolution in Aegon’s tasty shareholders’ remuneration. As a reminder, following the completion of the €1.5 billion share repurchase plan, Aegon initiated a new buyback of €200 million. The interim dividend was also increased to €0.16 and was aligned with our expectations. That said, here at the Lab, we anticipate a minimum €300 million share buyback from 2025, which will be covered by HoldCo cash flow. In our view, with the current dividend yield projection in 2025, Aegon still offers an attractive capital return of at least 10%.

(Unlocking assets value). The company released a new strategic plan at the end of June. Having carefully analyzed the UK business update, we believe the company has shown a clear strategy to improve Aegon’s Workplace and Advisor platforms and their net flows. However, the high upfront transformation costs will likely not drive positive fundamental earnings changes in the upcoming years. Our division’s reduced earnings changes reflect lower operating profit over 2024 and 2025 due to a £70/80 million restructuring charge per year. That said, with the operating costs being absorbed by the UK business, the Group’s operational capital generation will slightly increase with higher holding cash flow in our forecast numbers. Even if we are not anticipating this scenario, we believe the market would react favorably if the CEO ever decided to dispose of the UK life business. Aegon focuses on building Transamerica’s new earnings capabilities to unlock shareholders’ value. This trend has been positive. Our team believes that ASR share sales might be the next positive catalyst, but the long-term ambition is a US IPO for the Transamerica division. In this regard, the top management team has an exceptional track record.

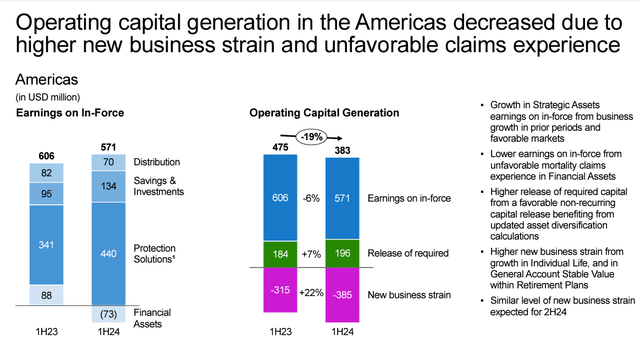

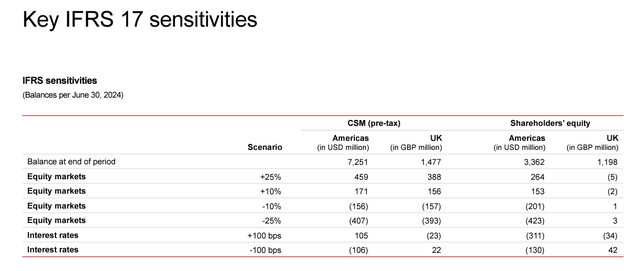

(Noteworthy ongoing results). According to Transamerica’s performance in H1, distribution and protection segments are growing strongly, with productivity improvements and increased market demand for the company’s products (Fig 3). Our team believes Aegon is on track to achieve the operational KPI target in this segment. In addition, compared to the past, Transamerica’s RBC ratio sensitivity to interest rates and equities has significantly decreased in recent years (Fig 4). This offers downside protection that cannot go unnoticed. Supportive new business strain and negative experiences in Financial Assets variances have impacted the performance. However, the company’s guidance of €1.1 billion remains unchanged.

Transamerica performance

Fig 3

Aegon Sensitivity

Fig 4

Adjusting Estimates and Valuation

Q2 earnings were not a relatively quiet quarter for the company. Here at the Lab, we slightly reduced our estimates to reflect Aegon’s UK Strategy Update. That said, we reiterate our overweight rating given the company’s attractive group capital return outlook and upside from potential disposal. In addition, we do not anticipate significant capital ratio loss from markets despite the implied volatility. With the company’s guidance unchanged and an H1 operating capital generation of €588 million, we were above the company’s outlook. In our previous coverage, we were forecasting a pre-tax operational income of €1.6 billion. This also included the a.s.r. dividend payment, which was fully paid in the quarter. With higher investment and transformation costs in the business, we decided to lower our operational income by €150 million. In addition, we estimate a lower Group Solvency ratio by five basis points. Including the positive accretion from buybacks with lower share counts, we lower our adjusted 2024 EPS estimates from €0.79 to €0.74.

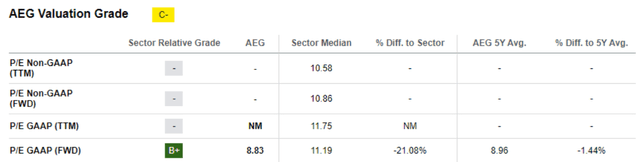

Regarding the valuation, we value it the same way as the rest of the sector and closest peers, such as NN Group. Continuing to apply an 8x P/E target (Fig 5), we arrive at a value of €5.92 per share. As a reminder, this 20% discount is aligned with Aegon’s past valuation and the MSCI Europe Insurance Index, which trades at a P/E forward multiple set at 10.3x.

Aegon SA Data Valuation

Fig 5

Risks

Our team has four years of coverage of Aegon. The main risks are included in the section below (Fig 6). In addition, we report: 1) execution risks on new business activities in the Transamerica division as well as higher restructuring charges in the UK division, 2) lower earnings projection due to unfavorable mortality claims, 3) higher release of capital from regulatory requirements or new business strain, and 4) lower buyback evolution. With Aegon’s international expansion and critical US and UK activities, the company might be impacted by FX changes.

Mare Ev. Lab Previous Risks Section

Fig 6

Conclusion

Despite the Q2 negative one-off, new business growth is supporting Aegon’s earnings progress. Ahead, we see downside protection from the company’s current asset base — related to disposal optionality. In addition, we see support from solid operating capital generation, which continues to offer an attractive capital remuneration policy. Our buy rating is then confirmed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here