I presented my bullish view on Workday (NASDAQ:WDAY) in my previous coverage in February 2024, highlighting their strong early renewal activities. The company released Q2 FY25 result on August 22nd, beating the market expectations. The headcount decline among Workday’s customers was moderating during the quarter. Workday anticipates mid-teen growth in their subscription revenue for both FY26 and FY27. I reiterate a ‘Buy’ rating with a fair value price of $300 per share.

Moderating Headcount Growth Among Customers

Workday lowered their full-year guidance in Q1 FY25 due to weak headcount growth among their customers. In Q2, the management indicated that the headcount decline began to moderate, which could be an early sign of market recovery.

I trust Workday will continue to deliver mid-teen growth in their subscription revenue in the near future. The key reasons can be summarized as follows:

- As indicated in my previous article, Workday holds a substantial market share in the HR market and is expanding into Finance sector. The Finance market is largely untapped market for Workday, and the company has made significant investments in this area, deploying AI technology into their platforms.

- During the earnings call, the management indicated that the company has been gaining market share in both HR and Finance markets. I have no doubt that Workday leads in technology and market share within their core HR market. The Finance is a fragmented market with many small competitors, and Workday’s HR and Finance platforms can better monetize their existing customer and leverage their internal sales team.

- The company are seeing more success across full suite opportunities including both HR and Finance platforms. The company added several customers with full suite including Clemson University, County of San Joaquin, and Presbyterian Healthcare Services.

Growth Projection and Valuation

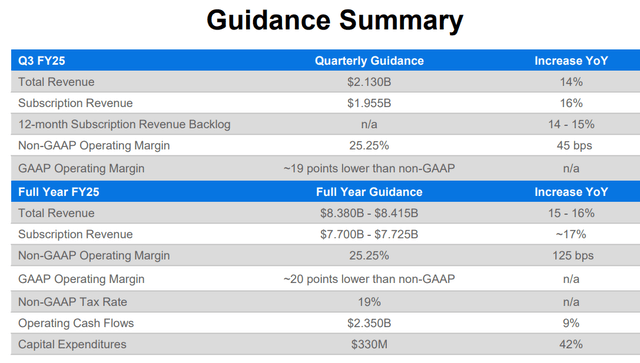

Workday is guiding for 15-16% revenue growth for FY25, and the guidance reflects the impact of weak headcount growth among their customers.

Workday Investor Presentation

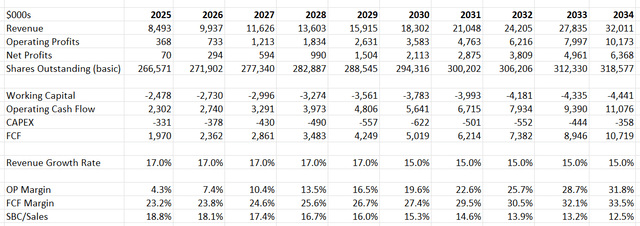

I estimate Workday will grow their revenue by 17% with the following assumptions:

- Grand View Research predicts the HR system will grow at a CAGR of 12.7% from 2023 to 2030, driven by the digitalization among enterprise customers. Workday has substantial advantages in the core HR market, and I forecast they will grow its core HR system by 12% annually.

- As discussed above, Finance is a new area where Workday is investing to drive growth. I anticipate Finance market will contribute an additional 3% to the overall topline growth.

- Lastly, I assume pricing will add another 2% to the overall revenue growth, aligned with the historical average.

Workday only earned 2.5% operating margin in FY24, due to heavy investments in R&D and Sales & Marketing. When the business scales, I forecast the operating margin will gradually expand to 31.8% by FY34. Key drivers are:

- 50bps margin expansion from gross profit due to pricing and new solutions in Finance

- 120bps operating leverage from sales and marketing. Workday has the opportunity to leverage their sales team to distribute various platforms.

- 100bps operating leverage from R&D expenses.

- 40bps leverage from general and administrative expenses.

DCF summary:

Workday DCF

The WACC is calculated to be 12% assuming: risk free rate 3.8% ((US 10Y Treasury)); beta 1.52 ((SA); equity risk premium 7%; cost of debt 7%; debt $3 billion; equity $8 billion; tax rate 19%.

Compared to my last DCF model from February 2024, several changes have been made:

- As Workday has not been active for acquisitions over the past two years, I don’t assume any contributions from acquisitions in the current DCF model. In other words, the growth rates in the model are entirely organic.

- With no acquisitions assumed, I estimate the operating expenses will grow by 10%-14.8% in the future, leading to a 31.8% operating margin by FY34.

- Lastly, the discount rate has changed from 10% in previous model to 12% here, reflecting changes in the stock’s beta, risk free rate and equity risk premium and updated balance for equity and debts.

Discounting all the future FCF, the fair value of Workday’s stock price is calculated to be $300 per share.

Downside Risk

As part of Workday’s strategies, the company is expanding their services into international markets, particularly in Asia Pacific and Europe. Remarkably, their international revenue grew by 18% during the quarter. While I think the international market expansion makes strategic sense, it might affect Workday’s overall operating margin due to early investments required in these new markets. In addition, Workday lacks sufficient experiences to operate as a truly global company.

Conclusion

I think Workday remains a structural growth company driven by both core HR and new Finance platforms. It is encouraging to see the headcount decline among their customers is moderating. I reiterate a ‘Buy’ rating with a fair value price of $300 per share.

Read the full article here