Since I initiated a ‘Strong Buy’ rating on Lockheed Martin (NYSE:LMT) in January 2024, the stock price has surged by more than 30%. In my initiation report, I discussed Lockheed Martin’s growth driven by escalating global conflicts. The company released its Q2 result on July 23rd, reporting an 8.6% year-on-year growth in revenue and raising full-year guidance. I think their recent acquisition of Terran Orbital is value accretive to shareholders. I reiterate a ‘Strong Buy’ rating with a fair value of $600 per share.

Strong Demands for Defense Technology Solutions

My biggest takeaway from Q2 is the strong growth in backlog, which has achieved around $160 billion in total. The strong backlog underscores a very strong demands for defense technology solutions, propelled by escalating geopolitical tensions.

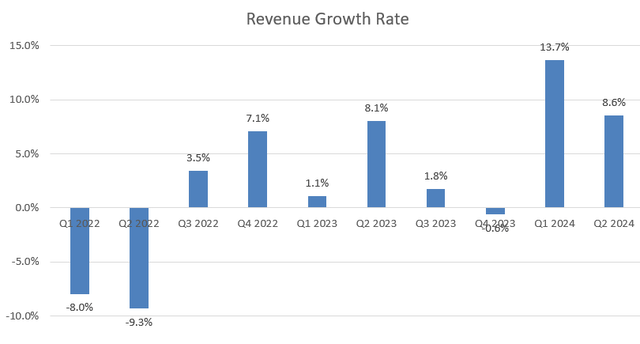

As a result, Lockheed Martin delivered 8.6% of topline growth with 20bps margin expansion for the quarter, as depicted in the chart below.

Lockheed Martin Quarterly Earnings

I think there are several major catalysts for the company’s growth in the near future:

- On July 19th 2024, Lockheed Martin disclosed that they started to deliver the first Technology Refresh 3 ((TR-3)) configured F-35 aircraft to the U.S. government. As communicated by the management, TR-3 and Block 4 represent itical advancements and are expected to contribute substantial growth to the company. As indicated over the earnings call, Lockheed Martin will produce 156 aircrafts per year and deliver 75 to 100 aircraft in the second half of 2024.

- Lockheed Martin’s PAC-3 program continues to gain growth momentum in international markets. For PAC-3 revenue, the management expects to achieve $550 million by FY25 and $650 million by FY27. I think all the partnership and contracts the company has secured will drive the future growth of their PAC-3 missile program.

- Lockheed Martin has made significant updates to both hardware and software of their F-35 program. With these major updates, the company expects demands for the F-35 to exceed production levels over the next few years, indicating a very strong growth head.

Recent Acquisition of Terran Orbital

On August 15th, Lockheed Martin announced to acquire Terran Orbital for $450 million in enterprise value. Terran Orbital is a global leader providing satellite-based solutions primarily supporting the aerospace/defense industries. I favor this deal for the following reasons:

- Both companies serve similar customers in the aerospace/defense industries. The acquisition could potentially leverage Lockheed Martin’s existing distribution channel and internal sales force, potentially generating revenue synergies.

- Lockheed Martin has collaborated with Terran Orbital over the past seven years on a variety of successful missions. As such, Lockheed Martin is well-acquainted with Terran Orbital, which should help minimize integration risks.

- Lockheed Martin is Terran Orbital’s largest customer currently. As such, the acquisition could better integrate Lockheed Martin’s supply chain, potentially reducing operating costs.

Outlook and Valuation

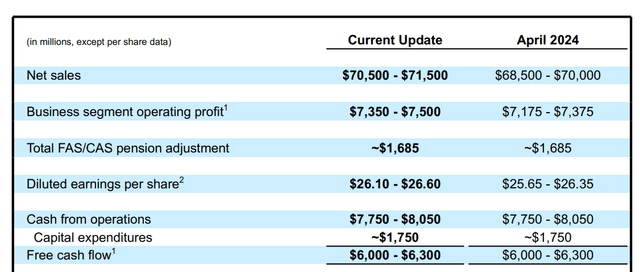

Due to the strong quarterly results, Lockheed Martin raised the full-year guidance for both revenue and operating profits, as detailed in the table below:

Lockheed Martin Investor Presentation

Due to the restart of F-35 program, I have revised the growth assumptions in my DCF model as follows:

- Aeronautics: I anticipate Aeronautics business will maintain the growth momentum, delivering 4% organic revenue growth in FY24. The growth will be primarily driven by high volume of F-35 and product ramp-up of the F-16 program.

- Missiles and Fire Control: Due to Lockheed Martin’s international expansion and increasing geopolitical tensions, I forecast Missiles and Fire Control will grow its revenue by 7%.

- Rotary and Mission Systems: Lockheed Martin has been growing their warfare systems and sensors on radar and laser programs over the past quarters. I expect this growth momentum to continue, leading to 7% organic revenue growth.

- Space: I assume the segment will grow by 3% in revenue, aligned with historical average.

As such, I calculate that Lockheed Martin’s organic revenue growth will be 5% in the near future.

Additionally, I assume the company will allocate 5% of revenue towards acquisitions, contributing 130bps to the overall topline growth.

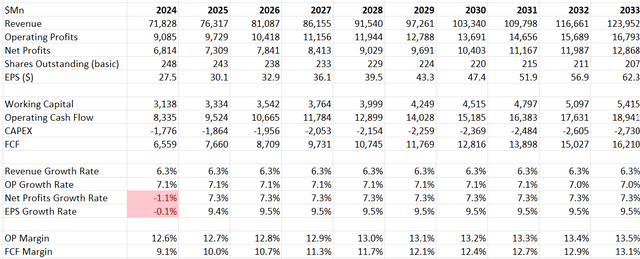

I model 10bps margin expansion in the DCF model, primarily driven by operating leverage of sales and marketing, as well as G&A expenses. With these parameters, the DCF summary can be found below:

Lockheed Martin DCF

The WACC is calculated to be 7.3% assuming: risk free rate 3.8%; cost of debt 7%; equity risk premium 7%: beta 1; equity $6.8 billion; debt $17.4 billion; tax rate 16%.

The fair value is estimated to be $600 per share, according to my DCF model.

Downside Risk

The FY25 U.S. defense budget has been approved by the House in March 2024, allocating $825 billion to the Defense Department, around $29 billion more than what Congress enacted in 2023. The U.S. defense budget now awaits approval from the Senate later this year. It is unclear whether the Senate will pass the budget or requires revisions. The outcome might have some short-term impact on Lockheed Martin’s stock price.

Conclusion

The restart of the F-35 program and the implementation of TR-3 and Block 4 could potentially accelerate Lockheed Martin’s business growth in the near future. It is evident that Lockheed Martin is well-positioned to benefit from intensifying geopolitical tensions. I reiterate a ‘Strong Buy’ rating with a fair value of $600 per share.

Read the full article here