The Smith & Wesson Investment Thesis

Seeking Alpha

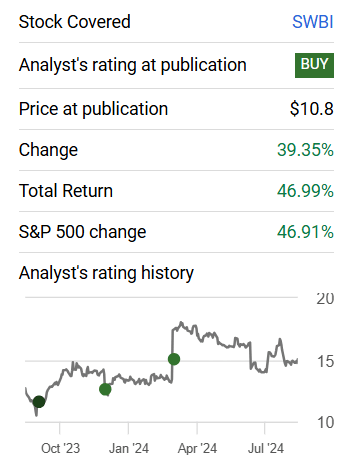

I wrote my first article on Smith & Wesson (NASDAQ:SWBI) in March 2023, and since then, the stock has returned almost exactly the same as the S&P 500 (SPY). Both are up 46% during a period when Smith & Wesson has struggled with high costs due to its headquarters relocation.

And I continue to believe that it is only now, after the relocation, that shareholders may be rewarded for their patience. The upside potential over the next five years is approximately 100% according to my EPS estimate.

Smith & Wesson’s FY24 Results

In my last article on Smith & Wesson, I predicted that Smith & Wesson would report FY24 revenues between $520 million and $535 million. Fortunately, they hit the high end of my range, coming in at $535.8 million.

This represents an increase in net sales of 11.8%, or $56.6 million, in a difficult year, which is a strong accomplishment by the management team. The gross margin was slightly lower than in FY23, 29.5% versus 32%, but EPS and net income were higher, so the results are still satisfactory. However, there are opportunities to improve margins in the coming years through operational improvements once the stress of the move has subsided.

Unfortunately, the market did not take well to the news that demand will be weaker than expected in the near term, leading to a modest sell-off. However, the upside potential for FY25 as a whole, including the elections and their potential impact, should be relatively high, offsetting the weaker-than-expected Q1.

Smith & Wesson is therefore likely to stockpile for this eventuality and be prepared for a high level of demand.

SWBI’s Capital Allocation

SWBI 10-K FY24

My original thesis was that Smith & Wesson, normalized after the relocation, would have about $80 to $100 million of FCF available to distribute to shareholders. This relocation plan, announced in September 2021, has so far cost more than $150 million in FY23 and FY24. But the big costs seem to be over, and if there are any in FY25, they will be smaller amounts.

But as you can see in Q4/24, where SWBI almost tripled FCF compared to Q4/23, $38 million versus $13 million, the use of capital already seems to be more effective. While Q4 is typically the quarter with the best FCF, I think an estimate of $20 to $30 million of CapEx for the full year and $100 to $110 million of operating cash flow for FY25 could be realistic. That would be roughly in the $80 million to $100 million FCF range.

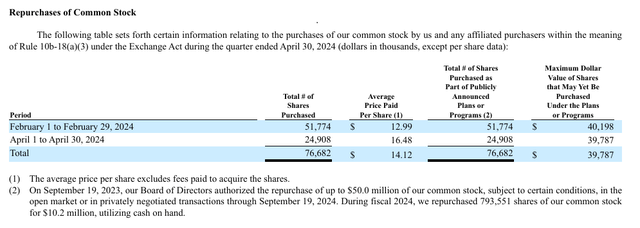

In FY24, $22 million was paid in dividends and $10.2 million in share repurchases. In total, more than $30 million was returned to shareholders. And in FY25, I hope to see something between $40 million and $45 million, the majority of which I would like to see used for share repurchases.

SWBI 10-K FY24

For the $10.2 million share repurchases made in FY24, 793,551 shares were repurchased and an additional $39 million is available under the repurchase program. Depending on the prices at which these shares are bought back, I assume that it will be about 2,500,000 to 3,000,000 shares.

SWBI 10-K FY24

Unfortunately, the $10.2 million did not result in a significant reduction in shares outstanding, as it only offset the dilution from SBC. As in FY23, the weighted number of shares outstanding remains at approximately 46 million.

But I expect the share buybacks to be larger than the SBC in FY25, which will reduce the share count. Ideally, a reduction of a little more than 1 million shares per year over the next 5 years to get the shares outstanding down to 40 million would be very supportive of total returns in my opinion.

I believe that by standardizing processes, SWBI can improve its margins and achieve solid growth without having to make extremely large investments.

SWBI’s Balance Sheet

SWBI 10-K FY24

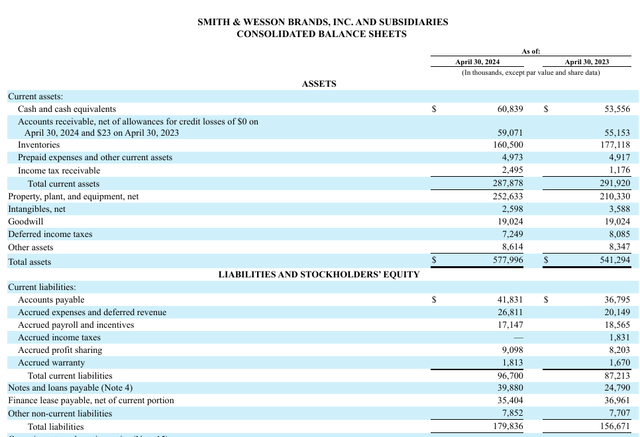

Smith & Wesson has a solid balance sheet with no long-term debt on the balance sheet, but they do have $40 million of borrowings outstanding on the revolving line at an interest rate of about 7.18%. But they also have $60 million in cash, so repaying the borrowings should not be a big problem.

Accounts receivable and accounts payable are up, so we should look at days sales outstanding and days payable outstanding to get a better picture of capital efficiency. And here we have an encouraging development because DSO went from 50 in FY20 to 39 in FY24, which means Smith & Wesson is getting paid faster. And DPO went from 47 in FY20 to 40 in FY24, which means vendors are also getting paid a little bit faster. But all in all, Smith & Wesson’s customers are paying faster than Smith & Wesson has to pay its suppliers. A positive sign.

In addition, suppliers have no real pricing power because Smith & Wesson has primary and secondary sources for every critical part it does not manufacture.

Smith & Wesson’s Valuation

Smith & Wesson is currently in a position where it has the potential to expand its margins, become a share cannibal, and grow net sales slightly each year. Therefore, in my 5-year plan, I would assume the following numbers. Net income margin expansion to 10%, share count decline to 40 million, and sales growth of 4% at an exit P/E multiple of 18x.

Starting revenue: $535m Price: $15

| Revenue in 5 Years | $651m |

| Net Income | $65,1m |

| Shares Outstanding | 40m |

| EPS | $1.63 |

| Multiple | 18x |

| Share Price 5Y | $29,34 |

| Upside | ~96% |

A 96% upside, with dividends on top of that, on only 4% revenue growth is a strong outlook in my opinion. And I expect dividends to continue to rise over the next few years, which could significantly increase the total return.

My hurdle rate is always a 100% upside over 5 years, and I think that in this case it is given with relatively conservative assumptions.

Conclusion

I think Smith & Wesson is still attractively valued and has a lot of upside. However, it will be important to keep an eye on SBC costs and see how management deploys FCF this year. I think FY25 could be critical here to see where the journey goes in the coming years.

Read the full article here