Thesis

On March 21, 2024, Reddit (RDDT) went public. Traders and meme stock enthusiasts were drawn in to arguably the highest profile IPO of 2024. At the time of writing, the market cap of RDDT is over $10 billion, with more than a quarter billion dollars’ worth of stock exchanged on a daily basis. Investors are attracted to the growth opportunity that comes from highly engaged communities and authentic user-generated content. Quality interaction and moderation are hallmarks of the business, which are only increasing in value in the age of AI/ML. There is a microcap company with a similar edge in social media and what, I think, is an even more attractive valuation and growth profile. (TSX:FORA:CA) trades on the Toronto Stock Exchange and is currently valued at $195 million. It also trades in the OTC markets as (OTCQX:VFORF). I rate it a Strong Buy for several reasons. There’s a lot to like about Reddit fundamentally, especially its strong revenue growth. It is, however, FCF negative, and until RDDT reports reliable FCF, I don’t want to own it. I also believe U.S. investors may overlook some of the value that can be found on the Toronto Stock Exchange, so I am interested in diversifying my portfolio into Canadian companies at this time. News of a NYSE or NASDAQ listing would be a momentous event for FORA.

Social Media Edge

Like RDDT, FORA is a digital platform for passionate people to connect and share information on mutual interests. Some of FORA’s popular community forums focus on cars, hobbies, and consumer products. Although unknown to many investors, FORA is quite large. It has over 120 million monthly active users according to the latest earnings report. For an apples-to-apples comparison, as RDDT only reports daily and weekly active users, I assume FORA has around 33 million daily active users. RDDT reported 91.2 million daily active users on its last earnings report. Looking at these numbers, you can see that RDDT has only 3x the daily active users and yet commands a market cap around 50x that of FORA. Being a user of both platforms, I can say the quality of content is comparable if not better on FORA when compared to RDDT. Very specific, user-generated nuggets of information are available to anyone with an internet connection.

The business model is attractive to me because it is a user-generated content model where the consumers are also the producers. Many media platforms rely on paid content creators, and platforms like TikTok have pivoted to an e-commerce focus, where product reviews face the issue of bias and reliability, as they are often generated by the vendor. Unlike these platforms, it is rare for a FORA contributor to receive compensation. FORA is exploring the e-commerce space, but the lionshare of revenue comes from advertising. Users compile their authentic personal experiences to inform one another, and unlike RDDT which has sub Reddits, FORA is a collection of separate websites, each catered to its own audience. The websites follow a consistent layout, powered by the proprietary FORA platform, making it easier for users to navigate various topics on the platform while reducing the overhead expenses and risks of publishing a single website. The potential to license the technology and further build an archipelago of sites, rather than one monolithic database, is another key differentiator that I like from a business development and growth standpoint.

Healthy Free Cash Flow

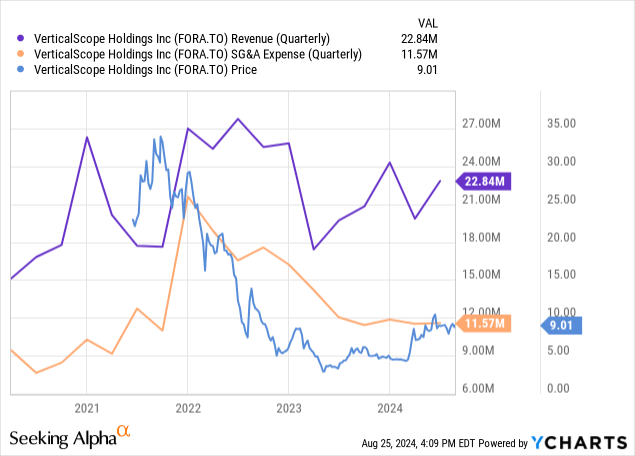

FCF for FORA looks quite good relative to its market cap. With the attention this stock deserves, I believe investors will realize that this stock is significantly mispriced. From June 2023 to the same month of this year, quarterly unlevered FCF grew approximately 26%. TTM unlevered FCF is $21.4 million. With just 21.6 million shares outstanding, FCF per share is $0.99 and FCF yield is 10.7% according to Seeking Alpha data. Both levered and unlevered annual FCF have been positive for five consecutive years. The strong FCF reflects the company’s success managing working capital and keeping capital intensity light. Having developed its algorithm for new websites, FORA is prepared to scale with minimal incremental investment. TTM revenue is $64.8 million, while total PP&E is valued at just $2.4 million, giving a capital intensity ratio of around 3.7%. This number would look a little higher if intangible assets and IP are included. The key driver of positive FCF for FORA seems to be management’s ability to control costs and improve margins. As shown below, SG&A expenses have declined as revenue has ranged from around $18 million to over $27 million.

Data from YCHARTS

Although revenue growth has been unremarkable, if anything a bit volatile over the past few years, it hasn’t declined in the same way share prices have. 87% of Q2 revenue was generated from advertising, and 13% was from e-commerce. 2/3 of the advertising is from programmatic or automated sales and 1/3 of the advertising is from direct sales. Most users live in the U.S. There is quality revenue behind the strong FCF. Revenue variance is likely due to various user acquisition campaigns and cost-cutting measures to improve margins, rather than any organic factor.

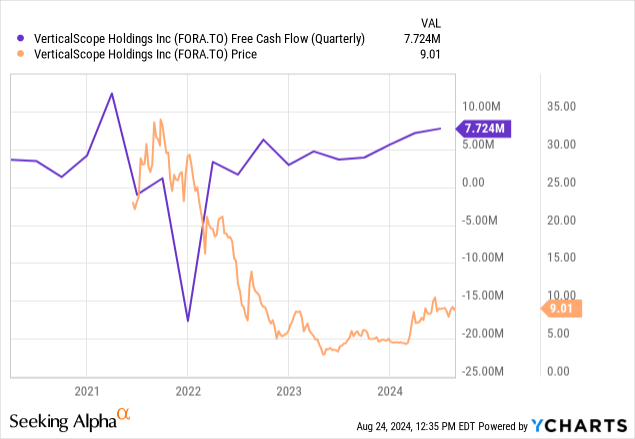

When compared to RDDT, FORA looks much healthier from a FCF perspective. RDDT is FCF negative for two consecutive calendar years. The negative FCF of RDDT does not reflect any large investments, meaning that RDDT is losing cash from its operations in several consecutive years by not controlling costs and working capital in the same way that FORA is. RDDT’s cash burn is especially unattractive to me considering the recent IPO. Although RDDT is generating linear revenue growth, it is burning cash, which suggests further debt and dilution down the road. It also makes RDDT look less stable as a company, despite having more active users. Being FCF positive, FORA is led by a management team and board that create shareholder value in a way that RDDT has not.

Data from YCHARTS

Compelling Valuation

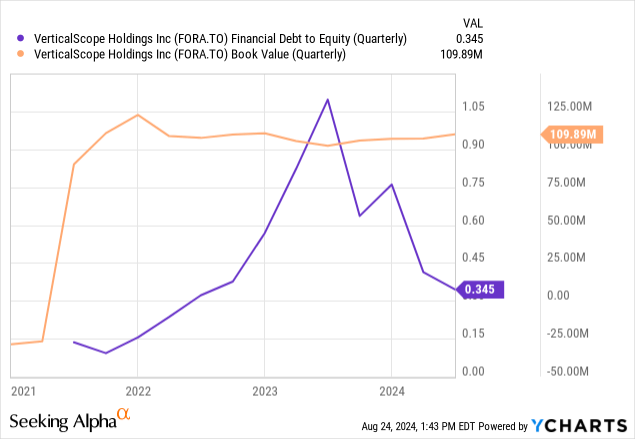

Priced at around 9.1x unlevered FCF, FORA looks very good to me. Despite maintaining positive FCF for quite a few quarters and several years, FORA share prices, as shown below, have slumped, and I cannot see a reason for this. Shares outstanding have grown some, so dilution is a possibility, but the valuation still looks low, and perhaps the stock has over-corrected in response to growth in the float. The book value per share has grown as well. Equity per share of FORA is $3.72, so it trades modestly at around 2.4x book value given its healthy FCF. RDDT has a book value of $11.43, which is only about 3x FORA, despite its market cap being about 50x. Driving the increase in book value is the company’s ability to pay down debt and retain its cash flow. The chart below shows book value steadily growing to a plateau and debt/equity decreasing rapidly since Q2, 2023. This rapid decrease in debt/equity is certainly a positive, but it does come with the increase in the float.

Data from YCHARTS

Risks

There are several noteworthy risks to opening a long FORA position. RDDT seems to have a stronger brand and better name recognition. FORA and RDDT will compete for organic search results, and I believe that brand recognition will play a role in which website ranks higher organically and receives clicks, ad impressions, and revenue in turn. The fact that FORA already has a substantial fraction of the monthly active users mitigates this risk, although the size of this platform is strange to me because I must admit, I had never heard of FORA before it came on my radar as an investment opportunity. I do like FORA’s niche in non-promotional, user-generated product experiences, tips, and reviews, while RDDT has a longer tail of small, old, or irrelevant forums. I would like to see more growth and less volatility in FORA’s revenue, as I believe RDDT’s growth is somewhat secular to the user-generated content model and FORA should be growing and monetizing users in a similar manner. If FORA can save money on its programmatic advertising by converting advertisers into direct buyers, then I think FORA has a path to stable revenue growth, less churn in advertisers, and overall less costly targeting. They could alternatively begin to license the technology or raise prices on their new ad-free options, which cost less than $5/month. Lastly, share prices have below-market volatility with a 24-month beta of 0.74 despite liquidity challenges evidenced by a 3-month average daily volume of 29,851. On an average day, less than $500,000 of stock trades, so RDDT does have superior liquidity.

Conclusion

I am confident that FORA is a better investment to capture the secular demand for user-generated content, and I am bullish on this model. I tend to favor FCF positivity as a value investor, and RDDT’s losses, as measured by FCF, exceeded $50 million in the calendar year 2023. Because it has a model similar to FORA, RDDT should have scaled its platform and gained margin as FORA has if it were growing organically. RDDT does have relatively high short interest at 8.23%. RDDT is the haven of short-squeezing, meme stock traders whose affinity for the platform points to explosive upside for RDDT. As a value investor, I like RDDT but love FORA. With FORA, I am simply seeing a better Sharpe ratio. This piece reflects my honest market outlook on August 26, 2024, and is subject to change, revision, or follow up to be published exclusively on Seeking Alpha.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here