Investors are taking Fed Chairman Powell’s comments from Jackson Hole last Friday around it is now time for monetary policy to ‘adjust‘ in the most positive light. However, this is akin to going to a chiropractor that has performed many adjustments in error (EK, inflation is ‘temporary‘ and ‘transitory‘, after adding 40% to money supply in two years during the pandemic) in the past and hoping this adjustment allows one to walk with absolutely no pain, instead of one that ends up crippling you.

That said, the only question now is whether it will be a 25bps or 50bps cut at September FOMC meeting. I am hoping the former as a 50bps rate reduction smacks of desperation, and probably means the labor market is quickly deteriorating.

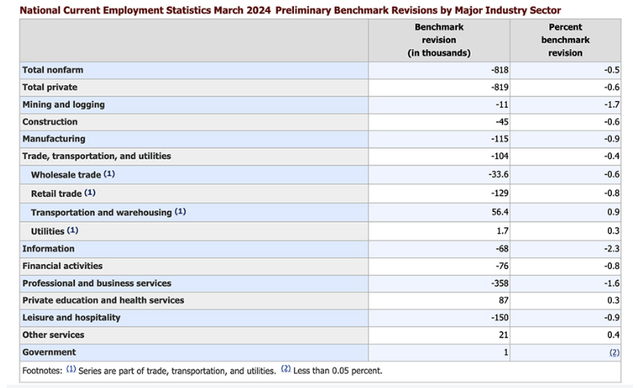

Bureau of Labor Statistics (BLS)

This is going to make the August BLS jobs report that comes out just before the bell on Friday, September 6th must watch TV for investors. This is especially true after July’s dismal BLS jobs report and after the BLS whacked their previous estimate of 2023 job creation down by 818,000 positions last week. This was the second-largest revision in BLS history, topped only by 2009 when the country was going through the Great Financial Crisis. If the August jobs report meets expectations, it is likely we will see a 25bps reduction less than two weeks later following the FOMC meeting. If the BLS reading disappoints again, a 50bps rate cut is fully on the table and the most likely outcome.

Modest Economic Impacts:

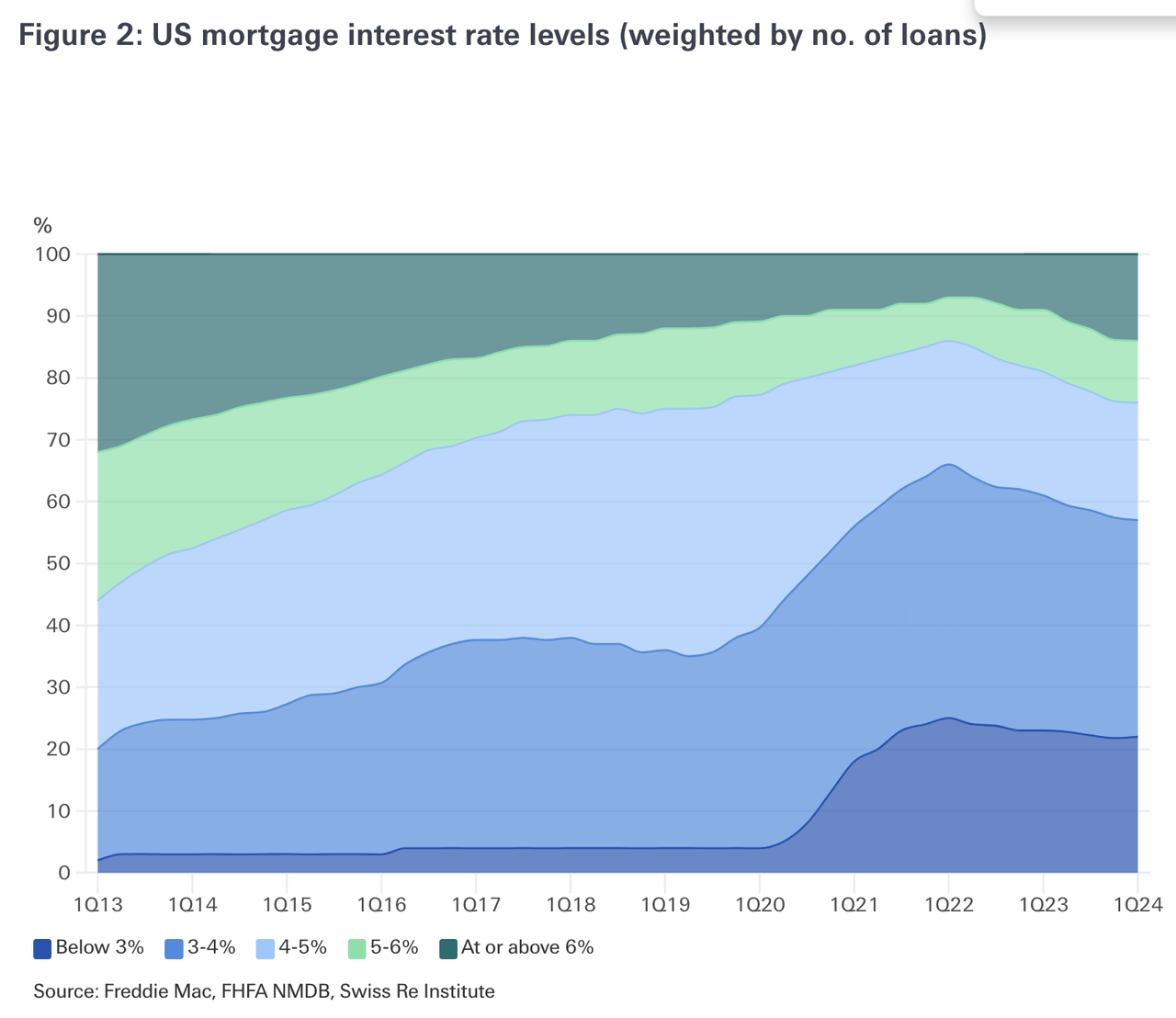

The first cut to the Fed Funds rate is likely to have a marginal impact at best on the economy. A slight reduction in average mortgage rates will do little to help boost sales of existing homes, which fell a whopping 16% on a year-over-year basis in July. New home sales rose 10.6% in the same month, pointing to the fact that current homeowners that are very reluctant to give up their three and four percent mortgage rates unless they have to or get an offer they can’t refuse. Fannie Mae was out early this week predicting home buying in the U.S. ‘will remain sluggish until a combination of stronger income growth and lower mortgage rates – closer to 6% – helps restore affordability in the housing market.’ Home builders will get some marginal help as slightly lower mortgage rates will reduce the costs and frequency of ‘incentives‘ they are using to move inventory, like mortgage rate buy downs.

Freddie Mac, FHFA, Swiss Re Institute

Slightly lower interest rates will also have little impact on commercial real estate, especially on the office sector where assistance is the most needed. Let’s take an example of a property owner that bought an office building for $500 million in a major city like Los Angeles, San Francisco or New York City in 2018 or 2019. It was 95% leased and the new owner put 30% down and financed the rest at five percent on a five-to-seven term loan. The building threw off healthy annual cash flow on these terms.

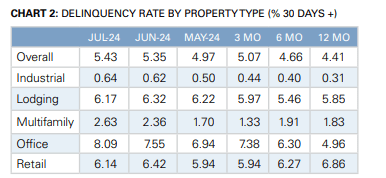

CMBS Delinquency Rate By Property Type – July 2024 (Trepp)

Fast-forward to 2024 and that term loan is up for renewal in the coming quarters. Thanks to the explosion in the virtual workforce, the building is now only 75% leased. Combined with an explosion in other building costs (insurance, utilities, maintenance, personnel, regulatory, etc…), the property is losing money every month even with a low-interest rate on the existing debt. In addition, the value of the building has been halved, completely wiping out the owner’s equity. Will the ability to refinance that debt at 9% or even 8%, compared to 10% before interest rate cuts make any difference to the owner of the building? Lenders might continue to be willing to play ‘extend and pretend‘ for some quarters. However, both delinquency and default rates should continue to rise at least through 2025 even if the Federal Reserve cuts rates significantly over the next four or five quarters.

Ignore History At Your Peril:

Those who cannot remember the past are condemned to repeat it.” — George Santayana

I thought after the massive pain that the Great Financial Crisis inflicted on the economy and equities, investors would not be so quick to dismiss history when making their investment decisions going forward. I was wrong. Miami, which was one of the epicenters of the housing crash that started in 2007, once again is the Wild West from a real estate standpoint. There are more than 90 skyscrapers over 40 stories currently going up between Coconut Grove and midtown Miami. The massive construction cranes that dot the Miami skyline puts the housing boom of 2004-2007 to shame as the tallest structures south of New York City rise.

I would really like to believe the Federal Reserve will achieve a ‘soft landing‘ in the quarters ahead. My portfolio certainly does better when stocks are going up or flat than when equities are declining, after all. However, I just can’t ignore history. And the fact is the central bank has only ushered in one true soft landing in my 57 years on this earth.

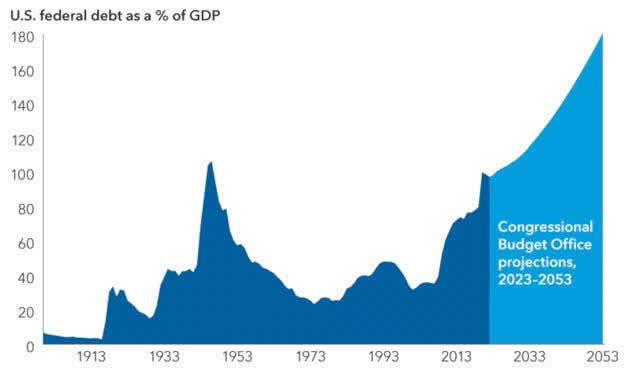

CBO/Capital Economics

That was in 1995 when many things were much supportive of that scenario. The huge Baby Boom demographic was in its prime earning years. The national debt was less than $6 trillion and the federal budget was more or less in balance. The Cold War had recently been won and there was a ‘peace dividend‘ to be spent in a unipolar world. In addition, the Internet Boom was in its early innings that would see the U.S. average more than four percent annual GDP growth from 1996 through 1999. None of those conditions exist today.

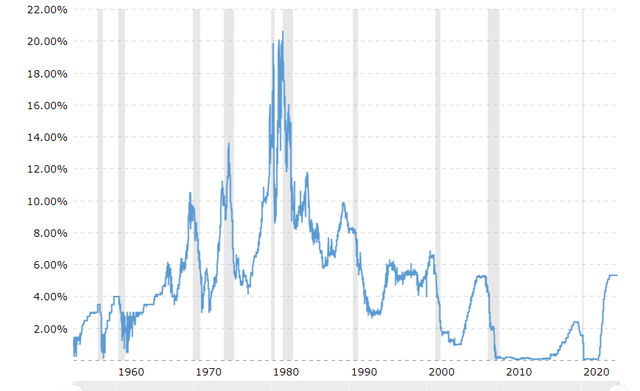

Fed Funds Rates (Macrotrends)

In addition, the last two times the Fed has most recently started to cut interest rates from over 5% levels (September 2007, January 2001), the end result hasn’t been pretty for the markets. In addition, the only other time the yield curve has been inverted continuously for a longer duration than currently, ended in 1929. To dramatically understate things, this also did not end up well for the markets or investors.

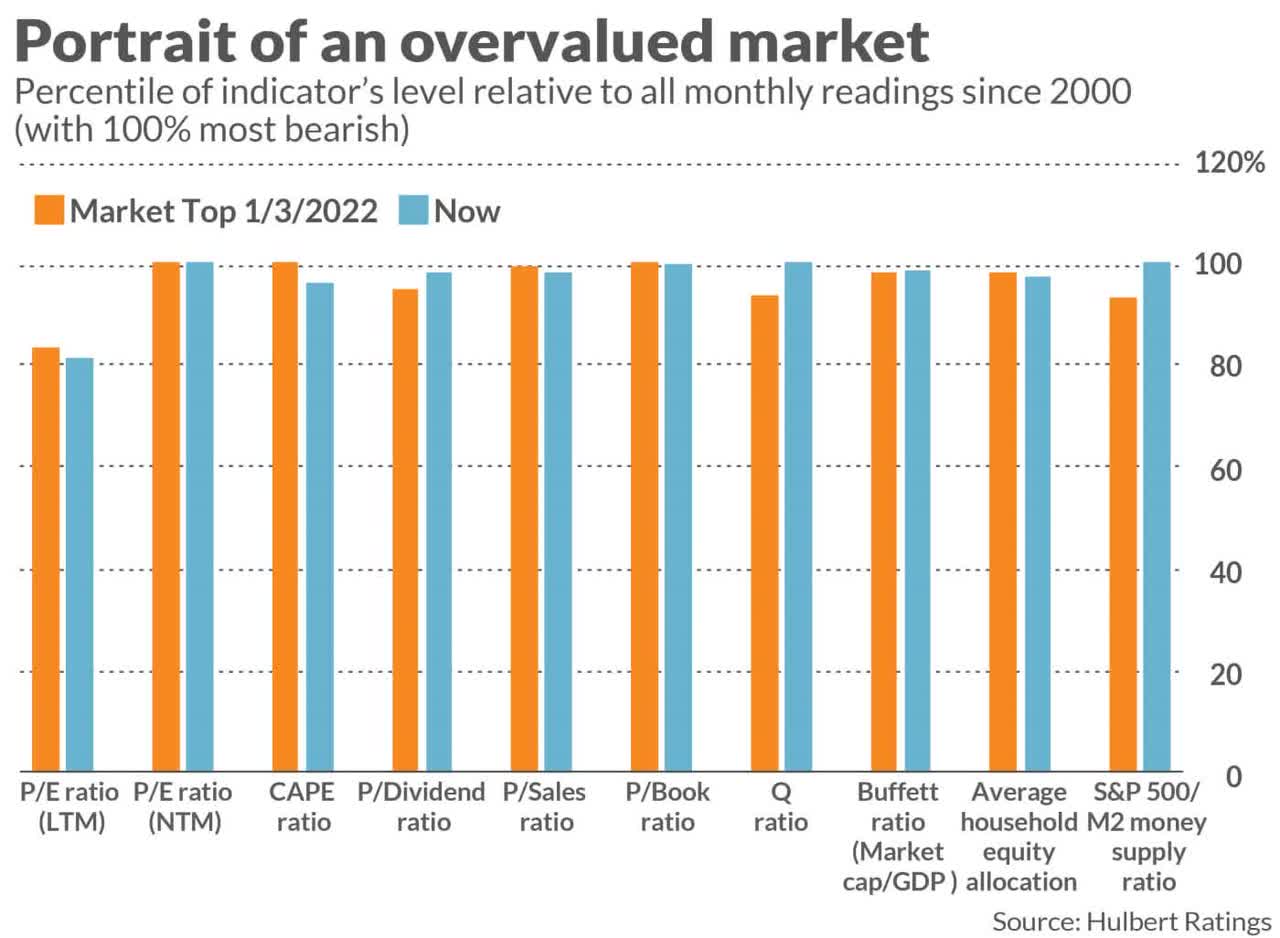

How Overvalued Is The Market?

I have noted how overvalued the market has become in some recent articles (I, II) looking at similar tops just before the Internet Boom turned to the Internet Bust in 2000 and just before the Great Financial Crisis. Today, a piece at MarketWatch does a commendable job comparing today’s market valuation to just before the last bear market a few years back. Here is the comparison to where we are now compared to where equities trading in the very first days of 2022 using a variety of metrics.

MarketWatch/Hulbert Ratings

As you can see, the market is eerily in the same overvalued territory as it was then, just before the S&P 500 lost some 20% of its value in 2022 and the NASDAQ shrank by roughly a third. Now, one can go on believing ‘It is different this time‘. However, after 40 years in the stock market, I can say those can be the five of the most dangerous words in the English language for investors. Prudent investors should allocate their portfolios accordingly.

Read the full article here