A Quick Take On Bicara Therapeutics

Bicara Therapeutics Inc. (BCAX) has filed to raise $200 million in an IPO of its common stock, according to SEC S-1 registration information.

BCAX is developing bifunctional therapy approaches for patients with solid tumors.

The company has seen intriguing early-stage trial response rates for its primary drug candidate, especially in conjunction with another drug treatment, and is well-capitalized by a substantial investor syndicate.

I’ll provide a final opinion when we learn more IPO details from management.

Bicara Overview And Development Efforts

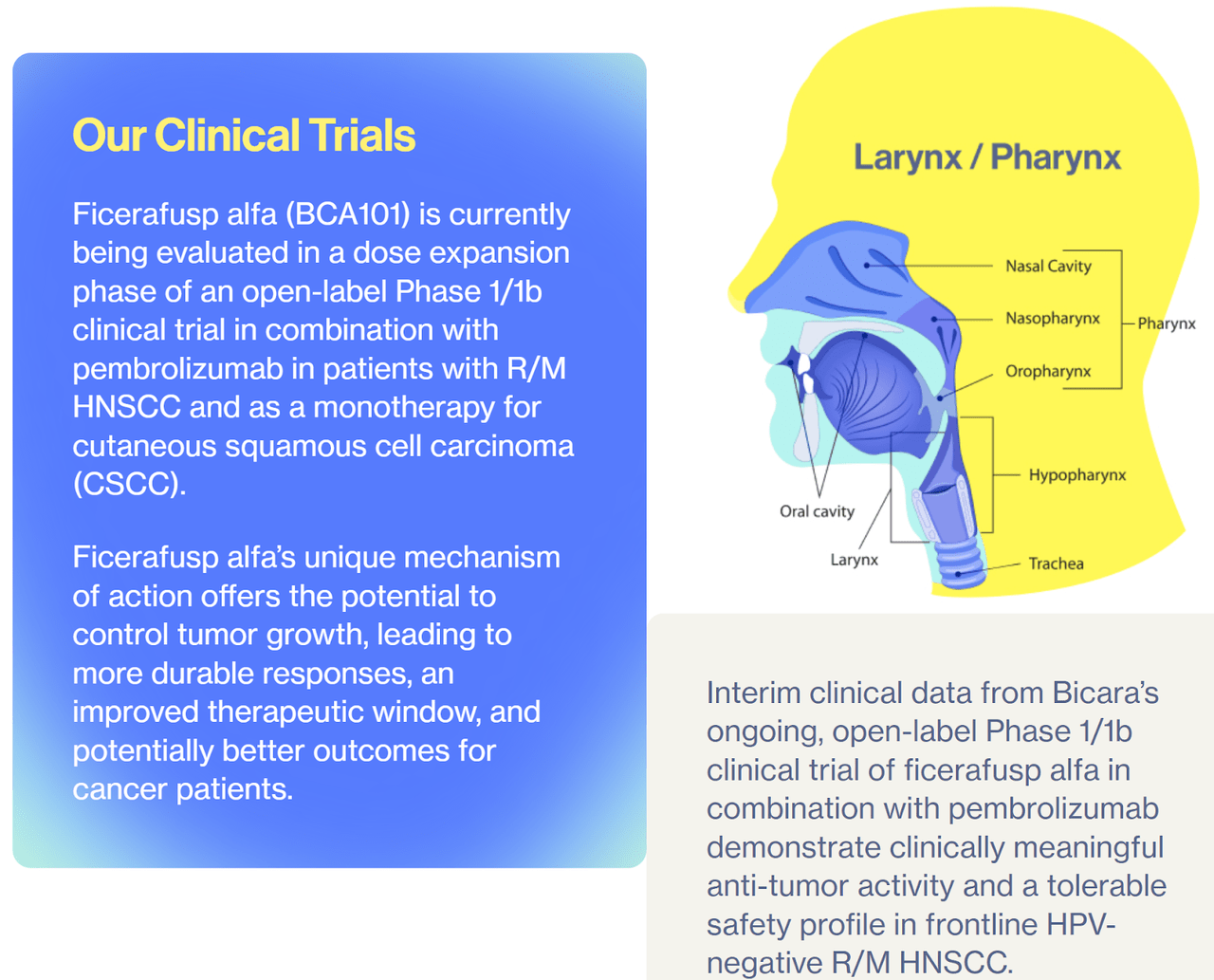

Boston, Massachusetts-based Bicara Therapeutics Inc. was founded to develop bifunctional antibody treatments for patients with head and neck squamous cell carcinoma, or HNSCC.

Management is led by Chief Executive Officer Claire Mazumdar, Ph.D., M.B.A., who has been with the firm since January 2020 and was previously Head of Business Development and Corporate Strategy at Rheos Medicines and an investment professional at Third Rock Ventures, a well-known life science venture capital firm.

The firm’s candidate is ficerafusp alfa, which is currently in Phase 1/1b trials for HNSCC patients.

The company also plans to initiate pivotal Phase 2/3 trials of its antibody in conjunction with pembrolizumab as a first-line therapy in recurrent/metastatic conditions for patients with HNSCC in late 2024 or early 2025.

The current status of the firm’s development pipeline is described here:

Bicara Therapeutics

Bicara has booked fair market value investment of $375 million as of June 30, 2024, from investors, including Biocon, RA Capital Management, Red Tree Ventures, Omega Funds, Invus Public Equities and TPG.

Bicara’s Market & Competitors

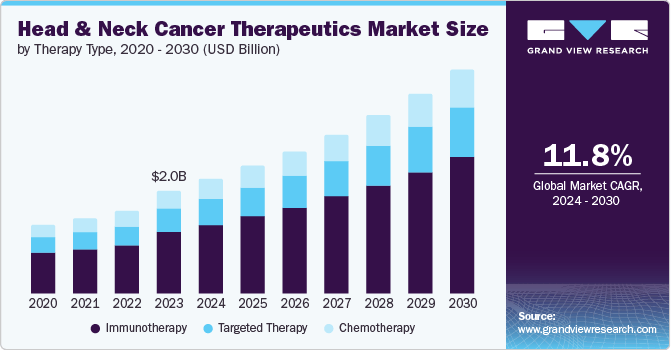

According to a 2024 market research report by Grand View Research, the global market for head and neck cancer therapeutics was an estimated $2 billion in 2023 and is forecasted to reach $4.4 billion in size by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of CAGR of 11.8% from 2024 to 2030.

The primary factors driving this expected growth are a growing frequency of head and neck cancer worldwide and increasing demand for treatment options for various subcategories of conditions.

The head and neck cancer-affected region includes the areas of the head, the oral cavity, the pharynx, the nasal cavity, the hypopharynx, the larynx and the salivary glands.

Also, the chart shown here illustrates the historical and projected future growth trajectory of the head and neck cancer treatment market by therapy type through 2030:

Grand View Research

Major competitive vendors that have developed or are developing similar treatments include the following firms:

-

Merck (MRK)

-

Pfizer (PFE)

-

Genmab A/S (GMAB)

-

Exelixis (EXEL)

-

Merus N.V. (MRUS)

-

Iovance Biotherapeutics (IOVA)

-

Kura Oncology (KURA)

-

ALX Oncology (ALXO)

-

Others

Bicara’s drug candidate is also being considered for additional indications at a later date, including colorectal cancers and other squamous cell cancers, which may represent large market opportunities as well.

Bicara Financial Results

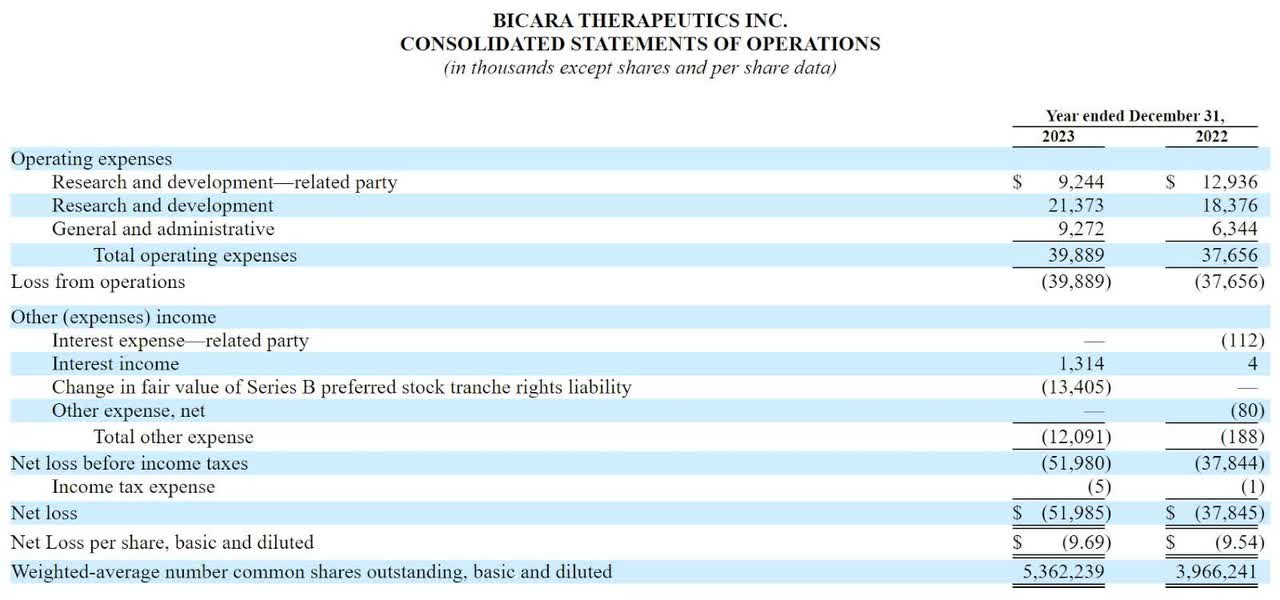

The company’s recent financial results for the past two full calendar years, per its recent IPO filing documents, show zero revenue and significant R&D and G&A expenses associated with its drug development efforts:

SEC

As of June 30, 2024, the company had $204 million in cash and $16.3 million in total liabilities.

Bicara IPO Details

Bicara intends to raise $200 million in gross proceeds from an IPO of its common stock, although the final figure will likely differ.

No existing or potentially new shareholders have yet disclosed an interest in acquiring shares of the IPO, although this may change in future filings.

Immediately after the IPO, BCAX will be a ‘smaller reporting company’ and an ‘emerging growth company’, which will enable management to disclose substantially less information to shareholders, if it chooses to do so.

This document I’ve prepared summarizes the various aspects of these two types of reporting regimes the company may choose to follow.

These reporting regimes were enacted or expanded as a result of the JOBS Act of 2012, which was designed to make it less burdensome for smaller companies to go public.

However, in many instances, the companies going public using these provisions have performed poorly post-IPO, although they have primarily been outside the categories of life science or biopharma firms.

Management said it plans to use the IPO net proceeds as detailed here:

to advance the development of ficerafusp alfa in head and neck squamous cell carcinoma, or HNSCC, and fund our pivotal Phase 2/3 trial for the filing of a Biologics License Application;

to fund expansion of ficerafusp alfa development in additional HNSCC patient populations, such as those with combined positive scores less than one and locally advanced HNSCC;

to advance the development of ficerafusp alfa in additional solid tumors, such as colorectal cancer and other squamous cell carcinomas including the initiation of clinical trials, clinical research outsourcing and drug manufacturing; and

the remainder for working capital and other general corporate purposes.

(Source: SEC)

Leadership’s online company roadshow presentation is not currently available.

For legal proceedings, the company said it was not currently a party to any legal actions that it believes would have a material adverse effect on its financial condition or operations.

The listed bookrunners of the IPO are Morgan Stanley, TD Cowen, Cantor and Stifel.

My Thoughts About Bicara’s IPO

BCAX is seeking U.S. public market funding to advance its primary drug candidate for the treatment of HNSCC and other solid tumor types.

Ficerafusp alfa is currently in Phase 1/1b trials for HNSCC patients, and management has plans to start Phase 2/3 trials in conjunction with pembrolizumab in recurrent/metastatic conditions for patients with HNSCC in late 2024 or early 2025.

In its Phase 1/1b trials, the company saw a 54% overall response rate, a strong result. In a 28-person safety trial in conjunction with pembrolizumab, Bicara witnessed an 18% complete response rate and other encouraging results.

Thus, management believes that along with pembrolizumab, Bicara’s drug has the potential to become ‘a first-line standard of care therapy in HPV-negative R/M HNSCC’.

The market opportunity for the treatment of HNSCC is large and expected to grow as the global population ages and a rise in incidence naturally occurs due to reduced immune system function over time.

Also, the company believes its compound may have treatment capabilities for other cancers, such as colorectal cancer and other squamous cell cancer conditions.

Management hasn’t disclosed a major pharma firm collaboration relationship. However, the company does have some partnerships, including with investor Biocon, an India-based publicly held manufacturer of generic active pharmaceutical ingredients [APIs] that are sold in approximately 120 countries.

The company’s investor syndicate also includes life science-focused venture capital and private equity firms.

With net cash on hand of around $190 million, a strong investor syndicate and positive trial results at an early stage, I estimate the company will have a market capitalization in the range of $500 – $700 million at IPO.

When we learn more about management’s proposed pricing and valuation assumptions, I’ll provide an update.

Expected IPO Pricing Date: To be announced.

Read the full article here