Investment Thesis

In my last article on Palo Alto Networks (NASDAQ:PANW), I discussed the company’s Q3 performance and highlighted the progress made on its platformization strategy. I also highlighted how the partnership with IBM could be a strong growth catalyst for the company, especially in the AI space.

In this article, I dissect the company’s fourth quarter earnings report and argue how the company stands to be a major beneficiary from a dramatically changing cybersecurity landscape. I also analyse how the platformization strategy is progressing and whether there has been any spillover from the global outage caused by CrowdStrike’s flawed update release.

Fourth Quarter Highlights

Palo Alto Networks finished the year on a high, with both the top- and bottom-lines beating analyst estimates. Q4 revenues came in at $2.19 billion, up 12.1% y/y and beating analyst estimates by $26.1 million. Diluted Non-GAAP EPS came in at $1.51, up 4.9% y/y and beating analyst estimates by $0.10. Non-GAAP operating margins continued their upward trajectory, expanding by 320 bps, coming in at 26.9%. Remaining Performance Obligations (RPOs) also came in strong, jumping 20% y/y to $12.7 billion, with current RPO growing 17% y/y to $5.9 billion.

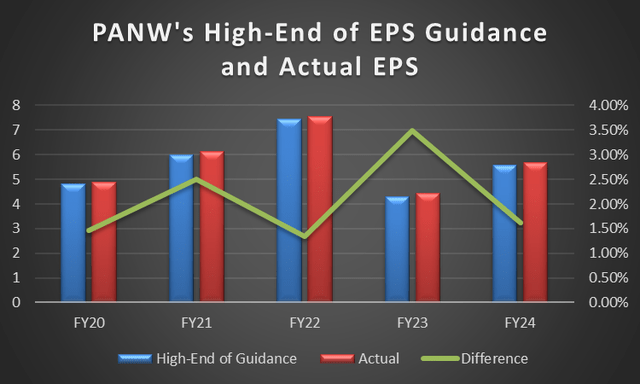

For the full-year, total revenues came in $8.03 billion, which represents a y/y growth of 16.5%. Diluted Non-GAAP EPS for FY24 came in at $5.67, which translates to an impressive y/y growth of 27.7%. Both metrics comfortably exceeded the higher-end of the company’s guidance. The company also announced an additional $500 million for buybacks, which takes the total allocation for buybacks to $1 billion.

The management’s guidance was also strong. Total revenues are now expected to come in between $9.1 billion and $9.15 billion, which translates to a y/y growth between 13% and 14%. Non-GAAP operating margins are now expected to be in the range of 27.5% to 28%, and adjusted free cash flow margins are projected to be in the range between 37% and 38%. FY25 non-GAAP diluted EPS is forecast to come in between $6.18 and $6.31, which would translate to a y/y growth of between 9% and 11%. For the first quarter, total revenues are forecast to be in the range of $2.1 billion to $2.13 billion, a growth in the range of 12% and 13%. Diluted Non-GAAP EPS is expected to come between $1.47 and $1.49, representing a growth in the range of 7% and 8%.

Platformization Strategy Exceeding Expectations

Six months ago, when the company announced that it was pivoting to a platformization strategy, there was pandemonium amongst investors and analysts. The stock had one of the worst days in its history, plunging 28%, as there was a lot of scepticism on whether the company’s plan to push all-in-one bundled cybersecurity packages to clients would pay off. At the same time, investors were also concerned with the headwinds on both revenue and billings growth, which management, at the time, had expected to last 12 to 18 months.

Fast forward to today, and it is clear that the investor reaction that day and their fear that the sudden pivot would have an adverse impact on the company’s growth were both overdone. The company, after adding approximately 65 new platformizations in the third quarter, added over 90 new platformizations in the fourth quarter. During the earnings call, CEO Nikesh Arora announced that about 1,000 of its 5,000 largest customers have now opted for the company’s all-in-one bundled packages, a significant milestone in my opinion, given that the strategy was only widely deployed two quarters ago.

The company also saw its ARRs receiving a boost from platformization, with the average ARR per platformization up over 10% since the first quarter. The company’s NGS ARRs, during the fourth quarter, came in at $4.2 billion, accounting for more than half of the company’s total FY24 revenues. And the company continues to see strong demand ahead, with senior-level customer meetings related to platformization jumping 70% y/y in the second half of the year.

One potential headwind to this strategy could have been the massive global IT outage experienced as a result of CrowdStrike’s faulty update, which laid bare the pitfalls of relying on a single vendor. PANW’s management, however, have not seen this situation affect the demand for platformization yet. On the contrary, following the outage, management, during the earnings call, mentioned that they have seen an uptick in customer enquiries surrounding some of their products such as XDR and XSIAM. Management also re-assured that the company issues its own updates in a “phased manner,” and it has enabled controls so “customers can manage the update process and control it.”

Whether PANW gets a temporary boost from CrowdStrike’s misstep or not is unclear, and it’s too soon to quantify the extent of PANW’s potential gains from CRWD’s crisis. What’s more important to understand is that the entire outage does not seem to have put off customers from adopting the company’s platformization strategy. This development bodes well for the company’s future growth prospects.

Changing Macro Landscape Should Boost Demand for Company’s Products

One of the key takeaways from the company’s earnings call was how the macro landscape is shifting dramatically, leading to increased risks of cyberattacks. According to CEO Nikesh Arora, cyber incidents and their impact are increasing. Financial damages from an individual breach topped $1 billion in the last six months. The company is seeing an increasing number of calls related to customer crises. At the same time that the number and nature of threats increase, the time that enterprises have to address any cyberattack before the damages escalate is falling. The company’s own research showed that in nearly half of the cyberattacks, customer data is exfiltrated within 24 hours. The company has also seen multiple non-government agencies being affected by “nation state activities.”

All of the aforementioned observations are not surprising, in my opinion. According to Statista, the global cost of cybercrime is expected to increase exponentially, from $9.22 trillion in 2024 to $13.82 trillion by 2028. According to the IMF, increasing cyberattacks in the financial sector pose a serious threat to global financial stability. Rising geopolitical tensions have resulted in a significant increase in cyberattacks in the shipping industry, as state-linked hackers attempt to disrupt trade flows. This year’s NATO Summit was also subject to cyberattacks, as hacktivist groups with anti-NATO sentiment deployed a series of attacks with the sole purpose of undermining NATO’s initiatives.

Furthermore, in a world that is undergoing an AI revolution, the nature of attacks are also evolving. A report by Trend Micro found that hackers are developing sophisticated AI-driven hacking tools to exploit the use of AI by enterprises. Deepfakes are also posing an increasing threat to both enterprises and individuals. And with the US elections taking place in November, the risk of cyberattacks using generative AI tools are set to increase in the nation.

All of this means that the demand for cybersecurity products is set to rise significantly. And PANW stands to be a major beneficiary of this demand. There was already some evidence of this in the most recent quarter, as seen by the surge in the company’s RPOs as well as its NGS ARRs. At the same time, the company is also adapting to capitalize on the surging demand. For instance, the acquisition of Talon has helped the company to develop a “natively integrated enterprise browser,” which enables its clients to protect the AI usage of their employees, both in SASE and browser products.

The company also launched its AI Access security offering that protects clients from AI-related cyber threats. At the end of the fourth quarter, over 1,000 of the company’s customers have shown interest to deploy AI Access. Then there’s the company’s acquisition of IBM’s QRadar SaaS assets, which is expected to close next month. The acquisition should give a further boost to the company’s AI offerings, as outlined in my previous article on the company.

Overall, the company generated $200 million in AI ARR for the full year. According to a report by MarketsAndMarkets, the global market size for AI cybersecurity products is expected to reach $60.6 billion by 2028, growing at a CAGR of 21.9%. Therefore, while PANW’s AI ARR remains small relative to the overall ARRs today, I do expect this segment to be a significant source of revenues as well as a major growth lever for the company in the future.

Valuation

|

Forward P/E Approach |

|

|

Price Target |

$353.00 |

|

Projected Forward P/E Multiple |

54.8 |

|

Projected FY25 EPS |

$6.44 |

Source: Company’s Q4FY24 Press Release, LSEG Data (formerly Refinitiv), and Author’s Calculations

As mentioned earlier, the company now expects FY25 diluted non-GAAP EPS to be in the range of $6.18 to $6.31. In the last five years, the company has consistently exceeded its high-end of the guidance, by an average of 2.1%. FY25 would be no different, in my opinion, given that the company has multiple tailwinds such as rising cyberattacks, increasing demand for cybersecurity from AI, the temporary boost from the CrowdStrike fallout, to name a few. As such, I do expect the company to once again beat the upper-end of its guidance. I have assumed that the magnitude of the beat would be 2.1%, the 5-year average. As such, my projected FY25 diluted non-GAAP EPS would come in at $6.44, slightly lower than my previous estimate of $6.71.

LSEG Data, Author’s Calculations

The company, according to LSEG Data (formerly Refinitiv), currently trades at a forward P/E of 54.8x, higher than its 5-year historical median multiple of 49x and its 10-year historical median multiple of 47.7x. However, it continues to trade cheaply relative to its peers such as Zscaler (58.3x) and CrowdStrike (60.95x), and SentinelOne (174.7x). The average long-term earnings growth of PANW, according to LSEG Data, is lower than these names, so the lower multiple is justified. Having said that, the company does deserve a multiple higher than its historical median multiples, given the tailwinds I mentioned earlier. All things considered, I have assumed a forward P/E multiple of 54.8x for my calculations, slightly higher than my previous estimate of 51.3x.

At a forward P/E of 54.8x and a projected FY25 EPS of $6.44, the price target comes to $353, which is slightly higher than my previous target of $344. However, it is around the levels where the stock is currently trading at. The little-to-no upside (1.7%) is hardly surprising, given that the stock is up nearly 18% YTD and is up 6.2% in the last one month. Having said that, it has a strong B+ grade on Seeking Alpha’s Momentum Scale, which suggests that, on the basis of momentum, the stock can continue to trade up. However, long-term investors who want to invest in the company might be better off waiting for a better entry point. As such, I am maintaining my HOLD rating on the stock.

Personally, I have a small position in the name, and while I don’t plan to add at these levels, I won’t be trimming either. In the long-term I continue to believe in the name and in the sector, especially when AI becomes more mainstream. As such, I do plan to continue to add to my position on any weakness.

Risk Factors

As I mentioned in my last article on PANW, while the company has managed its platformization strategy effectively and is reaping the rewards, it still has to strike a balance between ramping up its AI investments and the pivot to platformization. This balance act is one that investors need to consider.

Furthermore, PANW’s competitors are also pivoting to platformization, as evidenced by Rapid7’s announcement of its own platform earlier this month.

Finally, while the strategy has paid off so far, the CrowdStrike outage could put off some companies from relying on a single vendor. And while PANW management, during the earnings call, outlined that the way it deploys its updates are different and that so far, they are seeing a potential to acquire customers, the sentiment of CIOs towards platformization post the CrowdStrike outage remains unclear, which is a risk in my opinion.

Concluding Thoughts

PANW finished FY24 on a high, beating on both the top- and bottom-lines. The company’s platformization strategy is paying dividends and the company is not seeing any negative impact, from the global outage caused by CrowdStrike’s flawed update, on the strategy. The strategy has led to higher average ARR per customer, which has contributed significant growth to its overall ARR.

Moreover, PANW stands to be a major beneficiary as a result of the dramatically changing macro landscape, with both the number and nature of cyberattacks on the rise. The company’s AI-related security offerings are seeing rising demand as AI-related cyberattacks increase. This segment should become a major source of revenue and growth for the company in the coming months, in my opinion.

From a valuation perspective, I see little-to-no upside at current levels. As such, my rating on the company continues to be a HOLD. However, the long-term growth story of the company, in my opinion, remains intact, as the number of long-term tailwinds are too many to ignore. Therefore, any pullback in the name should be a great opportunity for new investors to buy into this cybersecurity leader.

Read the full article here