Dear readers/followers,

Kaiser Aluminum (NASDAQ:KALU) is a business I’ve been covering for a few years now. My latest coverage for this company has been over 16 months ago now, in an article that you can find here. That article has not delivered alpha, but that’s also not what I expected or forecasted. Indeed, I was at a “Hold” recommendation, and in this way, the company has not only underperformed but underperformed significantly. It’s up 11% since early 2023, but the S&P500 is up around 37% in the meantime, meaning less than 0.33x of the S&P500.

In this article, I mean to update you on this company’s thesis and upside going into this year, and the next few years. I’m an investor into aluminum and metals overall, as well as mining, and this company is potentially attractive – but only if we can get it at a price that makes sense for us.

I do not believe that is what we have here – and I will spend this article trying to justify this opinion to you.

A lot of investors I speak to consider beating the market to be “easy”, based on what they hear and see. I do not believe this to be the case. Beating the market requires, as I see it, careful consideration, and careful picking at conservative valuations. So this is what I focus on.

I’d rather have my money generating 3.7% in a risk-free account than put it into an investment that does not have considerable upside potential.

Does KALU have this here?

Let’s see.

Kaiser Aluminum – The company’s results, upside, and what can be seen in 2Q24.

When it comes to metal companies, some of my favorites include Norsk Hydro (OTCQX:NHYDY) and other Swedish and Scandinavian players. I also own a fair bit of thyssenkrupp (OTCPK:TKAMY).

I’ve made a profit in both of these investments – but I haven’t made a profit in KALU because I have not owned it yet. This is not due to fundamentals. 75 attractive years of business expertise makes a convincing thesis for the company at a good price, just not at any price. Given the operational challenges of aluminum, focusing on the vertically integrated players in this field is generally a very good idea. The company combines an organic and inorganic growth strategy, and how the company operates is itself an argument to invest. It’s very rare to find vertically integrated aluminum companies here – and looking at the upper percentiles in terms of margins and results, not many can measure up to KALU, even if they aren’t the “highest” as such.

Where KALU shines is in returns – things like RoE, RoA, ROIC and ROCE – all of these things are looking very good, and it’s better than at least half of the market when it comes to these KPIs in this segment. The latest set of company results confirm the company’s long-term upside, but does create challenges in the more short-term oriented outlook.

We’ve seen a somewhat problematic situation in the metal markets for over a year at this point. The company saw generally good trends in sales, top and bottom line, for most of the time during 2Q24. The company’s EBITDA came in at $53.5M, with an EBITDA margin close to 14.5%. The current strategy is a reduction in inventory levels – but this in itself caused a bit of an accounting effect, with a near 10% charge in LIFO.

The company’s results, as they stand, are driven by solid pricing, lower costs (and continuing to drop slightly), and good business strategies. All of these results were, in fact, despite unplanned outages in packaging, which resulted in lower shipments as well.

So from that lens, the company actually did rather well. The company is executing on stated initiatives for growth and upside…

Kaiser Aluminum IR (Kaiser Aluminum IR)

…but it’s equally clear here that the market is not that impressed by the company’s performance. All you need to do is look at what the market did to the company’s share price, which was a significant drop here.

So what’s going on?

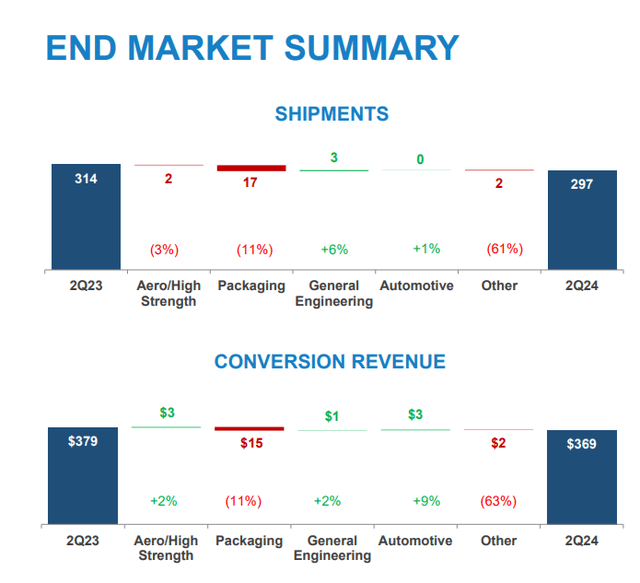

Well, part of it is probably a decline in shipments and lower overall conversion.

KALU IR (KALU IR)

What’s going on here is the upside from Aerospace/High Strength due to better customer diversification, and recovery in engineering. Things will probably continue to be down somewhat as long as automotive doesn’t show a solid recovery here – and anyone’s guess seems as good idea as any here as to when that’s going to happen.

The margins and other results are okay. The company is quite volatile – we’re talking 14.5%, which is both below the highest, but above the lowest sort of result. This quarter has seen some issues in packaging, so without that, we should be above 15%, which would be a fairly solid quarter. The company did well on the sourcing side and cut both management and overhead, as well as manufacturing costs. CapEx for the year is set to be around $190M on the high side, and the company has over $610M in liquidity as things stand on June 30th.

LTM, the company, has managed to generate shipments already in excess of 2023 for some of the company’s key segments. Diversification has been an absolute key in how well the company has been doing here, and “fighting” against the impact of OEM build rates.

For the remainder of the full year, KALU expects the company’s conversion to remain flat (likely a reason why the company went down after this report), a slight improvement in EBITDA margin, focusing on stabilization of operations, as opposed to growth, and moving into a better position for that growth going into 2025E and beyond.

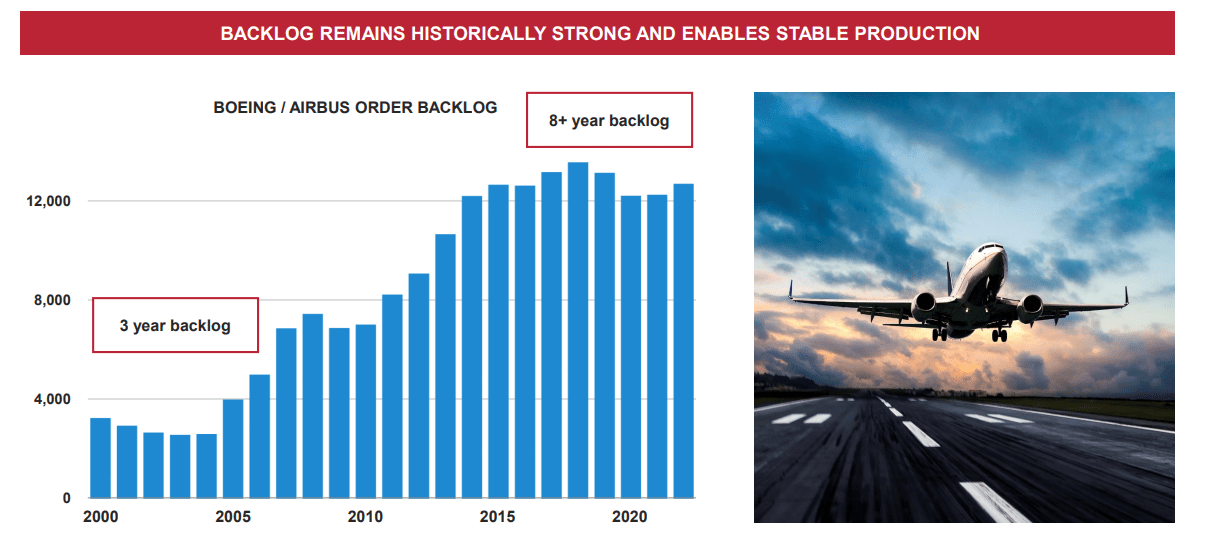

The company does remain a very major player in very important fields – including packaging, Automotive, and general engineering, which I see as the more interesting. The sustainability angle from the aluminum packaging field is going to beat the “plastic” moves from this part of the industry, and this translates to around 5-7% annualized growth rate on the top line in terms of the market.

KALU IR (KALU IR)

Meanwhile, Automotive, which is always a very fickle sort of mistress, is likely going to be a low-growth area for some time. The NA industrial demand should prop things up a bit, but it will be in line with the re-shoring of domestic supply, and we’ll see how this goes. The same thing is true for the Aerospace field, where it’s likely we’ll see growth or moves correlated to how air travel evolves. For now, this seems positive, but there are risks here. This makes the thesis for the company tricky.

Here is what I see in terms of valuation.

Kaiser – unfortunately not a “Kaiser”/Emperor in terms of valuation

The main disadvantages of this company include a less-than-flawless sort of credit rating, with only a BB- and a leverage of 61.7% in long-term debt to capital. As such, the company is somewhat highly leveraged. Aside from this, it’s also very volatile in a way that peers like NHYDY are not. Between 2019 and 2022, the company’s EPS on an adjusted basis fell 56%, 20%, and 106%, going negative in 2022. These results have, of course, recovered – for 2023, we’re back to $2.74 in EPS, but it’s important to note that this EPS does not even come close to matching 2019, which was at almost $7/share when the company traded materially at a similar price to where it does today.

It’s this coupled with the company’s volatility which makes me doubtful about investing here. There is a forecasted resurgence in the company’s earnings – we’re talking 2025E, where earnings are currently forecasted to improve by around 80% (Source: Paywalled F.A.S.T Graphs Link).

But how likely is such a development? 65% of the time, the company’s forecasts and analyst forecasts are negatively missed. So such a forecast would be dangerous to put too much stock in if the company were to underperform. What KALU has going for it is, in fact, the company’s yield, which is actually over 4% at this time and which makes this one of the better-yielding metal companies out there.

But this comes with a price – and that price is that the company does not cover its dividend with earnings. Not for 2023, not for 2024 even, which still falls short 4 cents of coverage. If the company does improve earnings next year, this is not so much of a thing – but again, we do need to consider if the likelihood if this is high or not.

Analysts following the company are split almost down the middle. The company has a high of over $100 and a low of below $70/share. The current share price is $73/share, which is above my last article, but not as much as I would expect, with an average over the $80/share mark. This has the result of having an upside, based on forecasts of around 10%. However, this fails to take into consideration that the company does not have its debt under control. As I said in my previous piece, the hurdle for me to invest in KALU is clarity. I want the company to more clearly show me a conservative upside, and I do not believe the company is currently capable of this.

In my last article, I set a $70/share PT. I could increase it here, but the fact is that current trends in earnings and how the company’s results look in 2Q24, do not give me a lot of hope that the company is about to outperform for the 2024E period.

This makes the company a risk/reward play that is not attractive, i.e., the risk is too high for the reward that is being offered, and I believe there are significantly more attractive opportunities available here.

And for that reason, I can only consider KALU to be a “Hold” here. I look forward to more clarity in 3Q24, to see if there’s a justification for a better upside here.

Thesis

- Kaiser Aluminum is a not-uninteresting aluminum company active in 4 appealing end markets. It has a solid yield, not a solid credit, and difficult, volatile forecasts. In order to make sure that you have a good upside here, you need to buy the company towards the cheaper end of its usual spectrum.

- I still view this as being around $70/share – and this is unchanged from my previous article back in April 2023.

- For that reason, I wouldn’t go higher than “HOLD” at this time – but if the company were to drop enough, I will be investing here. But this would require a drop below $70/share, and where I could see an upside to a conservative 15% annualized.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company, due to BB-, and the current market situation, which is significantly changed, does not fulfill my quality criteria, nor is it cheap. For that reason, I’m only willing to give it a “HOLD” at this time.

Read the full article here