NCR Atleos: Investment Thesis

My previous article in relation to NCR Atleos Corporation (NYSE:NATL) was back on February 13, 2024, “NCR Atleos: Burdened With Debt And Shares Expensive – Sell”. The share price at the time of publication was $23.18 and has since increased by 24.98% to $28.97, compared to a 12.56% increase in the S&P 500. This is a strong reminder that market sentiment is often swayed by matters other than mere fundamentals. I maintain my contention the shares are unjustifiably expensive, coupled with a highly leveraged and weak balance sheet, that significantly increases the risk profile for this business. I maintain a Sell rating on this stock. Below I discuss some of the matters that give rise to the market price of stocks exceeding their intrinsic value for periods of time, although in the longer term fundamentals generally win out. Following this, I provide data in support of my contention the shares are overpriced as well as a summary analysis highlighting balance sheet weaknesses. Here are some of the factors other than fundamentals driving share prices:

1. Actual or potential shifts in fundamentals driving revenue and earnings increases that might or might not be enduring.

A good example of this was the increase in Alpha Pro Tech, Ltd. (APT) share price, from ~$3 to $4 pre COVID-19 to a high of $41.59 in 2020, on the apparent belief the massive increase in sales of Covid-19 masks and protective apparel would continue indefinitely. The share price has now settled back to ~$6. The current growth thesis for NCR Atleos is explained in this excerpt from the company’s Q2-2024 earnings call transcript available through Seeking Alpha:

As global banks seek to improve their customers’ experience in the most cost-effective way, the importance of self-service devices is increasing. As a result, our customers are reinvesting back into their retail banking footprint and embracing shared financial utilities. For them, this strategy will result in lower cost, higher quality, better consumer experience, broader reach, and higher foot traffic. For NCR Atleos, it will drive higher revenue growth, and higher profitability both from scale and a richer revenue mix and predictable free cash flows. In this vein, in the second quarter, we grew services revenue by 6% and grew ATM as a service revenue by more than 30%. We added key new clients to our networks, added new network geographies, and rolled out new transaction types.

My observations on the above, with a caveat. The first is this growth is unlike the temporary boost for Alpha Pro Tech due to COVID-19, and is likely enduring. It appears reasonable for this to excite investor interest in the stock. I will give a positive tick to NCR Atleos for potential enduring growth. The caveat is what effect on ATMs if the trend of some businesses to discourage or decline acceptance of cash for sales transactions eventually results in cash no longer being used as a medium for transactions?

2. Headline results reported by management do not reflect the economic reality

I see a lot of this, where management reports non-GAAP results as a supposed better and fairer means of conveying the underlying earnings of a company. It is true that it can be useful to present non-GAAP results, based on GAAP results adjusted for unusual and non-recurring items, to gain a clearer indication of the underlying current and longer-term profitability of a business. Where I have concerns:

2.1 Exclusion of items of expense, year after year, so these expenses can no longer be considered as non-recurring in nature, but are part of the cost of doing business

In my February 2018 article, “NCR: Understanding The Blackstone Deal – Its Impact On The Company And Its Shareholders”, I wrote,

Blackstone Inc. (BX) was brought in by NCR in December 2015, as an experienced technology investor to add value to and accelerate NCR’s strategic transformation to an integrated software & services company.

And for the eight years ever since 2015, until the split into NCR Atleos and NCR Voyix Corporation (VYX) in 2023, NCR continually and regularly added back significant “Transformation & Restructuring Costs” to GAAP results to arrive at inflated non-GAAP results. It might or might not be true, that the benefit of these costs will be received in the future, but these costs are not brought to account in the non-GAAP results at any time, including in the future. And NCR Atleos continues to add back amounts for “Transformation & Restructuring Costs”, totaling $6 million net of tax in the first half of 2024, even after the enormously costly restructure and separation was concluded in 2023.

2.2 Exclusion of Stock-based compensation expense in arriving at non-GAAP result

GAAP requires a value to be placed on shares issued by way of employee stock compensation for purposes of determining GAAP net income results. It is very clear such expense is a “real” expense when shares are repurchased on the market to offset issues to staff to avoid a dilution effect. I believe it is arguable stock compensation is a “real” expense, whether or not shares are repurchased as an offset. From shareholders’ perspective, the imputed cost of shares issued as part of compensation for employees should not be adjusted out of GAAP earnings to arrive at a non-GAAP result.

NCR Atleos non-GAAP results – a more appropriate formulation

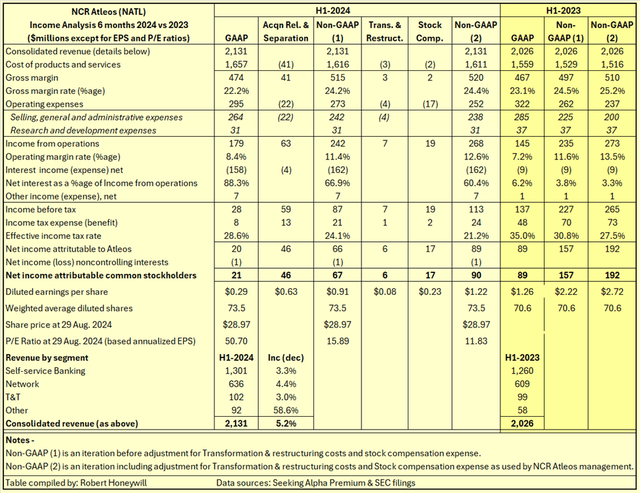

I have compiled Table 1 below to highlight various aspects of NCR Atleos financial performance.

Table 1

SA Premium and SEC filings.

Comments on the financial performance for the first half of 2024 compared to the first half of 2023 follow:

Revenue growth – The period-on-period total revenue growth of 5.2%, per Table 1, is not as encouraging as the statement, “…we grew services revenue by 6% and grew ATM as a service revenue by more than 30%…”, per the Q2-2024 earning calls transcript linked further above.

Non-GAAP (2) – These columns display adjusted non-GAAP figures consistent with NCR Atleos management’s calculation of non-GAAP for purposes of monitoring the financial performance of the business from management’s perspective.

Non-GAAP (1) – These columns display adjusted results which, I believe, are more appropriate for purposes of monitoring the financial performance of the business from a shareholders’ perspective. The remainder of my comments on financial performance relate to the data in these columns.

Gross margin rate (%age) – Gross margin rate decreased slightly from 24.5% for H1-2023 to 24.2% for H1-2024. This is not inconsistent with this statement excerpted from the Q2-2024 earnings call,

…The year-over-year decrease in EBITDA and margin was consistent with our projections that incorporated known dis-synergies and higher labor costs. Macro headwinds remained consistent with last quarter, partially offsetting the productivity savings we have accomplished…

Operating margin rate (%age) – Similar to the gross margin rate, the Operating margin rate decreased slightly from 11.6% to 11.4% between the periods. The effect of higher Selling, general and administrative costs on Operating unit costs was offset by higher revenue and gross margin between the periods.

Net interest as a %age of Income from operations – Here can be seen the huge impact of the debt burden taken on by NCR Atleos under the split arrangements. In H1-2023 net interest expense required just 3.8% of Income from operations. For H1-2024 net interest expense required a majority (66.9%) of Income from operations.

P/E Ratio on August 29, 2024 (based on H1-2024 EPS annualized) – Based on diluted non-GAAP (1) EPS of $0.91 for H1-2024 and the current share price of $28.97, the current P/E ratio is 15.89. This compares to the median P/E ratio of 11.94 for the NCR Atleos sector per SA Premium. Given minimal growth in operating earnings, per Table 1 above, and a weak balance sheet as described in Table 2 below, it is difficult to see why NCR Atleos should attract a P/E ratio in excess of the sector median. At a sector median of 11.94, the share price would reduce from $28.97 to $21.77.

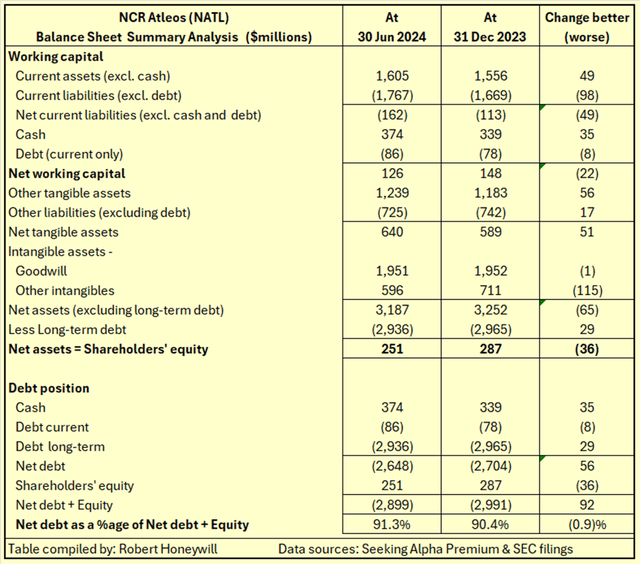

NCR Atleos: Balance Sheet Summary Analysis

Table 2

SA Premium and SEC filings.

Comments on the balance sheet follow:

Net debt as a %age of Net debt + Equity – This is very high at 91.3% – the lenders are the major stakeholders in the business. Despite a small reduction in net debt, the debt ratio has increased by 0.9 percentage points over the last six months, due to shareholders’ equity decreasing over the period.

Debt security – As of June 30, 2024, there is only $640 million of net tangible assets compared to the total outstanding loans balance of $3.02 billion.

Net current liabilities – Excluding cash and current debt, current liabilities exceeded current assets by $162 million as of June 30, 2024, an increase of $49 million over the position on December 31, 2023.

Cash – It can be assumed the $35 million increase in cash will have been generated from the $49 million increase in net current liabilities, rather than from earnings.

Other intangibles – This intangible asset is being amortized, but the amortization is being added back to GAAP earnings to arrive at non-GAAP (1) earnings per Table 1 above. Without the Other intangibles balance of $596 million on the June 30, 2024, balance sheet, shareholders’ equity would be negative, and the business would effectively be 100% debt funded. This is not an issue, per se, but it highlights the fact the business is highly dependent on free cash flows to meet debt repayment obligations, with little option other than an equity raise if free cash flows fall short.

NCR Atleos: Summary and Conclusions

The underlying business of NCR Atleos appears to be a good and sustainable business. My concerns relate to the share price being excessive in relation to the appropriately calculated underlying earnings, and current revenue and earnings growth. This situation is not helped by the high level of indebtedness, which necessarily increases risk. Higher risk requires higher returns, which in turn puts additional downward pressure on the share price. Unless obtainable at a lower share price than the present $28.97, it is likely there will be other stocks available, with higher potential returns and with lower balance sheet risk.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here