I last wrote about Verano (OTCQX:VRNOF) on July 26th, upgrading it to Neutral from Sell. Since then, the company reported a weaker-than-expected Q2. The price dropped on the financial update and then plunged on the news that the DEA has scheduled a hearing for its rescheduling recommendation.

I am upgrading the stock to buy with this article that discusses the chart, Q2 and the changing outlook, and the valuation. Readers of this article will appreciate why I like Verano now. I added some this week to my Beat the Global Cannabis Stock Index that I share with 420 Investor subscribers.

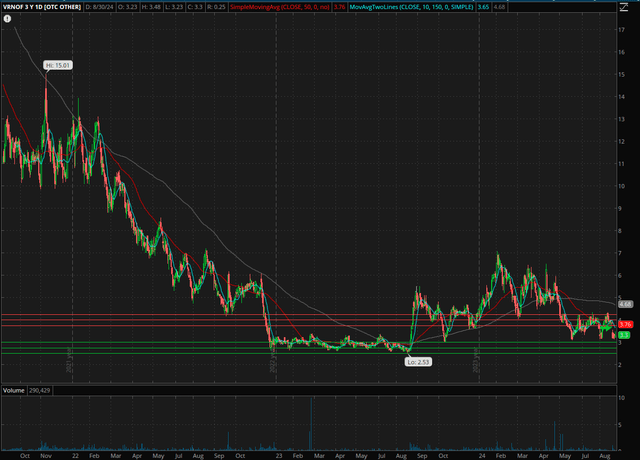

Verano’s Chart Is Beaten Up But Solid

I want to start with the 3-year chart, as it shows what was a very long-term bottom formation that took place in early 2023:

Schwab Thinkorswim

The trading range, which included an all-time low near $2.50 in August 2023 just before the rumor hit that the Department of Health & Human Services had requested that the DEA consider rescheduling cannabis, was roughly $2.50-3.50, and it is back in that range again.

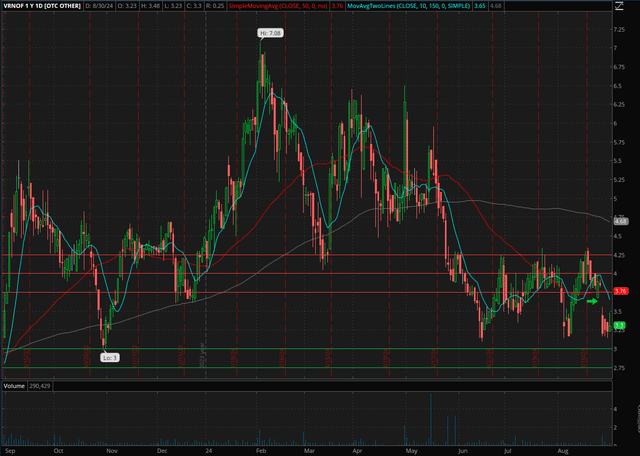

The one-year chart reveals a slightly different perspective:

Schwab Thinkorswim

First, the recent lows are above the late-October low of $3.00. Second, there is a gap above to $3.82. I see support at $3.00 and resistance $3.75-4.25. The stock ended 2023 at $4.48.

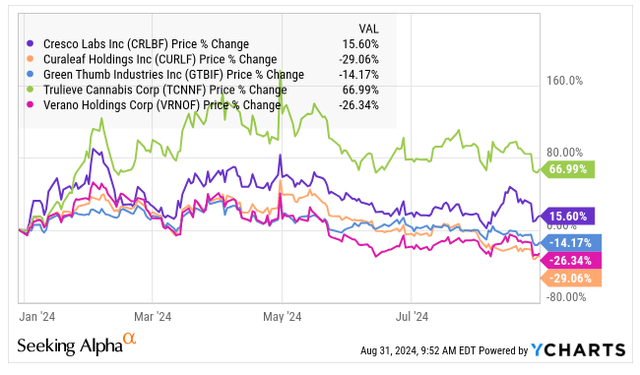

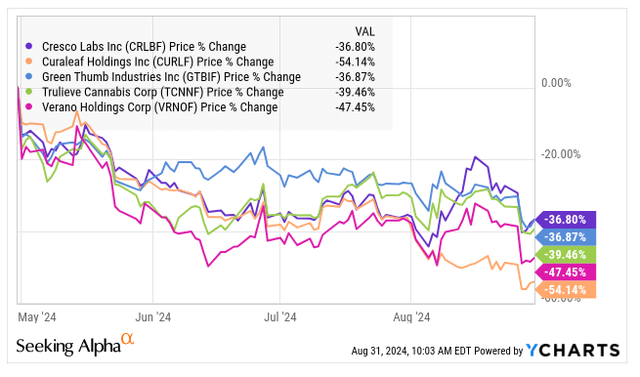

Verano has lagged its peers in 2024:

YCharts

Curaleaf (OTCPK:CURLF), which I upgraded from Strong Sell to Sell last week, is down more, but Verano is below the average of 2.6% by a great deal.

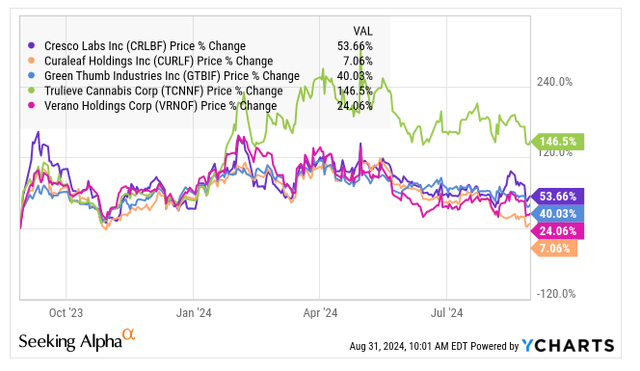

I think that the important dates to look at are 8/29/23, the day before the potential rescheduling news hit, and 4/30/24, when the market peaked on the news that the DEA was officially recommending rescheduling.

YCharts

Since 8/29, Verano has increased 24.1%, but this is below three of its peers by far and above only Curaleaf. The average Tier 1 MSO has gained 54.3%.

YCharts

Since the peak in April, Verano has fallen more than all but Curaleaf. The average decline has been 42.9%.

Q2 Was Rough for Verano

In my piece last month, I warned that the Verano outlook has been deteriorating. I shared a preview with subscribers of 420 Investor ahead of the report on August 7th that analysts were expecting revenue to be $226 million with adjusted EBITDA dropping to $67 million. The company reported Q2 revenue of $222.4 million, up just 0.5% sequentially but down 5% from a year ago. Adjusted EBITDA was ahead of expectations at $70.6 million, but this was down 1% from a year earlier.

In Q2, retail sales revenue fell 12% from a year earlier, while wholesale expanded by 7%. Operating income improved from Q1 but fell from a year earlier by 10%. Operating cash flow of $8 million was down sequentially

The current ratio at the end of Q2 was just 0.99X, showing current liabilities slightly higher than current assets. Net debt rose slightly to $266 million during the quarter. This net debt does not include income tax payable and deferred tax, which total $426 million. Tangible book value was reported at -$50.7 million.

The Updated Outlook for Verano Is Solid

Ahead of the Q4 report, analysts were expecting 2024 revenue to grow 2% to $921 million, according to AlphaSense. They were projecting adjusted EBITDA of $277 million. The company did not provide guidance in its press release that shared Q2 financials due to the pending acquisitions in Arizona and Virginia, which ended up closing in late August. Despite the additional revenue, analysts have reduced their outlook. They now expect 2024 revenue to decline 3% to $908 million. Adjusted EBITDA is projected to fall 8% to $282 million.

For 2025, the analysts were projecting revenue of $1.027 billion with adjusted EBITDA of $328 million, a margin of 31.9%. They now project that revenue will grow 9% to $986 million with adjusted EBITDA growing 9% to $308 million, a margin of 31.2%, which is close to the 31% level that I had used in that article in July.

Despite the M&A, which, I think, made sense both for the buyer, Verano, and the seller, the projected 2025 estimates are lower today than they were before the quarter was reported. How Florida voters decide in November when they vote on adult-use legalization will certainly have an impact on the 2025 projections.

Verano Is Cheap to Its Peers

Comparing Verano to the other four Tier 1 MSOs, it trades at the lowest enterprise value to projected adjusted EBITDA for 2025, tied with Trulieve (OTCQX:TCNNF):

Alan Brochstein, using AlphaSense

Even Curaleaf, which I don’t like at the current price relative to its peers, is cheap compared to where cannabis stocks should trade in my opinion. Verano has a much better balance sheet than Curaleaf, but it is not pristine. Green Thumb Industries (OTCQX:GTBIF) has positive tangible book value and very little net debt.

In the piece I shared here in July, I discussed my year-end target price of $6.49 based on 8X enterprise value to my lower-than-consensus projected adjusted EBITDA for 2025. Updating it for the lower consensus and the adjusted share-count and capital position, I get $6.19. This level, which is below the close on 4/30, would represent a potential gain of 87.5% from the $3.30 close on 8/30.

My year-end target may be too aggressive, as perhaps investors will not improve the valuation until after 280E has been wiped out, which is not likely to take place in 2024. With that said, the valuation could move a lot higher in 2025. Verano is the only Tier 1 name that I hold in my model portfolio that aims to do better than the Global Cannabis Stock Index, and I expect it could do very well in 2025.

Conclusion

While I continue to fear that the analyst margins for Verano are too high, this is not a problem for it in the short term. The company’s next financial update will be in early November. I added it to my model portfolio this week at $3.24, which is down 27.7% from its price at the end of 2023. Still, this price is 28.1% above its all-time low set a little over a year ago.

I continue to expect that the DEA will be successful with its attempt to reschedule cannabis from Schedule 1 to Schedule 3. This will wipe out 280E taxation, which will help cash flow and net income for Verano and all cannabis operators in America.

The chart seems constructive, and the valuation appears very inexpensive relative to peers. Verano is not my favorite cannabis stock by far, as my position in my model portfolio is just 3.1%, which is below its weight in the Global Cannabis Stock Index of 3.3%. I am currently 42.9% MSOs.

While I am optimistic about the investment potential of the MSOs, there are risks. Rescheduling may not happen, and these companies generally have low or negative tangible book values and substantial debt. I believe that ancillary companies, which represent 33.9% of my model portfolio, will benefit from 280E being eliminated as the financial strengths of their customers improve. These stocks trade on the NASDAQ, and some trade below tangible book valuation or at relatively low multiples to projected adjusted EBITDA. I have reduced my Canadian LP exposure to 22.9% in two stocks. Here, there is no benefit from rescheduling, but the stocks appear cheap.

For investors looking to capitalize on cannabis, I think the MSOs are very timely. The elimination of 280E, if it happens, could be a catalyst. It’s not yet clear if Trump were elected President if he would support it, and this is the main risk to rescheduling. For those who want to make a bet and are limited to just the larger names, I think Verano is the best Tier 1 right now. I prefer some of the Tier 2 names and some other smaller ones.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here