Logo of the Laurentian Bank of Canada, or Banque Laurentienne, on their main office in Montreal at dusk.

Note: All amounts discussed are in Canadian Dollars and the stock price refers to the TSX stock price and not the OTC one.

Our work on Laurentian Bank of Canada (OTCPK:LRCDF) (TSX:LB:CA) has not panned out remotely as we expected. But in there are lessons for investors. Failure tends to be a more stern teacher than success, but the lessons are generally more valuable. We will go over our original thesis on this today, review what we got wrong and see how the recent quarterly results play into it.

The First Bull Call

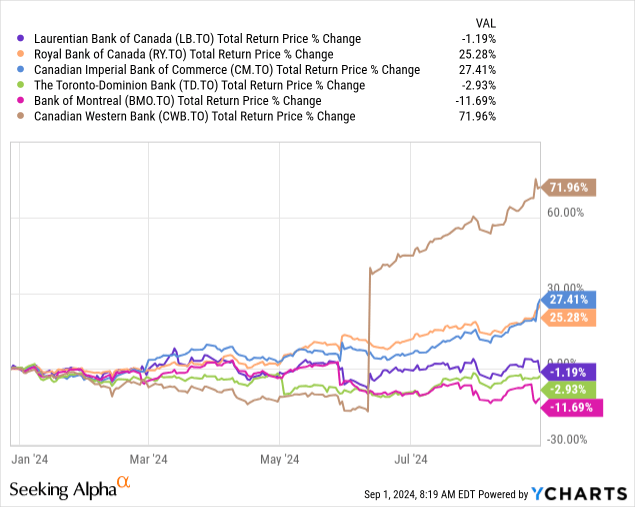

We went with a buy in December 2023. We also gave the preferred shares, Laurentian Bank of Canada PFD SHS SER 13 (TSX:LB.PR.H:CA), a buy rating. It was not the worst possible call we could make. Laurentian beat two of the banks we talked about. Both The Toronto-Dominion Bank (TD:CA) and Bank Of Montreal (BMO:CA) lagged the mediocre returns of Laurentian.

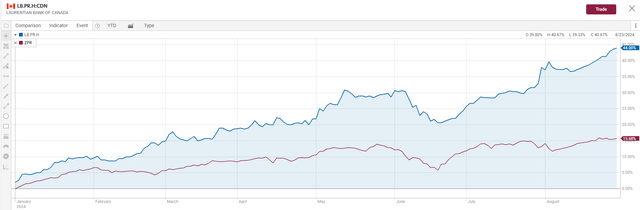

But clearly we went out of our way to dodge a few potential winners. The funniest aspect of our analysis was we postulated that Laurentian could trade at the multiple of Canadian Western Bank (CWB:CA). Instead, CWB was offered a deal to be bought out at a big 6 multiple by National Bank of Canada (NA:CA) and it returned 72%. So on our report card here, we give ourselves a D minus. The preferreds did spectacularly well in comparison. They beat out BMO Laddered Preferred Share Index ETF (ZPR:CA) by more than almost 3:1 margin since we recommended it.

CIBC

We give our performance here an A minus. Of course investors are curious as to how we handle the D minus and that is what we look at next.

Q3

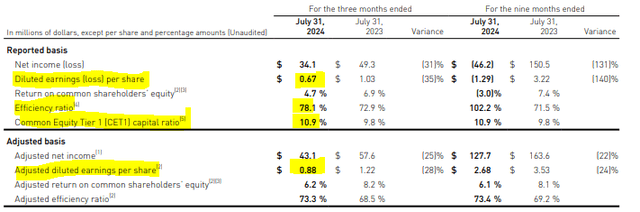

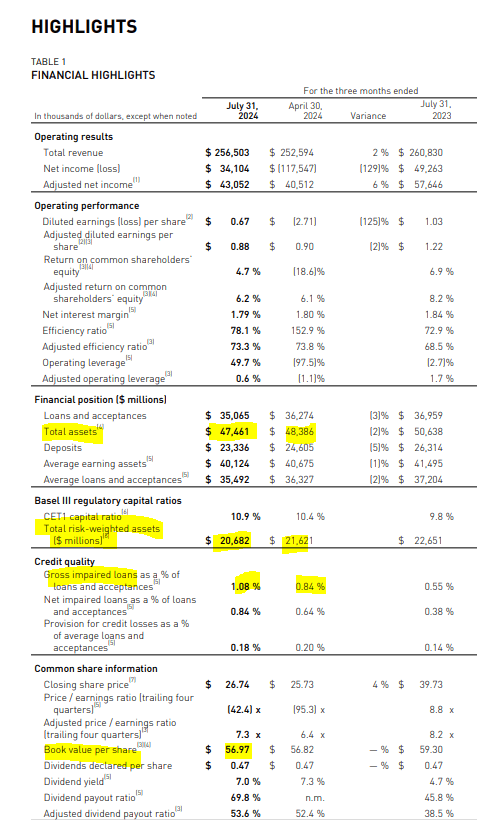

Laurentian has a fiscal year ending in October so we just got results for Q3-2024. They were not pleasant. While adjusted earnings came in slightly ahead of consensus, we would focus here on the diluted actual number of 67 cents a share.

LB Q3 Results

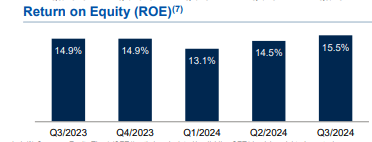

That number showed an efficiency ratio of 78.1% (higher is worse) and this is a bank that was aiming for this figure to be under 60% at one point. The return on equity was 4.7% for the IFRS number, and that meant that you could have made about as much investing in money market assets over that quarter. For comparison, here is the kind of return on equity the number one bank, Royal Bank of Canada (RY:CA) produces.

Royal bank Q2-2024 Fact Sheet

That probably made Laurentian investors sing the Lorde hit song.

And we’ll never be Royals (Royals), It don’t run in our blood

Source: Genius

Yeah, so 4.7% is going to cut it only if Laurentian plans on running a lemonade stand on the east side of Quebec City. So why are they performing so badly? Well, we have reverse economies of scale in play here. Put another way, operating leverage is working against them. Laurentian is shedding assets and contracting its balance sheet. At the same time, it is facing issues from a weakened economy. Gross impaired loans are rising. Finally, progress in book value is marginal as the severance charges keep draining capital beyond the dividend.

LB Q3 Results

At the end of the day, things look about as bad as they can get. But can they get better?

Outlook & Verdict

Laurentian is hopeful that the rate cuts will increase demand for its loans. At least its CET1 ratio is headed the right way.

Yvan Deschamps

Thank you, Sohrab. So I’ll start and maybe Christian is going to add to the answers. So the 10.9%, as you mentioned, of CET1 this quarter, 50 basis point increase came from the loan volume reduction. So reduction in the RWA. And as Eric mentioned, we’re awaiting the rate cuts and we expect pent up demand in inventory financing CRE, including those that will come back and take some of that capital. So we’re currently extremely well-positioned from a capital perspective to sustain that and sustain the plan that we’re launching as well. From a credit perspective, our guidance has been clearly for the last two quarters and is still maintained at the same thing, low 20s to high teens. And pretty much it’s what we see for the next quarter or next two quarters.

Source: LB Q3 Conference Call Transcript

The bank lacks a coherent strategy to improve its valuation and in general, this is hard when you signal that you are ready to issue new shares at less than 40% of tangible book value. Sure, the amounts are small, but there is a signaling effect over here and that is crucial to get big money onboard.

Douglas Young

Hi. Good morning. Just going back to the CET1 ratio and I kind of understand how it flexes with volume growth and you’re sitting at a healthy level right now. But I’m just curious, why have a discounted DRIP in place given where you stand today? I’ll start there.

Yvan Deschamps

Yeah. Thank you for the question. This is Yvan. So, DRIP, if I knock it directly, I would say it’s a program that we try not to stop and start too often. So at this point, we just decide to play prudent. As we mentioned, we have pent-up demand that we expect is going to come back. We need to support the plan that we’re launching. So we’re playing safe in terms of capital at this point. And that includes the DRIP of not trying to turn it on enough depending on a quarterly basis what’s happening.

Source: LB Q3 Conference Call Transcript

The reason the stock probably tanked on the earnings is that there is no end in sight to the efficiency issues.

Douglas Young

So expense ratio is roughly around where we’re seeing them today? That’s kind of what we should be thinking?

Eric Provost

Yeah. And then probably just, it could be a little bit more in Q4, just to the fact of the pressure we just mentioned on top-line from a revenue perspective. So expect to still put pressure on the overall efficiency ratio.

Source: LB Q3 Conference Call Transcript

The bank has two paths to realizing a better valuation. The first is a full turnaround, and we would think that takes at least 3 years. The current management has not inspired confidence that it can be done, so it might require some big shakeup and perhaps a poaching of key executives from the Big 6. The alternative is a modest improvement in the efficiency ratio alongside an improvement in the CET1 ratio to over 13%. This might seem like an unusual gambit, but one we think makes it ripe for an acquisition by the big 6 at the right price. Keep in mind that National Bank paid 1.4X tangible book for CWB. That multiple would mean an $80 stock price for Laurentian. Even more if this happens in 3 years and the bank manages to push its tangible book 10%-15% higher. It is an asymmetrical payoff and while we are disappointed at the way things have panned out, we are sticking with a buy. We own a little and might add more down the line.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here