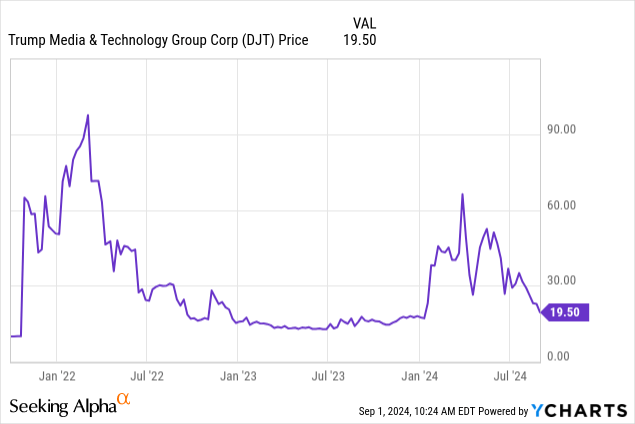

Trump Media & Technology Corp. (NASDAQ:DJT) has dropped recently because bears and political bashers are selling without fully understanding the future potential of TMTG. At the current low price of under $20, DJT is a speculative buy.

My prior articles mostly just focused on the process of merging Digital World Acquisition Corp. with Trump Media and Technology Group, since the value of DWAC stock could only be worth more than the approximate $10 per share liquidating value if the merger was actually completed. This is my first article specifically on DJT as an operating media company. As I disclosed in my prior articles, I was long DWAC/DJT and further disclosed in the comment section of my last article that I sold my remaining DJT stock when it first started trading last March at prices between $60-$70. This article covers why I bought DJT stock at prices below $20 last week and why I now have a buy recommendation.

Valuing DJT – Combination of Three Perspectives

When valuing DJT stock, you need to look at it from a combination of three different perspectives. The first is the trade name “Trump”; the second is from a political angle, which currently means mostly the upcoming election results; the third is from a standard operational valuation, which admittedly has been horrific.

The Trump Brand Is Very Valuable

The name “Trump” is an extremely well-known international brand. Buying DJT stock is currently the only way retail investors can directly participate with the Trump brand. Most of Trump Media and Technology Group’s assets are associated with Truth Social, but that could change because I don’t see restrictions on buying other entities/properties in their by-laws using DJT equity and/or debt. Their recent S-1 even mentions that Truth Social is “TMTG’s first product”, which implies that they are planning to have multiple new products/operations in the future. This is more likely to happen, in my opinion, if Trump does not win this November and wants to use the publicly traded DJT to build a major diverse corporation as a regular citizen and not as an elected official.

Many DJT bears focus on Donald Trump’s long list of failed Trump entities, but they are ignoring the list of very profitable deals, such as the Manhattan residential/commercial development in the old railroad track area over-looking the Hudson River, which was a huge financial success. True, many of the operating Trump companies were failures, whereas his develop/sell projects were the major successful Trump businesses.

DJT Stock Price Related to Expected Election Results

There is a modest correlation between DJT stock price and the probability of a Trump victory in November – the less likely he will win, the lower DJT goes, and the reverse is also true. Some feel that if Trump does not win he will “go off into the sunset” and so will Trump Media. To estimate his election chances, many investors look at polls, which is not really rational, in my opinion, because of the serious problems with most polls. I will post after this article is published a lengthy detailed coverage of polls/surveys issues in the comment section below, but I briefly want to mention one serious problem – polls conducted on Wednesdays, especially in certain states, such as Georgia and North Carolina.

Wednesday evening is Bible study time at church for many Evangelical Christians and if they are in church, they would not be included in polls/surveys conducted by phone that evening. Since Evangelical Christians are one of the strongest Republican groups in the U.S., if they are not included because the poll was conducted on Wednesday evening, others who potentially might be less likely to vote Republican would be included resulting in flawed reported poll results that are less favorable for Trump. (I will cover this Wednesday issue in more detail in the comment section.)

It will be interesting to see if there is any DJT stock price reaction to the September 10 planned debate on ABC, which in the past has been hostile to Trump, in my opinion. I expect most media outlets will declare Harris the winner unless she makes an ‘I beat Medicare’ type of mistake, but voters and DJT stock traders may come to a different opinion.

Actual Operating Results Are a Major Issue

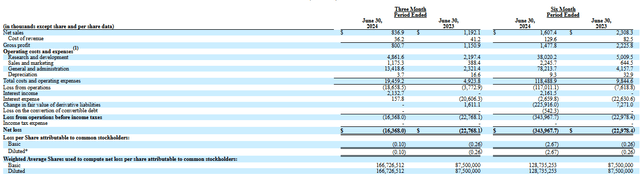

So far, the operating results for TMTG have been terrible – very disappointing. 2Q ’24 revenue was down about 30% from 2Q ’23. It seems, in my opinion, they are too focused on their stated agenda “to fight back against the big tech companies…that may curtail debate in America and censor voices that contradict their woke ideology” instead of focusing on their actual operations, including the Truth Social website. (At this point, TMTG is using just a “pocketknife” to fight back against big tech companies who are using “nuclear missiles”.) Their Truth Social website is far, far below what is needed to fight big tech.

2Q and Six Months Income Statement 2024 and 2023

2Q 10-Q (sec.gov)

(Note: Going forward, the reported results per share will be significantly impacted by increasing weighted average number of shares outstanding.)

Senior management spent a lot of their time on the lengthy and complicated SPAC merger of TMTG and Digital Acquisition Corp. instead of being able to focus on actual operations. In addition, there were serious financial issues facing both TMTG and DWAC before the merger was finally completed earlier this year. I still, however, think that they could have been much more creative in developing their Truth Social website.

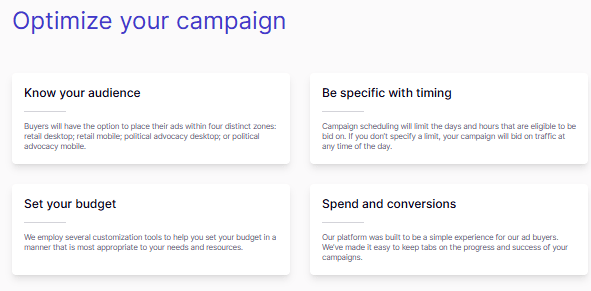

For example, their attempt on their website to gain new advertisers is, in my opinion, very unprofessional. As can be seen below of the copy/paste from their website discussing advertising, it is not engaging. Since this is targeted towards professionals in the marketing/advertising industry, you need some critical metrics in a dynamic presentation – not just boring statements.

truthsocial.com/advertising

While TMTG is still new and trying to grow, their sales/marketing efforts have been very disappointing. Sales dropped to $0.837 million in 2Q ’24 from $1.192 million in 2Q ’23, but sales and marketing expenses increased to $1.175 million from $0.388 million. This might be partially because of their website issues, as I mentioned above, or it might also be the result of their agreements with advertising manager service companies. According to a statement in their 10-Q:

The advertising manager service companies provide advertising services through their Ad Manager Service Platform on the Truth Social website to customers. The Company determines the number of Ad Units available on its Truth Social website. The advertising manager service companies have sole discretion over the terms of the auction and all payments and actions associated therewith. Prices for the Ad Units are set by an auction operated and managed by these companies. The Company has the right to block specific advertisers at its sole reasonable discretion, consistent with applicable laws, rules, regulations, statutes, and ordinances. The Company is an agent in these arrangements, and recognizes revenue for its share in exchange for arranging for the specified advertising to be provided by the advertising manager service companies. The advertising revenues are recognized in the period when the advertising services are provided.

This marketing business model is clearly not working effectively with revenue under a million dollars in a quarter for a multi-billion dollar company. It farms out too much authority to the outside ad manager company, in my opinion. This needs to be changed. I bet even an old school ad sales approach used by magazines decades ago of having a team of salespeople paid a token base salary and a sliding scale commission selling ad space directly to companies and ad agencies could generate significantly higher revenue than they are currently getting.

I also think that they also need to add to their “four distinct zones: retail desktop; retail mobile; political advocacy desktop; or political advocacy mobile”. The focus is way too narrow, in my opinion, for many potential advertisers. I am not sure what would be the most profitable subject areas to add, but investing might be an interesting new zone/area.

A major point DJT bears are missing is that TMTG does not currently have any debt, which is rather unusual for a Trump entity. As of June 30, the company had just under $344 million cash while “burning” $21.4 million cash in 2Q ’24 and $30.8 million for the first six months. They could, therefore, operate for a few years before they would face a cash crisis, and I would expect that eventually their ad sales will become more robust, which could allow them to avoid a cash problem. Their prior accountant statements about “going concern” issues were before the merger, when both TPTG and DWAC had cash issues. There is also the potential for a significant amount of new cash from the Yorkville stock purchase agreement. If they ever get a higher level of operations, they may also be able to negotiate a modest unsecured revolving credit agreement. Remember, TMTG does not have high fixed operating expenses. Many of Trump’s business failures were very capital intensive, but this media business model is not capital intensive. Those expecting a bankruptcy filing are most likely going to be greatly disappointed.

Lock-Up Period Ending

The market is worried that Donald Trump, who owns 114,750,000 (57.3%) DJT shares, could sell some of his stock after the lock-up period ends. The lock-up period ends September 25, but it will most likely will actually end September 20 – “the date on which the closing price for the Common Stock equals or exceeds $12.00 per share… for any 20 trading days within any 30-trading day period commencing on August 22, 2024”.

Trying to predict what Trump will do is difficult to say the least. For two major reasons, I seriously doubt Trump will sell any of his shares in the near future. First, if he sells it may depress DJT stock price, but he actually needs DJT to trade much higher in order to raise cash for TMTG via the Yorkville stock sale deal. Those shares can only be sold with an average price at or above $31.73 according to the July 3 S-1 that states:

We shall not effect any sales under the SEPA and Yorkville shall not have any obligation to purchase Shares under the SEPA to the extent that after giving effect to such purchase and sale the aggregate number of shares of Common Stock issued under the SEPA together with any shares of Common Stock issued in connection with any other transactions that may be considered part of the same series of transactions, where the average price of such sales would be less than $31.73…

In theory, some other different deal with a lower DJT average price minimum could be negotiated in the future, but this is the deal that they are hoping to allow the company to raise needed new cash in the future. Trump needs to take actions to increase the stock price – not depress it by selling stock.

The second reason why I doubt Trump will sell stock in the near term is for political reasons. He does not want the negative media coverage of a plunging DJT stock price during the election process, and he does not want to annoy current DJT shareholders who are also potential Trump voters.

Conclusion

Besides underestimating Trump’s polling numbers, DJT bears and Trump bashers are underestimating Trump Media & Technology Group’s potential. Eventually, I think Truth Social will get their business model right and generate higher revenue/cash-flow. In addition, TMTG could expand into new areas capitalizing on the powerful Trump brand name, which itself is worth billions in my opinion.

TMTG is not highly leveraged – neither financially nor operationally. Given their current high cash and manageable cash burn level, TMTG has plenty of time to get their business model right and potentially expand into other areas. Below $20, DJT stock is a speculative buy, which is an upgrade from when I rated DWAC a hold during the merger process.

Read the full article here