Oscar Health, Inc. (NYSE:OSCR) has a different business model within the life insurance sector, by combining health insurance coverage with technology capabilities, boding well for business growth ahead. However, this appears already well reflected in its share price and investors should wait for a potential pullback.

Company Overview

Oscar Health is a health insurance company, specialized in offering healthcare products and solutions to its members. The company was founded in 2012 and has been listed since 2021, having nowadays a market value of about $4.4 billion, being therefore a relatively small company by this measure.

Its core business is to provide healthcare insurance through its cloud-native technology platform, being its key differentiated factor from traditional insurance companies. Oscar offers health plans in the individual and small group markets, plus a dedicated platform product called +Oscar.

The individual insurance market basically consists of individual and families who buy policies through Health Insurance Marketplaces. The small group market consists of companies with up to 50 employees in some states and up to 100 full-time workers in other states, which means Oscar is focused on a specific segment of the insurance market.

In the individual market, Oscar offers plans in five categories defined by the Affordable Care Act (ACA), which differ based on the size of monthly premium and the level of sharing of medical costs between the company and its members. It also offered the Medicare Advantage insurance, but it has decided to exit the coverage for plan year 2024.

Oscar’s health plans include access to a network of high-quality physicians and hospitals, plus support for its members to find doctors or manage their costs. This means the company puts significant effort in providing a good service to its members and being innovative in its approach to health insurance. In this way, it distinguishes itself in the industry and has a sustainable business model over the long term.

Oscar currently has more than 1.6 million members and offers its insurance coverage in about twenty states. It’s consistently evaluating new market opportunities and the strategic fit of its current markets, potentially entering new markets or exiting current ones based on its proprietary analysis. Over the past couple of years, Florida, Texas, and Georgia were its most important markets based on members, being responsible for about 70% of total membership.

Its membership growth has been strong over the past few years, given that it has increased by a compounded annual growth rate (CAGR) of 37% during 2021-23, and its member retention rate was 82% for coverage plan year 2024. This indicates that Oscar offers a good experience for its members at a reasonable cost, a proposition that should lead to sustainable business growth ahead.

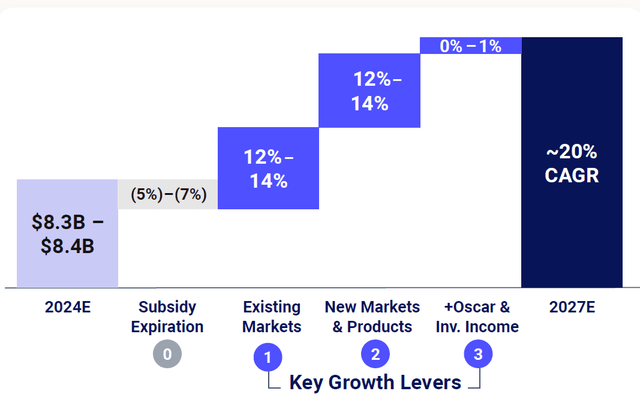

Regarding its growth strategy, Oscar intends to continue to invest in its product offerings and service. It also intends to monetize its technology by allowing industry players to use its platform, which could change Oscar’s business profile in the future somewhat by diversifying its revenues and earnings in a mix of insurance and technology services. Regarding its main financial targets, it wants to grow its revenues by about 20% annually and reach an operating margin of about 5% by 2027.

Business strategy (Oscar Health)

To achieve these goals, Oscar intends to expand its market footprint and establish an Individual Coverage Health Reimbursement Arrangement (ICHRA) business, which should be complementary to its current individual health segment (ACA), plus achieve higher profitability by improving its operating efficiency. These targets seem to be achievable considering Oscar’s track record, but execution is key and there is obviously some risk that the company may fail to deliver on its business goal ahead.

Financial Overview

Regarding its financial performance, as a company in a relatively early growth phase, Oscar has reported strong top-line growth recently. This is supported by its membership growth, but it has reported a bottom-line loss in recent years. This shows that its business model is not yet mature, even though it’s on the right path.

In 2023, its total premiums (after reinsurance) amounted to nearly $5.7 billion, an increase of 47% from the previous year, but its total operating expenses were above $6 billion, leading to a reported loss of about $271 million. Despite that, Oscar was able to achieve an important milestone, as the company reported for the first time a positive adjusted EBITDA in the insurance segment.

During the first six months of 2024, Oscar has maintained an excellent operating momentum, reporting strong revenue growth and improvements in its business profitability. Indeed, in Q2 2024, its revenues amounted to $2.2 billion (+46% YoY), driven by rate increases and higher membership in the individual and small group insurance segments, and its Adjusted EBITDA was $104 million, an improvement of $68 million compared to the same quarter of 2023. Its operating expense ratio was 19.6%, an improvement of about 260 basis points (bps) year-on-year and its medical loss ratio was 79%, improving by 90 bps YoY.

Due to higher revenues and an improvement in its operating efficiency, Oscar was also able to report a positive net income in the quarter ($56 million in Q2), which is quite promising for the sustainability of its business model in the long term. Due to this positive operating performance, Oscar has increased its guidance for the full year, expecting now to reach $9-9.1 billion (vs. $8.3-8.4 billion previously), and its adjusted EBITDA to be in the $160-220 million range ($35 million above its previous range).

This means Oscar is clearly on the right track to achieve its medium-term goals, as revenue growth is beating its estimates for this year. Operating efficiencies are also progressing well, showing that its management is executing well on its growth strategy and its unique business model of combining technology with insurance in the health segment is paying off.

Revenue growth (Oscar Health)

Regarding operating efficiencies, while the company wants to maintain pricing discipline and achieve a good balance between membership growth and good retention of current ones, it does not expect much improvement in its medical loss ratio. Indeed, this ratio has been around 80-81% in the recent quarter, and Oscar is only expecting this to be around 80% by 2027, showing that there isn’t much to improve in this area.

On the other hand, where Oscar clearly has better scale efficiency to gain is in its operating expenses, as a good part of its cost base is fixed. Of its total SG&A expenses, around 30-40% of costs are fixed, which are not projected to change much as the company grows over the coming years. Moreover, due to its technological capabilities, Oscar intends to optimize automation in some processes, which can lead to lower costs in the future. Therefore, its goal is to reduce its SG&A ratio from 24.3% in 2023, to about 16% by 2027, being a key driver of higher operating margins in the near future.

Oscar’s improving profitability in recent quarters and positive business prospects ahead is also important for its organic cash flow and capital generation. The company is now in a good position to finance its growth by reinvesting profits in the business. Oscar has never paid dividends and is not expected to do in the foreseeable future. Instead, it expects to use capital generated in the insurance subsidiaries to reinvest in business growth, especially in its technology, which is its key distinguishing factor compared to traditional insurance companies.

Oscar expects to have about $1.2 billion of enterprise capital by the end of 2024, and expects this capital to grow by a CAGR of 37% over the next three years, which is a good position to support business growth. Moreover, this is also critical for current shareholders because this significantly reduces the potential dilution risk. If Oscar were to remain unprofitable for some more years, most likely it would have to raise capital from shareholders, which would be negative for its share price. As the company has a good capital position and is expected to raise this capital organically in the coming years, the dilution risk seems now to be quite low.

Regarding its valuation, given that Oscar has only quite recently reached positive earnings, I think the best metric to value it is based on book value. The company is currently trading at 3.8x book value, which is not particularly cheap in the insurance sector, and also compared to its history over the past couple of years (2.2x book value on average). Compared to its peers, Oscar’s valuation also appears to be clearly high considering the U.S. insurance sector trades at only 1.27x book value, but this includes insurtech and traditional insurance companies.

Indeed, most mid-sized life insurance companies trade closer to book value, such as its peers CNO Financial Group (CNO) or F&G Annuities & Life (FG), while its insurtech peer Lemonade (LMND) is trading at slightly above 2x book value. Therefore, Oscar’s valuation appears to be moderately high currently, following a strong share price rally over the past year.

Conclusion

Oscar Health is an interesting company by having a different business model than most insurance companies operating in the health segment, combining insurance products with technology to potentially have a moat over the long term. Its business model appears to be sustainable given that it’s now profitable and has good growth prospects ahead, coupled with margin expansion and organic capital generation. Despite this positive backdrop, Oscar Health, Inc. shares aren’t particularly cheap right now, thus investors should wait, in my opinion, for a pullback to enter a position or buy more shares.

Read the full article here