American International Group, Inc. (NYSE:AIG) has made a significant business overhaul recently and seems now well positioned to enter into a new phase of business growth. However, its growth prospects are somewhat muted due to its size and global operations, and its profitability level needs improvement.

Company Overview

AIG is one of the largest insurance companies in the world, having a global business that is present in about 190 countries. The company serves individual, commercial, and institutional customers in several insurance segments, plus it also offers retirement solutions.

AIG has been listed since 1984 and trades on the New York Stock Exchange, having nowadays a market value of about $49 billion. Since the global financial crisis, its operating profile has changed somewhat. Its business has been in restructuring mode for a long time, as the company’s strategy has been to streamline its operations and improve its underwriting performance, which was historically underwhelming.

Underwriting Capabilities

Investors should be aware that underwriting profits and investment income are two critical factors for the profitability of insurance companies. They collect premiums from selling insurance coverage and make a profit if these premiums are enough to cover operating expenses and claims costs. In addition, they also earn income from their investments, which usually are highly concentrated in fixed-income securities. Insurance companies have a low-risk investment allocation because their priority is to preserve their solvency over the long term, rather than seeking high returns from investments.

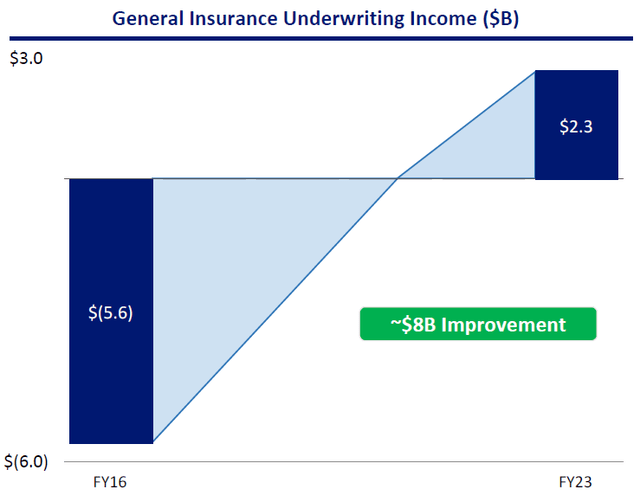

Regarding AIG’s underwriting history, it was not good enough for a long time, as the company lost about $30 billion from 2008-18, showing that AIG clearly needed to improve its core insurance business. Indeed, AIG’s general insurance operations (property & casualty insurance) are the largest one within the group, thus underwriting is critical, while in the life segment, the business is more spread-based, especially in products linked to financial investments and retirement solutions, such as annuities.

AIG made a significant effort over the past few years to improve its underwriting capabilities across the world, hiring experienced underwriters and claims experts. It also made structural changes in how it takes risks and set limits on a single risk, took a more prudent reserve philosophy, and established from scratch a new reinsurance program. This makes AIG much more effective in managing risk and protecting its balance sheet.

As I’ve covered in a previous article on Chubb (CB), underwriting is a key factor in the insurance industry. It’s now easy to have an edge in this area over peers, something that Chubb was able to achieve in the past, showing that having strong underwriting capabilities is key for a sustainable and recurring business over the long term.

AIG was not clearly known for its underwriting capabilities but has improved a lot recently. This is due to its strategic orientation to improve in this matter, something that has been successful recently, as the company has reported an annual underwriting profit of about $2 billion over the past couple of years. This is more important as AIG’s business profile is changing quite significantly, making it highly exposed to the general insurance segment.

Underwriting (AIG)

Business Profile

AIG has transformed its business profile over the past few years, through several divestitures, which have led to a business more streamlined toward the P&C insurance segment. In 2023, it sold Validus Reinsurance to RenaissanceRe (RNR) in a transaction valued at about $4.5 billion and Crop Risk Services to American Financial Group (AFG) for about $240 million. More significant was AIG’s decision to spin off its life business through an IPO of Corebridge Financial (CRBG) in 2022.

While AIG still owned the majority of Corebridge’s capital since its IPO, it has been reducing its stake and has reached a significant milestone during the last quarter, by reducing its stake to less than 50%.

While AIG still holds 48% of Corebridge, the fact that its holding is now below 50% has allowed AIG to deconsolidate from its balance sheet the Corebridge business, which makes a huge difference in its business profile and balance sheet size.

Indeed, Corebridge by itself has a market value of about $17 billion and had, at the end of last June, some $385 billion in assets, which represented about 70% of total AIG’s assets. This is justified by Corebridge being a life insurance business, offering annuities, retirement products, and asset management, which are spread-based products and insurance companies need to own financial assets in their balance sheets to cover liabilities.

On the other hand, P&C insurance has a different profile given that investments aren’t needed to cover liabilities, as personal and commercial insurance claims are covered by written premiums (if the combined ratio is below 100%). Thus, AIG’s investments in this segment are considered to be “insurance company float.”

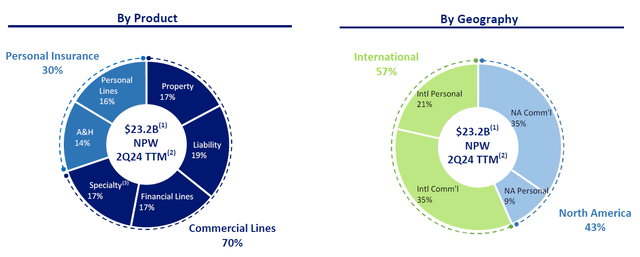

This explains why, following the deconsolidation of Corebridge, AIG’s assets are now much smaller, which should also lead to less sensitivity to rates and lower balance sheet risk, especially concerning interest rate risk. Regarding its business mix, it’s now highly exposed to general insurance, being more tilted to the commercial side, with the majority of premiums being generated in international markets.

General Insurance Profile (AIG)

As the company has been investing its underwriting capabilities and probably couldn’t generate much value in the life insurance segment, this strategic decision to separate AIG into two different companies seems to make sense. Synergies between the two segments are also quite low, and the capital benefit of having a more diversified business profile is not great. Given AIG’s current business mix, AIG’s underwriting performance is now even more critical to its profitability over the long term than before, as underwriting profits should be its most important driver of earnings in the future.

Indeed, the allocation of its $92 billion investment portfolio is similar to most insurance companies, being heavily exposed to low-risk fixed-income securities, which represent about 92% of total investments (excluding its stake in Corebridge). Including this stake, fixed-income securities represent some 84% of the total investment portfolio, which is still a high concentration of investments in low-risk assets. At the end of Q2 2024, the average duration of AIG’s portfolio is relatively low at less than four years, which is explained by its recent deconsolidation of the life segment (which usually has much more exposure to long-term rates), being aligned with the average duration of its liabilities.

Therefore, AIG’s asset-liability management (“ALM”) is aligned with best practices in the insurance industry, and its balance sheet exposure to interest rate risk should be relatively limited. This makes sense given that interest rates should be at its cyclical peak and higher rate volatility is expected ahead.

Financial Overview

Regarding its financial performance, investors should be aware that looking at AIG’s historical earnings is not a reflection of its earnings power or the potential path of its future financial performance. This takes into account that AIG has been for many years in restructuring mode and has changed quite significantly its business profile.

This phase seems now to be over following the deconsolidation of Corebridge, but AIG still has a significant equity stake in the company. This could lead to some earnings volatility ahead, given that it still represents about 10% of its investment portfolio.

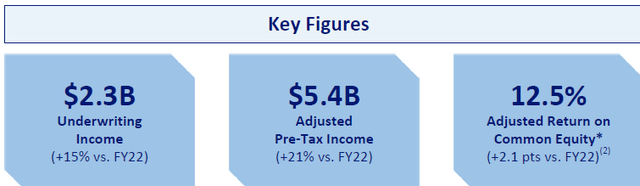

Moreover, even considering only the general insurance segment, there were two significant transactions in 2023. Thus, investors should look into historical trends in this segment with some caution. Nevertheless, AIG reported a positive operating performance in the general insurance segment in 2023, supported by a higher underwriting profit ($2.3 billion in the last year, up 15% YoY). Its combined ratio improved by 130 basis points (bps) during the year to 90.6%, and its investment income increased by 27% YoY to more than $3 billion due to higher interest rates. Its return on equity (ROE) ratio was above 12.5% in the general insurance segment, a much higher level than its overall ROE reported in 2023 (about 9%).

General Insurance KPIs (AIG)

During the first six months of 2024, AIG has reported a positive operating income in its general insurance segment, which bodes well for its business prospects ahead. Despite that, in Q2 2024, AIG has reported a net loss due to the accounting treatment of Corebridge’s deconsolidation. Thus, its reported financial figures don’t reflect its underlying operating momentum.

Adjusted for this effect and its divestments made in 2023, its net premiums written increased by 7% YoY to $6.9 billion in Q2 2024, while its combined ratio was 92.5% (+10 bps YoY). Due to lower operating expenses, its underwriting profit increased by 2.4% YoY to $430 million, and AIG’s investment income was up by 9.5% YoY to $746 million. This shows that AIG’s operating momentum is quite good, a trend that is expected to be maintained in the near future.

Indeed, according to analysts’ estimates, AIG’s net written premiums and earnings are expected to grow at mid-single-digit rates over the coming years. Its ROE is estimated to increase from about 8% this year to about 12% by 2026. This is a good improvement in its profitability, but it is still below some of its peers, such as Chubb. That company has an ROE of around 13%, showing that AIG still needs to do some work to have higher underwriting profits in the near future.

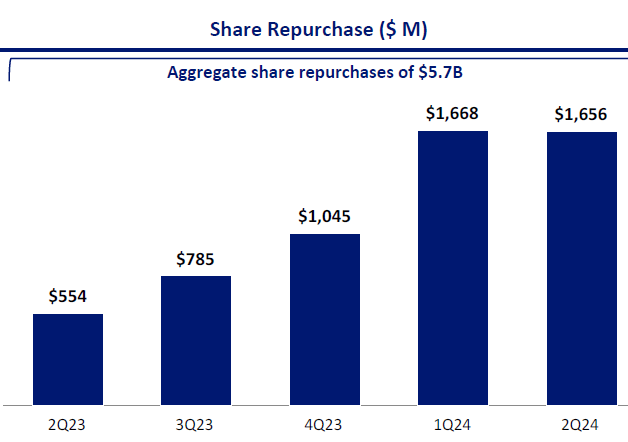

Regarding its balance sheet, AIG has a solid position given that its debt-capital ratio was only 18% at the end of Q2 2024. This is a relatively low leverage ratio and within its target range of 15-20%, plus its U.S. general insurance companies had a capital ratio of 484%, well above its target of higher than 400%. AIG is well capitalized and does not need to retain many earnings in the future, allowing it to return significant capital to shareholders.

This has been its strategy recently, both through dividend and share buybacks, even though its dividend yield is currently slightly above 2%, which is not particularly attractive for income investors. However, this happens because AIG’s priority has been to repurchase shares given that quarterly dividend outflows are about $260 million and over the past couple of quarters it has allocated more than $1.6 billion to share buybacks.

Share Buybacks (AIG)

This strategy is not expected to change much in the near future. Thus, AIG’s income appeal is expected to remain low over the coming years, considering that its annual dividend is estimated to gradually increase to around $1.80 per share by 2027, compared to $1.60 per share expected in 2024.

Regarding its valuation, AIG is currently trading at 1.1x book value, which is above its historical average over the past five years at about 0.8x book value. However, AIG’s business profile and earnings power have improved significantly over the past few years, thus, in my opinion, a higher multiple compared to its past is deserved. Compared to global peers, such as Zurich (OTCQX:ZURVY) or AXA (OTCQX:AXAHY), AIG is trading at lower multiples given that its peers trade on average at about 1.2x book value, but considering AIG’s below-average ROE this seems to be justified.

Conclusion

AIG has made a significant overhaul of its business profile recently, of which the recent deconsolidation of Corebridge is an important milestone, now having a high reliance on the P&C segment globally. While its growth prospects are somewhat muted, the company has invested in improving its underwriting capabilities. Thus, it can achieve higher earnings growth than top-line growth over the coming years. However, its current profitability is still below the average of its peers and its valuation seems fair. Thus, investors should stay on the sidelines on its shares for now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here