Introduction

As it has been a while since I discussed Eagle Point Credit (NYSE:ECC) and its perpetual preferred shares, I wanted to keep an eye on the company’s ability to continue to cover the preferred dividend payments. The yield on the preferred shares has increased to 8.7% and I still think this offers a good risk/reward ratio.

The earnings reported by ECC remain strong

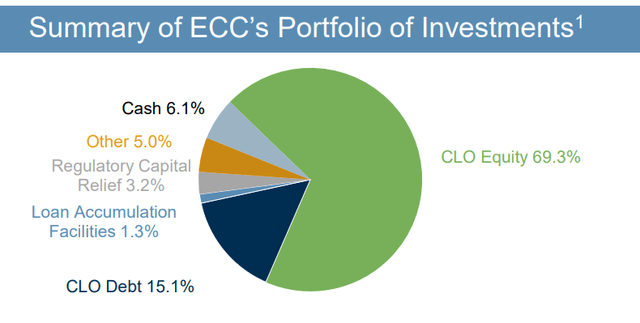

In Eagle Point Credit’s case, the majority of the portfolio consists of CLO Equity. Those investments are at the bottom of the CLO food chain and only received the ‘leftovers’ in terms of income. Only after all payments on the CLO Debt securities have been covered, the CLO Equity will receive a payout. Of course these higher risk securities come with a higher reward as the CLO Equity investments tend to have a return of around and even over 20% these days.

ECC Investor Relations

Given the higher risk element in CLO Equity versus CLO debt, it’s important to keep track of the default rate of the CLO issuers, as it is very unlikely CLO Equity will recover anything in the event of a default. But as the 12-month trailing default rate was just 0.92% at the end of June (a decrease from the year-end 2023 default rate), and that of course is a very manageable percentage that could easily be absorbed by the incoming cash flows from the performing securities.

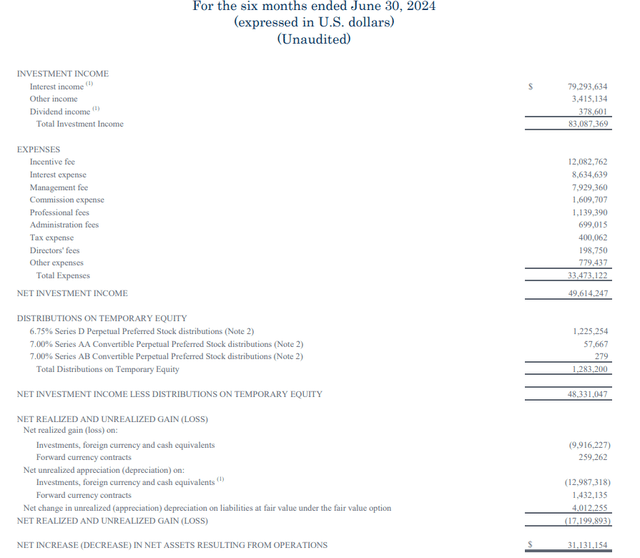

As shown below, Eagle Point Credit generated a total investment income of $83.1M in the first half of this year. Meanwhile, the total expenses came in at $33.5M (and this includes the interest payments as well as the dividend payments on the term preferred stock) resulting in a net investment income of $49.6M.

ECC Investor Relations

As shown above, the $1.22M in preferred dividend payments on the Series D preferred stock, resulting in a net investment income of $48.3M after the distributions.

The income statement above tells us two things. First of all, the payout ratio of the Series D preferred dividends versus the net investment income is less than 3%. That is great. Secondly, it also shows that the company could cover almost $100M per year in defaults before reporting a net loss. So while CLO Equity is riskier than CLO debt, in ECC’s case the higher CLO income is more than sufficient to cover the impact of the potential defaults.

The income statement also shows there was a realized loss of $9.9M on investments, which means that the net investment income minus realized losses was approximately $38.4M. Divided over 97.8M shares, this results in a result of approximately $0.39/share. I am not including unrealized losses here, as these losses either A) do materialize and end up in the category of realized losses or B) don’t materialize, and the market price trades closer to par value closer to the maturity date of the securities. So based on the current results and default rate, the preferred dividends are very well covered.

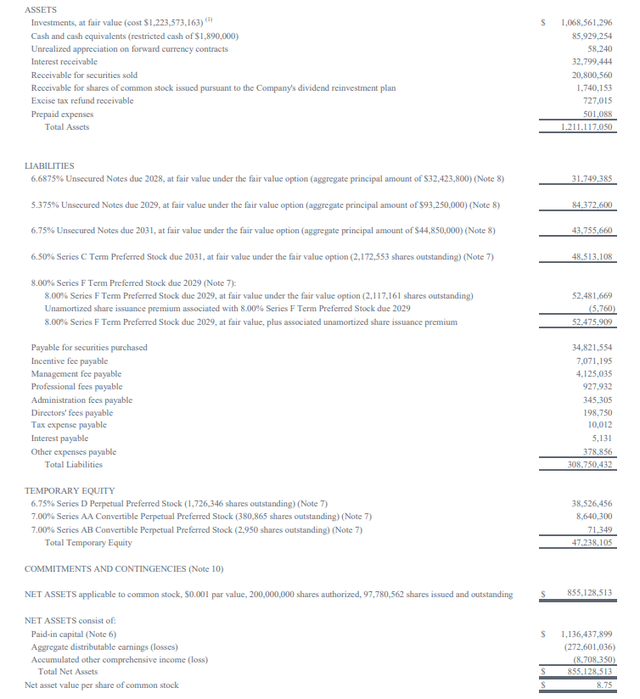

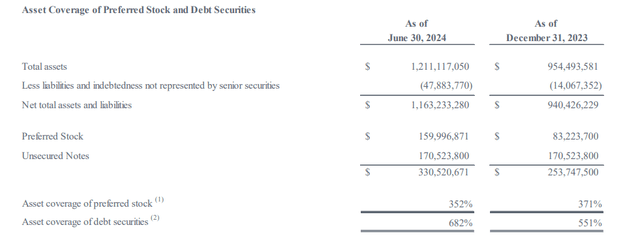

The asset coverage ratio remains excellent as well. As you can see below, there are 1.73M preferred shares outstanding (excluding the term preferred shares which are included in the liabilities segment and aren’t counted as equity), resulting in preferred equity of $47M to which the $855M in common equity ranks junior.

ECC Investor Relations

And thanks to the robust balance sheet, the company also handsomely meets the minimum 200% preferred stock asset coverage ratio, with a total coverage ratio of 352% as of the end of June.

ECC Investor Relations

So from both the dividend coverage perspective and the asset coverage ratio perspective, I’m not worried about ECC’s payment commitments.

Adding duration to my portfolio using the perpetual preferred shares

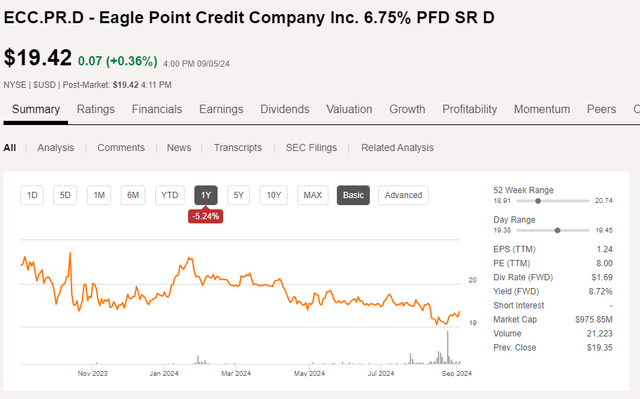

While Eagle Point Credit has several issues of term preferred shares and baby bonds outstanding, I became increasingly intrigued by the perpetual preferred shares, trading with (NYSE:ECC.PR.D) as ticker symbol. The Series D preferred shares are currently trading at $19.42 (shown below) which means the current yield is approximately 8.7%. As these are perpetual preferred shares without a firm maturity date, it’s pretty useless to calculate a yield to call (which would be the better metric to use for the term preferred shares). As 6.75% is a pretty low cost of capital for Eagle Point Credit, I’m not counting on these preferred shares being retired anytime soon.

Seeking Alpha

These preferred shares pay an annual distribution of $1.6875 per share, payable in monthly tranches of just over $0.14 per month.

Investment thesis

I currently have a small long position in ECC’s preferred shares Series D as I like the risk/reward ratio and as the perpetual nature of these preferred securities adds duration to my portfolio. I may add some of the other preferred or debt securities to my portfolio. Meanwhile, the common shares appear pretty interesting as well as the current quarterly distribution of $0.48/share (paid monthly) is decently covered while the yield on the common shares is approximately 19%. But while the distribution rate on the common units is appealing, let’s not forget the stock is trading at a premium of almost 15% to its NAV but Eagle Point continues to sell common stock on the open market at the same premium.

Read the full article here